Prices

June 25, 2019

Raw Materials Prices: Iron Ore, Coke, Scrap, Pig Iron, Zinc

Written by Peter Wright

Steel Market Update is pleased to share this Premium content with Executive level members. For more information on upgrading to a Premium-level subscription, email Info@SteelMarketUpdate.com.

The price of iron ore has surged as scrap has declined benefiting the EAF producers in the U.S. over the integrated mills.

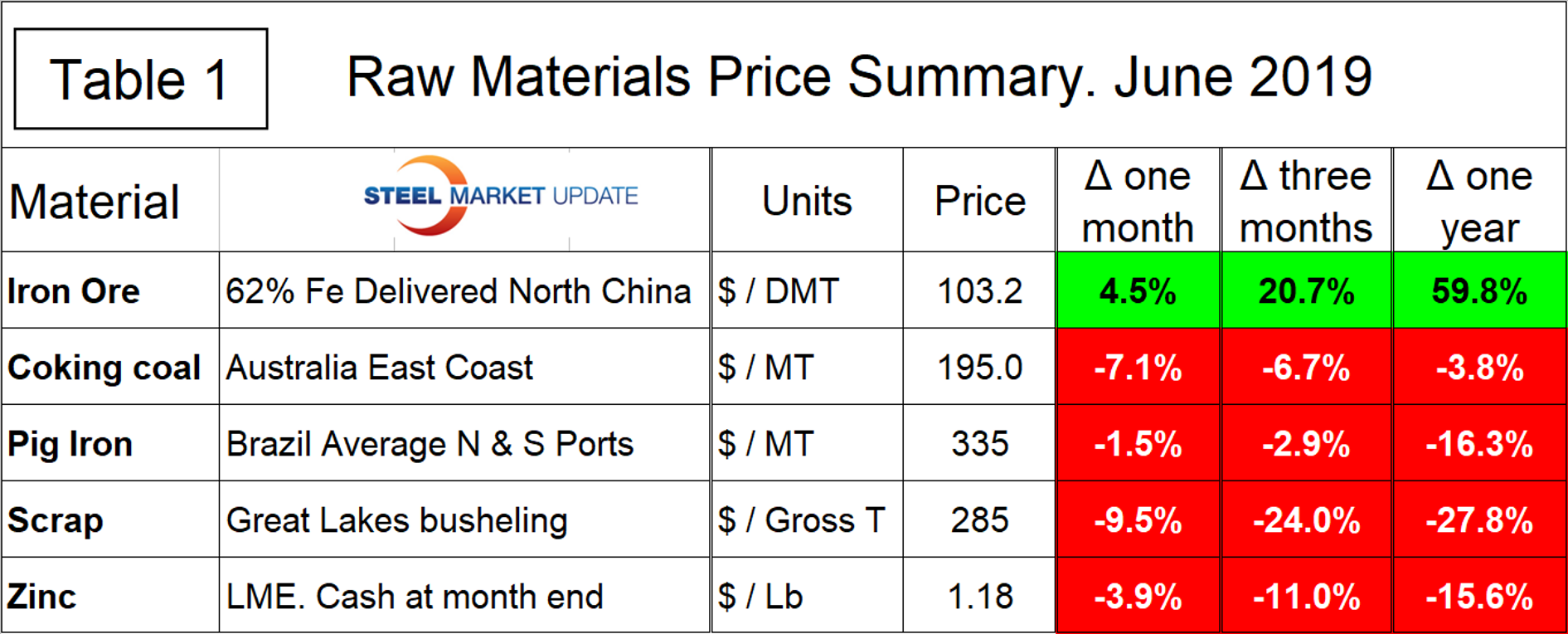

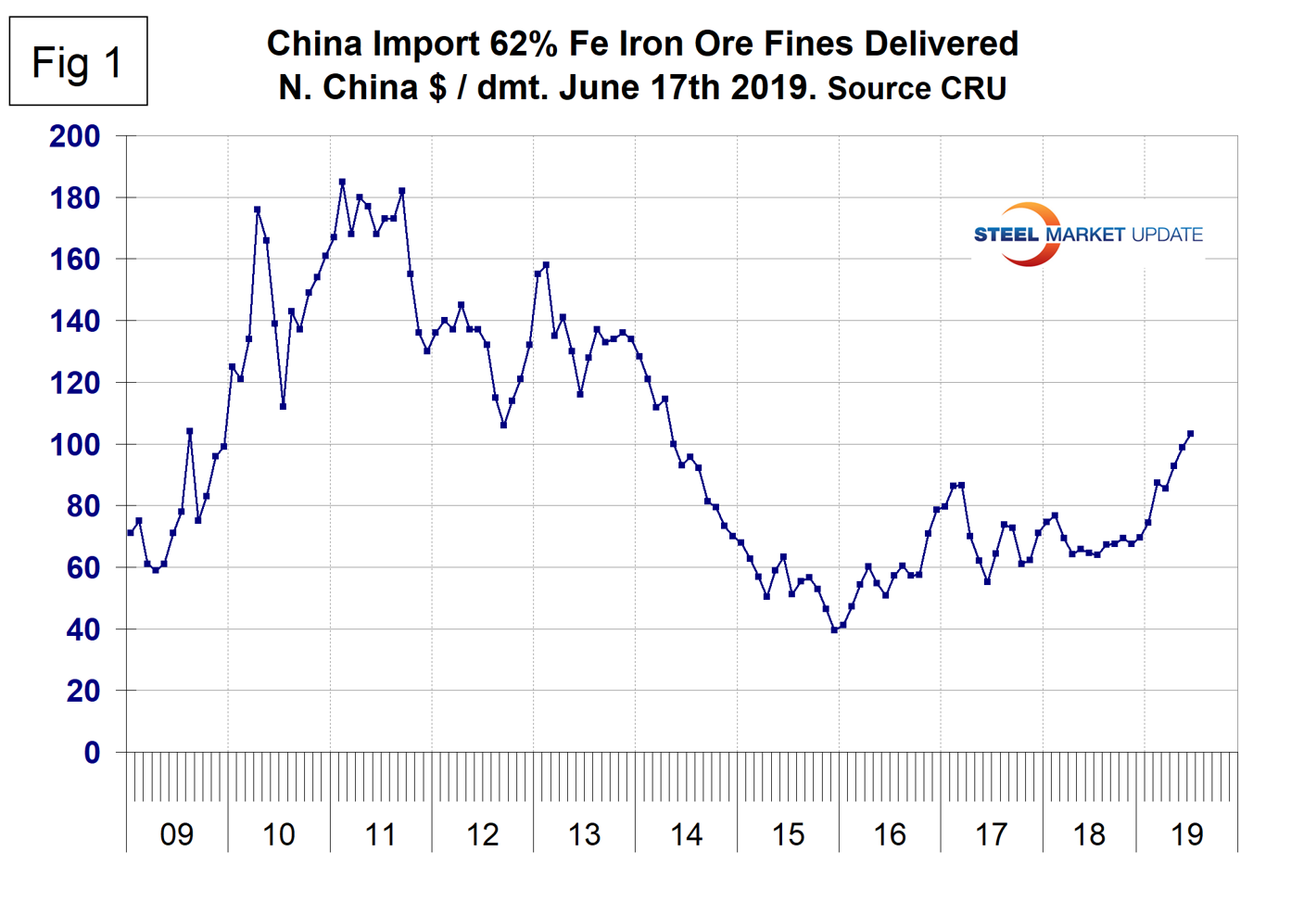

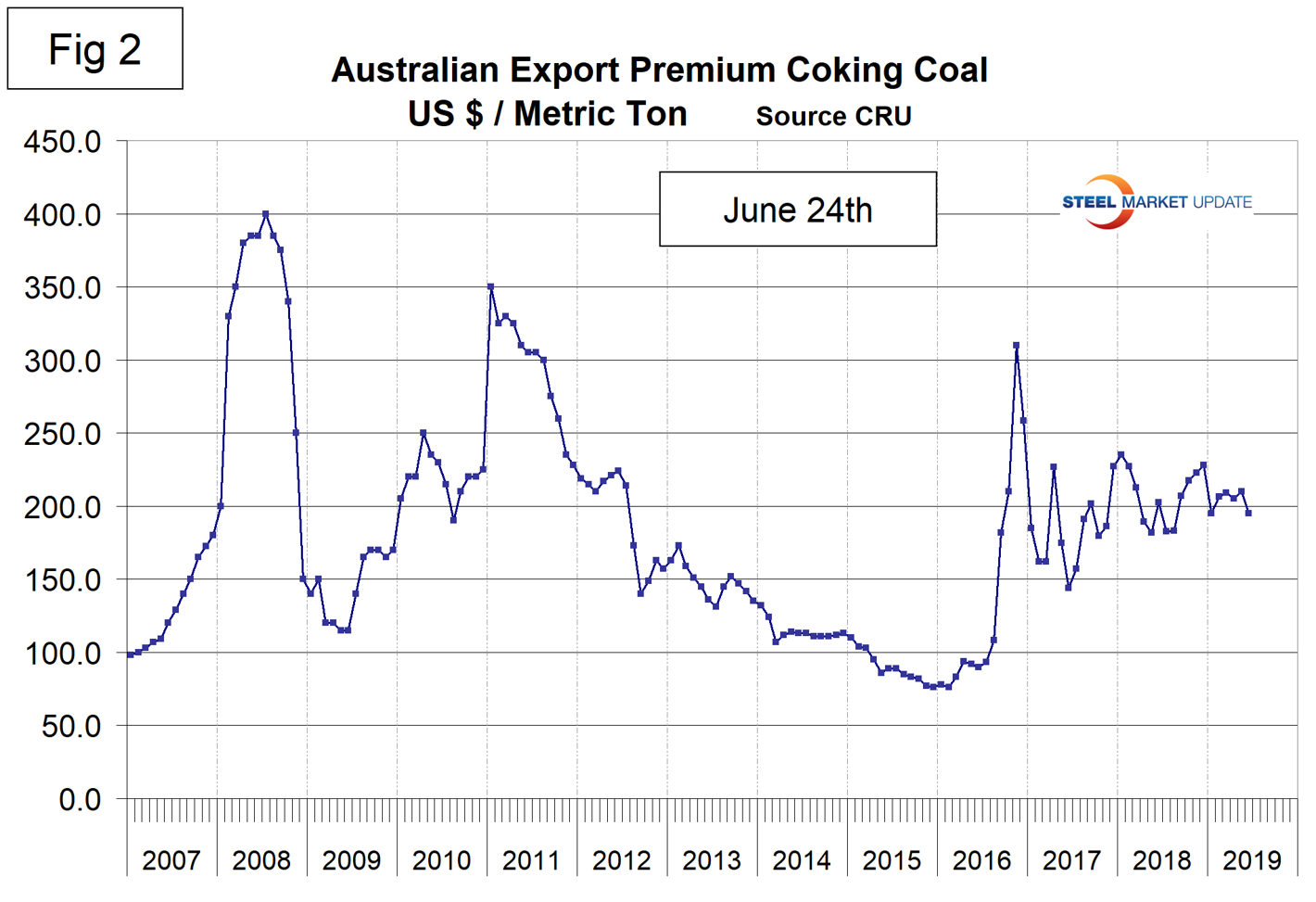

Table 1 summarizes the price changes through June of the five materials considered in this analysis. It reports the month/month, 3 months/3 months and 12 months/12 months changes and tells us that iron ore and scrap have moved in opposite directions this year and coking coal, pig iron and zinc prices have declined in all three time frames.

Iron Ore

