Government/Policy

March 28, 2017

The Data Shows the Trade Cases Have Failed: The Question is Why?

Written by John Packard

If the goal of the 2015 CORE, cold rolled and hot rolled trade cases was to reduce the number of foreign steel tons coming into the United States, well, the data says the cases did not complete their mission. There is one exception, hot rolled steel imports did indeed move lower and continue to move lower so far this year (compared to last).

If the goal was to take U.S. flat rolled steel prices to today’s lofty world leading prices – well, then they succeeded.

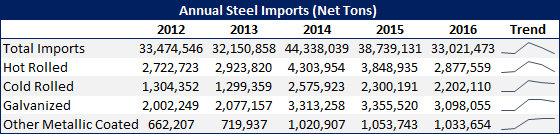

Imports of foreign flat rolled steels peaked in 2014 prior to the launching the antidumping (AD) and 2014 to 33 million net tons by the end of last year. However, from a flat rolled standpoint the victory is hollow at best and in some cases nonexistent.

In the table below, we are showing total imports for the years 2012-2016. We are also displaying the hot rolled, cold rolled, galvanized and other metallic (mostly Galvalume) and it is important to review the data to see how successful the trade cases have been at stopping the flow of foreign steel into the U.S.

Hot rolled tonnage surged to 4.3 million tons in 2014 and remained quite high the following year. When we get to 2016 we see HRC imports dropping back to the levels seen in 2012/2013.

Cold rolled imports also surged up to 2.5 million tons in 2014. Since then there has only been a modest decline reaching 2.2 million tons last year which is still 900,000 tons above 2012/2013 levels.

Galvanized imports also grew to 3.3 million tons in 2014 from 2.0 million tons the previous two years. Amazingly, even with trade suits 2015 tonnage exceeded 2014 and 2016 were 3.0 million tons, one million tons more than 2012/2013.

Other metallic, most of which is Galvalume, went from 660,000 tons in 2012 to 1.0 million tons in 2014. The trade suits on AZ (part of the CORE suits) were filed in June 2015 and imports have not dropped, they continue to be 1.0 million tons.

If you believe what traders have been telling Steel Market Update in our surveys the expectation is for 2017 to see imports at worst remain the same as 2016 and most of the trading companies were telling us that they would drop by 10 to 25 percent.

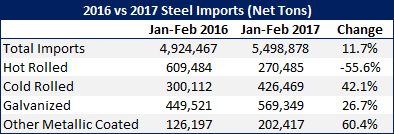

So, we take a look at the first two months of 2017 import data from the U.S. Department of Commerce. We are finding total imports are up 11.7 percent. Hot rolled imports dropped 55.6 percent. Cold rolled imports rose by 42.1 percent, galvanized up by 26.7 percent and other metallic coated up 60.4 percent.

The question is why?

Is it because the Chinese are circumventing the U.S. trade laws by shipping substrate to Vietnam and other countries to be transformed and then sent to the U.S.?

Is it because other countries are able to produce steel at so much lower prices and then are able to add freight and other costs on top of that cost and sell it to the U.S. cheaper than it can be made here?

Is it because the domestic mills have taken advantage of the trade cases and have used the cases to take the spread between hot rolled and cold rolled/coated base prices to $200 per ton or more instead of maintaining the $100-$120 per ton spread seen prior to the trade suits?

Maybe it is all currency related (strength of the U.S. dollar makes U.S. market more attractive)?

Maybe it is something else or a combination of all of the above. What do you think?

Send your comments to: John@SteelMarketUpdate.com