Prices

October 7, 2018

August Finished Steel Imports at 2 Million Net Tons

Written by Brett Linton

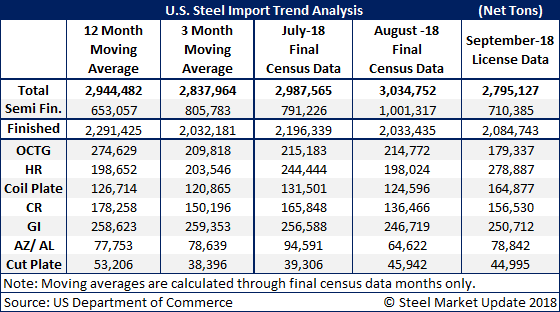

The U.S. Department of Commerce released Final Census Data on August foreign steel imports late last week. The final data shows August imports hit 3,034,752 net tons, just slightly above the 2,987,565 net tons reported for the month of July. Total imports continue to be resilient, mostly on the back of semi-finished steels (mostly slabs going to domestic mills). In August, semi’s account for one-third of the total imports with 1,001,317 net tons.

This means finished imports fell to just over 2 million net tons. You can see how each product we follow fared in the table below.

At the same time, the DOC reported license data for the month of September. September is looking like it will come in at 2.8 million tons. The drop was essentially all semi’s as they are looking like they will be around 700,000 net tons vs. 1,000,000 in August.

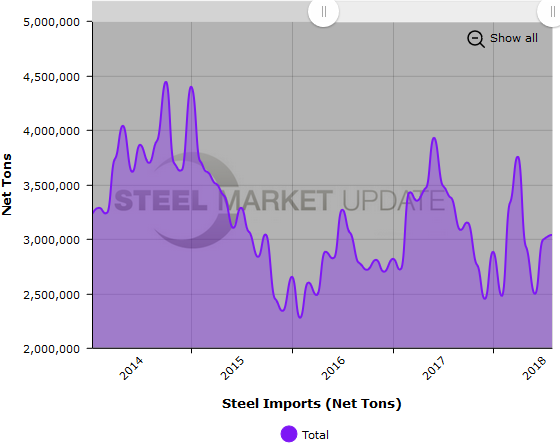

Below is a graph showing the history of total steel imports. You will need to view the graph on our website to use its interactive features; you can do so by clicking here. If you need assistance logging in to or navigating the website, please contact Brett at Brett@SteelMarketUpdate.com.