Based on CRU’s data, the weekly average spot price of 62% fines delivered North China was $103.20 per dry metric ton on June 17. The price has increased every month this year and is up from $69.50 in mid-January. Figure 1 shows the price of 62% Fe delivered North China since January 2009. The price of ore has broken out of the $20 range that prior to February 2019 had existed for a year and a half.

From S&P Dow Jones Indices, June 13: “Prior to the recent rally, the S&P GSCI Iron Ore was relatively range-bound for two years due to competing macro themes. To ease the burden of U.S. tariffs and to support the slowing economy, Beijing announced a variety of stimulus measures focused on boosting its industrial complex. China currently purchases approximately two-thirds of seaborne iron ore. As has been seen in the last few years with each global growth scare, the People’s Bank of China has not hesitated to turn on its stimulus levers, which historically have been ways to increase funding for construction and infrastructure projects. The S&P GSCI Iron Ore is highly correlated to Chinese economic indicators such as real estate investment, industrial production, and steel production. Several of these indicators spiked in Q1 2019 just as iron ore prices started to rise. It is worth noting that the most recent industrial production number dropped to a five-year low of 5%. To make matters worse, supply has been drastically curtailed in recent months. Inventories held globally have been reduced and are on pace to fall to five-year lows within the next few months. The Vale dam collapse in Brazil in late January 2019 and a cyclone in Australia in March 2019 reduced supply from the world’s two largest iron ore exporters. Shipments from Australia have largely returned to normal, but it is likely that Brazilian iron ore exports will be constrained for an extended period of time. Imported iron ore stock at Chinese ports fell to a 2.5-year low of 121.6mm metric tons in mid-June, 2019 according to Steelhome.”

