Prices

August 12, 2018

June Apparent Steel Supply Down to 8.9 Million Tons

Written by Brett Linton

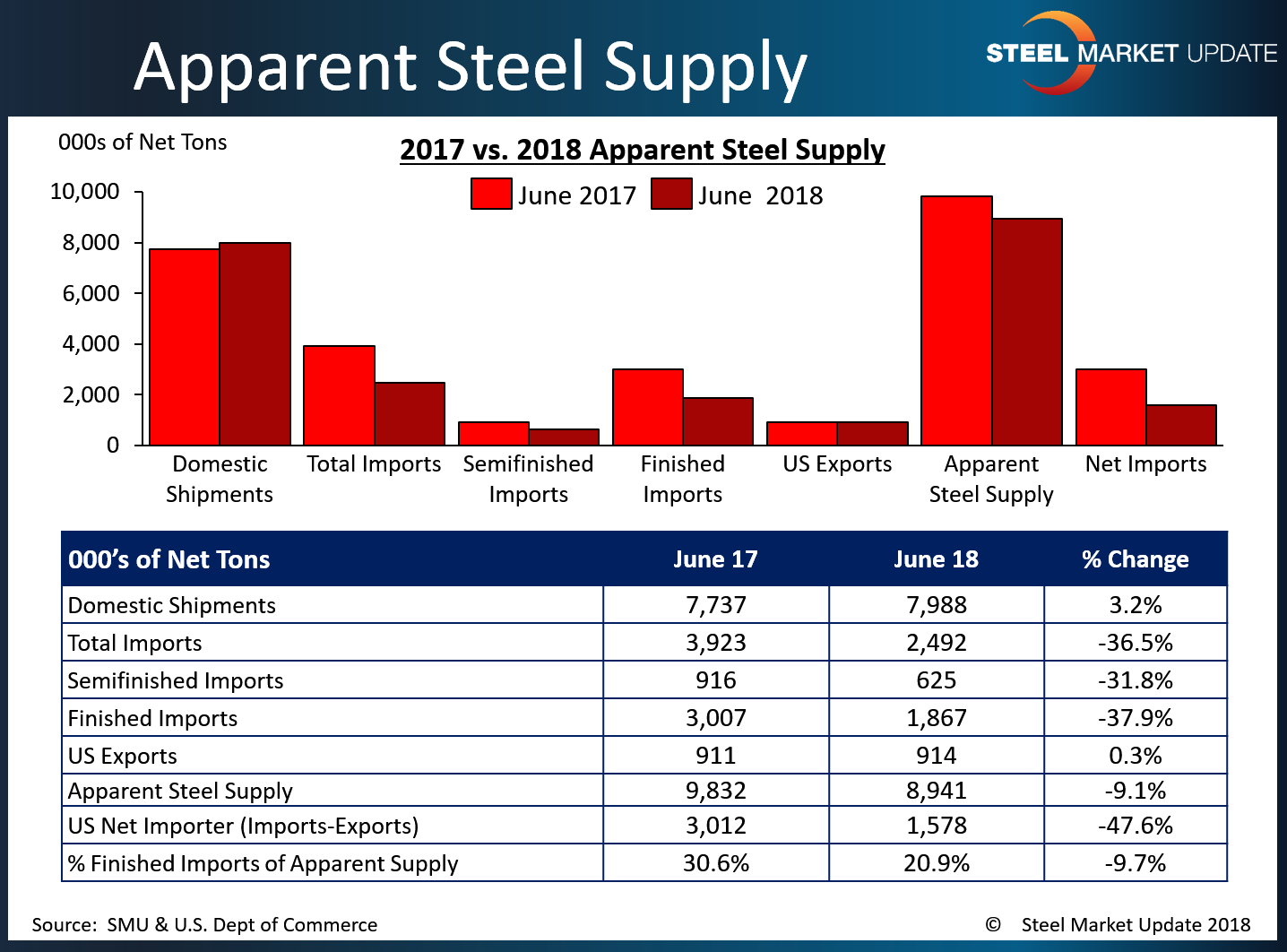

June apparent steel supply fell 7.4 percent over May to 8,941,089 net tons, according to government data released late last week. Although down somewhat, supply remains in line with levels of the last three years. Apparent steel supply is calculated by adding domestic steel shipments and finished U.S. steel imports, then subtracting total U.S. steel exports.

June apparent steel supply saw a 891,410 ton or 9.1 percent decrease compared to the same month one year ago. This change was due to a decrease in finished imports of 1,139,872 tons or 37.9 percent. A 251,180 ton or 3.2 percent increase in domestic shipments lessened the overall decline in apparent steel supply. Exports were flat, up just 2,717 tons or 0.3 percent.

The net trade balance between U.S. steel imports and exports was a surplus of 1,577,870 tons imported in June, down 494,109 tons or 23.8 percent from the prior month, and down 1,434,268 tons or 47.6 percent from one year ago. Foreign steel imports accounted for 20.9 percent of apparent steel supply in June, down from 25.4 percent in the prior month, and down from 30.6 percent one year ago.

Compared to the prior month when apparent steel supply was 9,654,200 tons, June supply fell by 713,111 tons or 7.4 percent. This was due to a decrease in finished imports of 588,739 tons or 24.0 percent, a decrease in domestic shipments of 68,340 tons or 0.8 percent, and an increase in exports of 56,032 tons or 6.5 percent.

