Prices

April 25, 2019

Final February Imports at 2.4M Tons; March and April Up

Written by Brett Linton

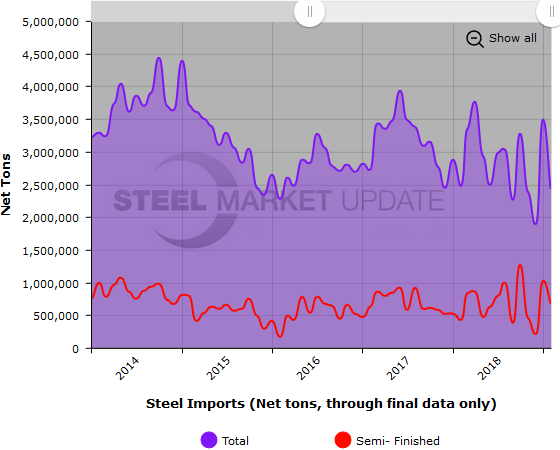

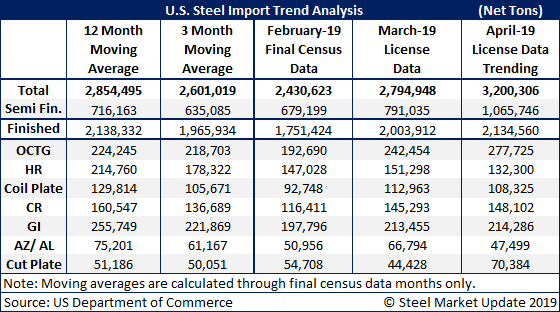

Final February steel import data was recently released by the U.S. Department of Commerce, putting the total monthly import level at 2.4 million net tons, down 30.1 percent compared to January’s 3.5 million ton high. The February figure is below both the three-month moving average (3MMA) and the 12-month moving average (12MMA).

When removing the semi-finished products from the mix (680,000 tons), the finished steel import levels drop to 1.8 million net tons, below both the 3MMA and 12MMA.

March total import license data is currently just under 2.8 million tons, a 15.0 percent increase over the prior month. After removing semi-finished imports, we get a total finished import level of just over 2 million tons.

April license data is currently trending towards 3.2 million tons, which would be a 14.5 increase over March. Semi-finished imports are trending over 1 million tons for the month, which could be a six-month high if they remain at that level. Imports of finished products are at 2.1 million tons.

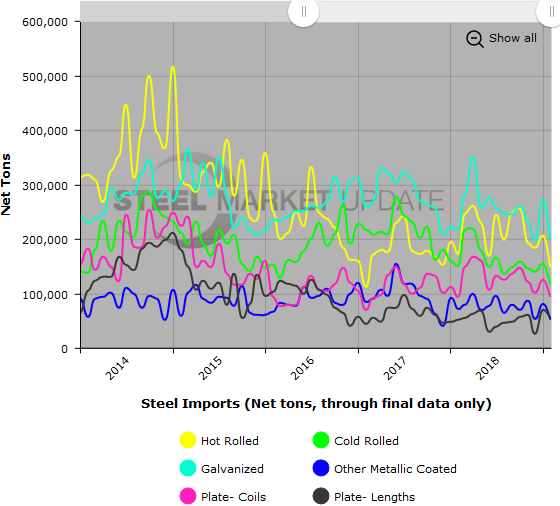

Below are two graphs covering steel imports through February 2019 figures. You will need to view the graphs on our website to use their interactive features; you can do so by clicking here. If you need assistance logging into or navigating the website, contact us at info@SteelMarketUpdate.com.