Coking Coal

The price of premium low volatile coking coal FOB east coast of Australia declined in January and has been trading in a narrow range for the first half of 2019. The June price is $195 per metric ton, down from $210 in May (Figure 2).

Pig Iron

Most of the pig iron imported into the U.S. currently comes from Russia, Ukraine and Brazil with additional material from South Africa and Latvia. In this report, we summarize prices out of Brazil and average the FOB value from the north and south ports. The price had a recent peak of $400 per metric ton in May and June last year and had fallen to $335 in June this year (Figure 3). The average price in June was 16.3 percent lower than in June last year.

Scrap

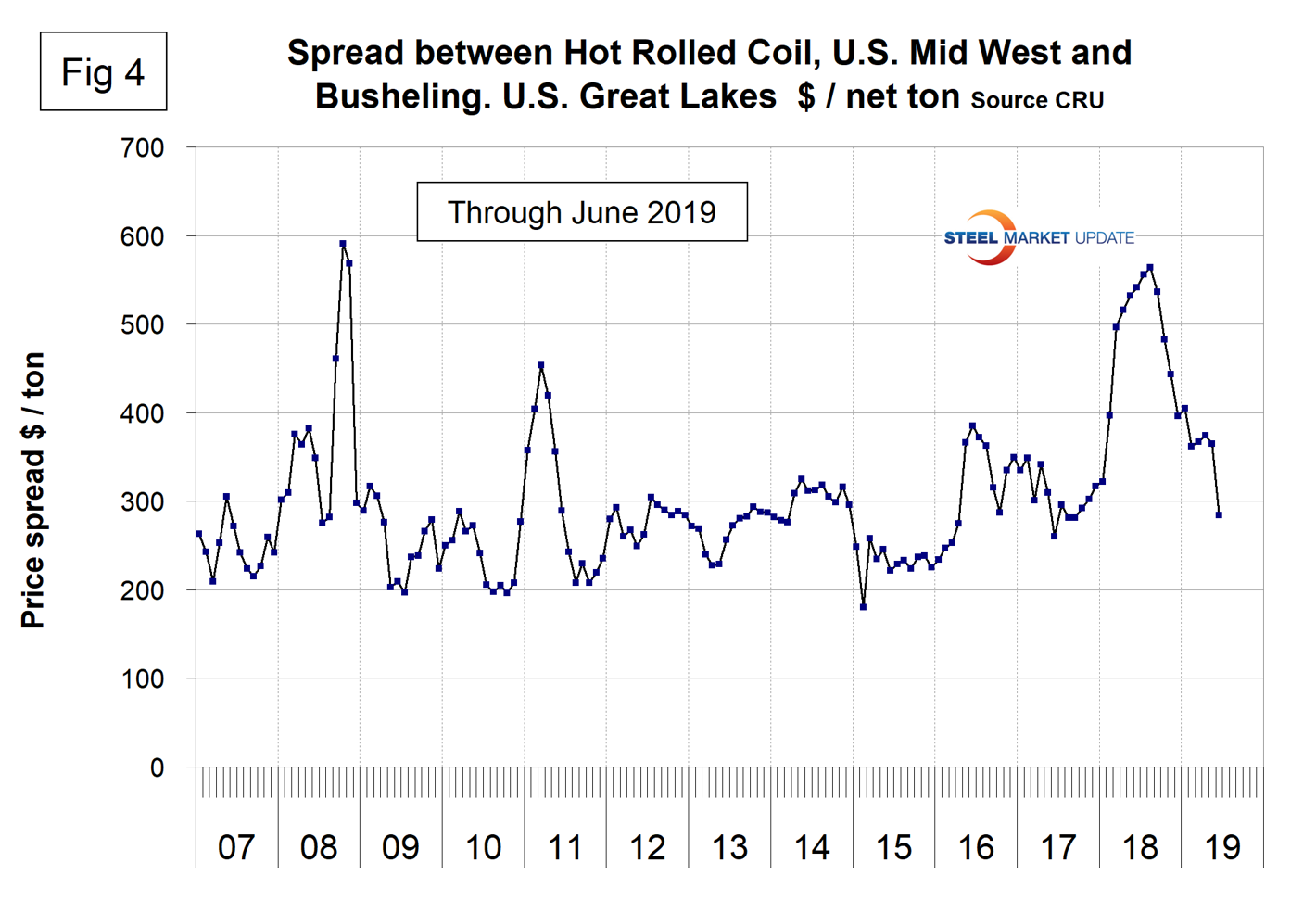

To put this raw materials commentary into perspective, we include here Figure 4, which shows the spread between busheling in the Great Lakes region and hot rolled coil Midwest U.S. through mid-June 2019, both in dollars per net ton. The spread has collapsed from $564 in August last year to $285 in June 2019 and is now in a range more historically normal for the last 15 years.