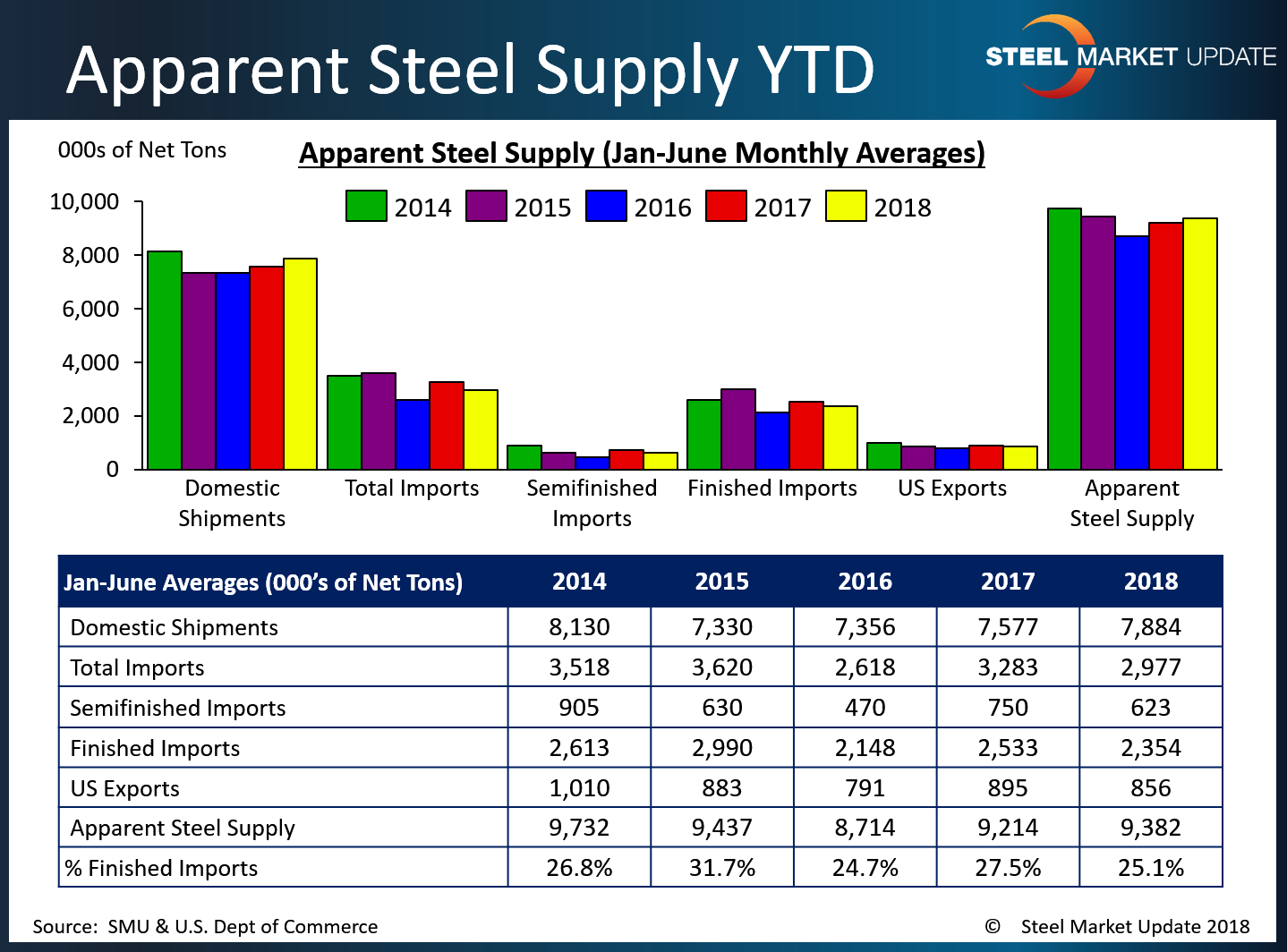

The table below shows year-to-date totals for each statistic over the last five years. The 2018 data was previously steady to higher compared to the previous two years, but is now mixed.

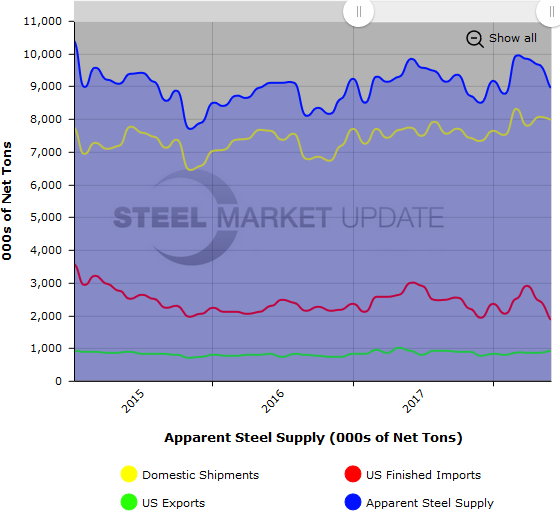

To see an interactive graphic of our Apparent Steel Supply history (example below), visit the Apparent Steel Supply page in the Analysis section of the SMU website. If you need any assistance logging in or navigating the website, contact us at info@SteelMarketUpdate.com or 800-432-3475.