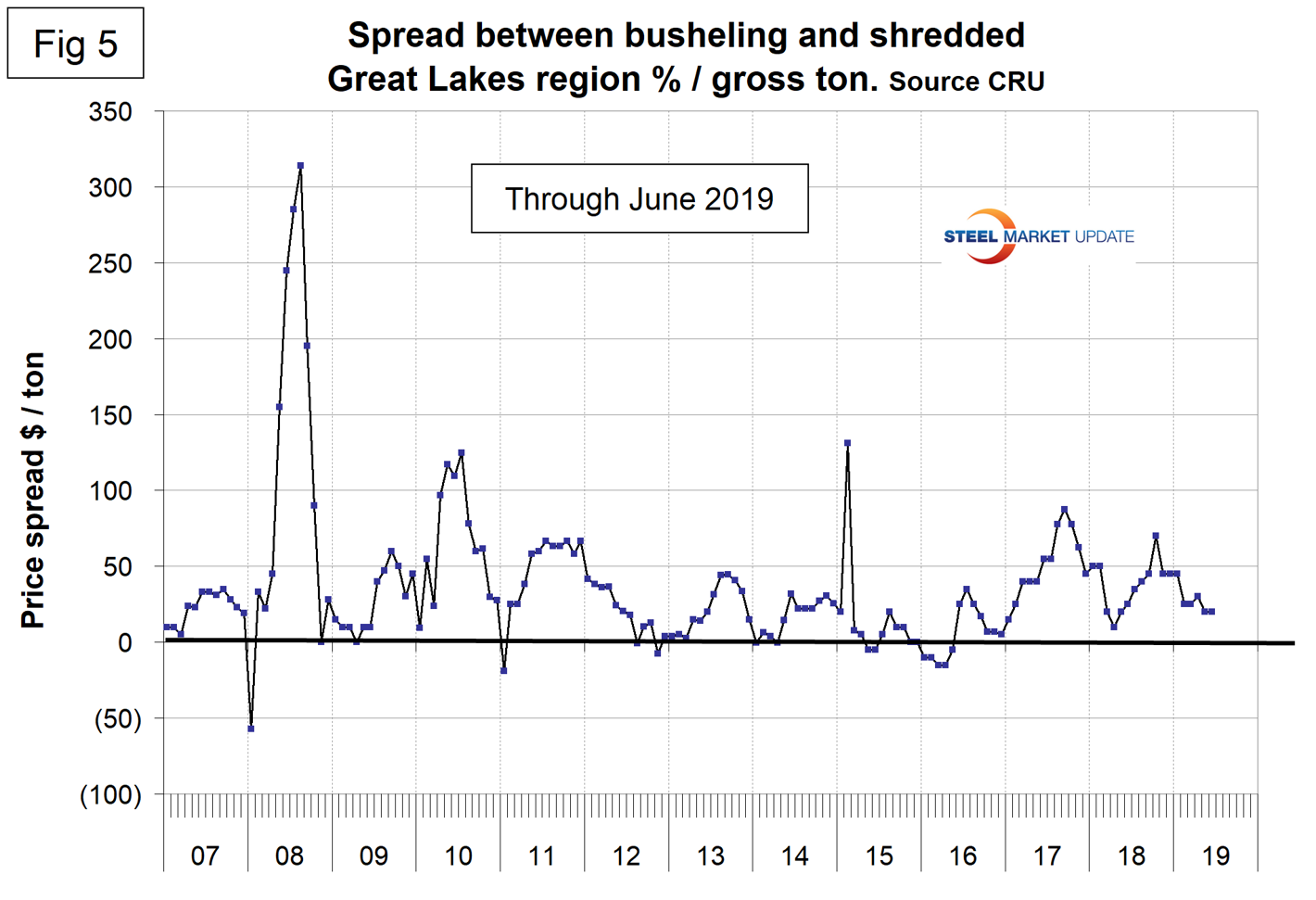

Figure 5 shows the relationship between shredded and busheling both priced in dollars per gross ton in the Great Lakes region. This spread was $20 in May and June and was the lowest since April last year.

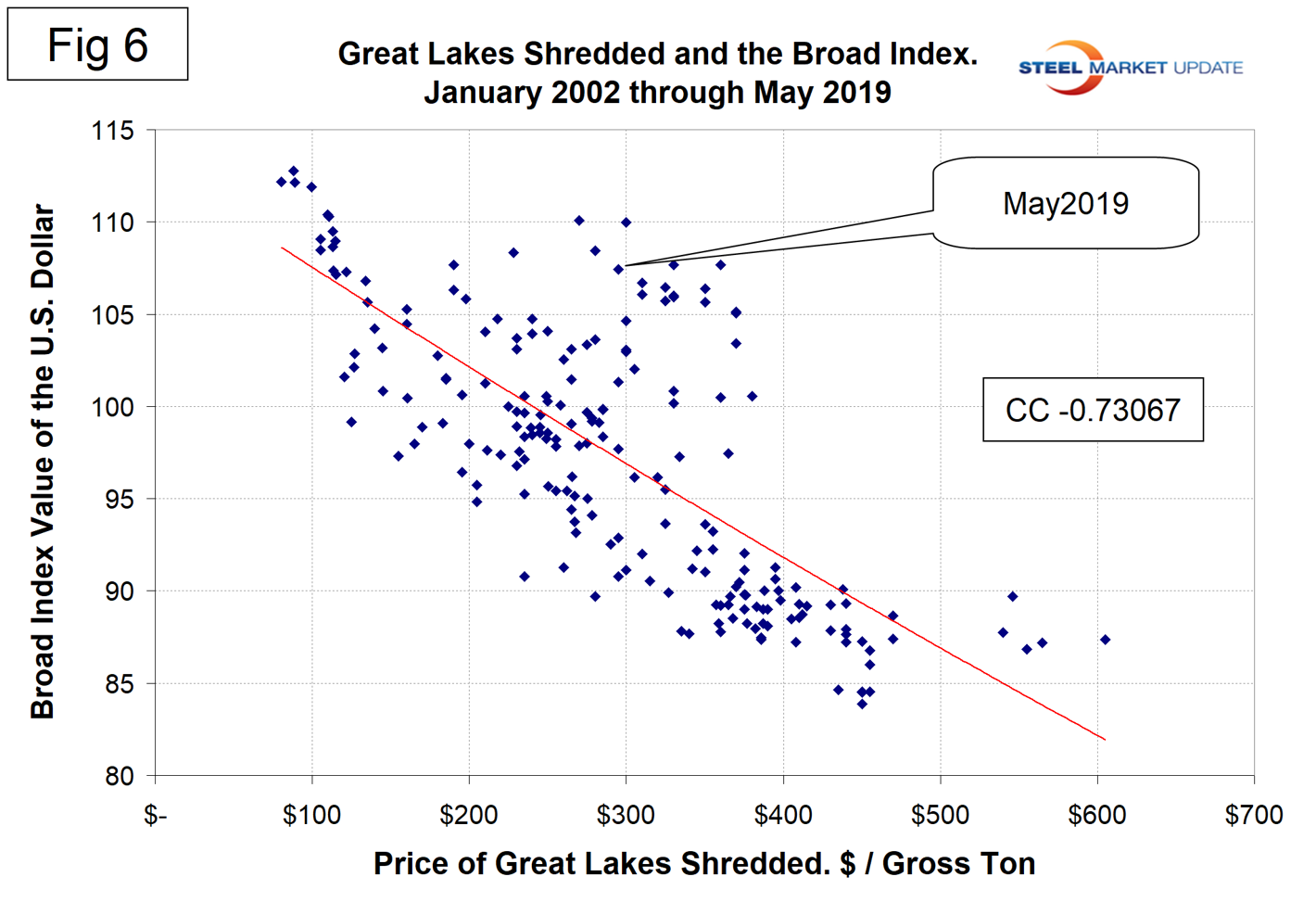

Figure 6 is a scatter gram of the price of Chicago shredded and the monthly Broad Index value of the U.S. dollar as reported by the Federal Reserve. The latest data for the monthly Broad Index was May. This is a causal relationship with a negative correlation of over 73 percent, but recent data is further from the norm than at any time in the last seven years.

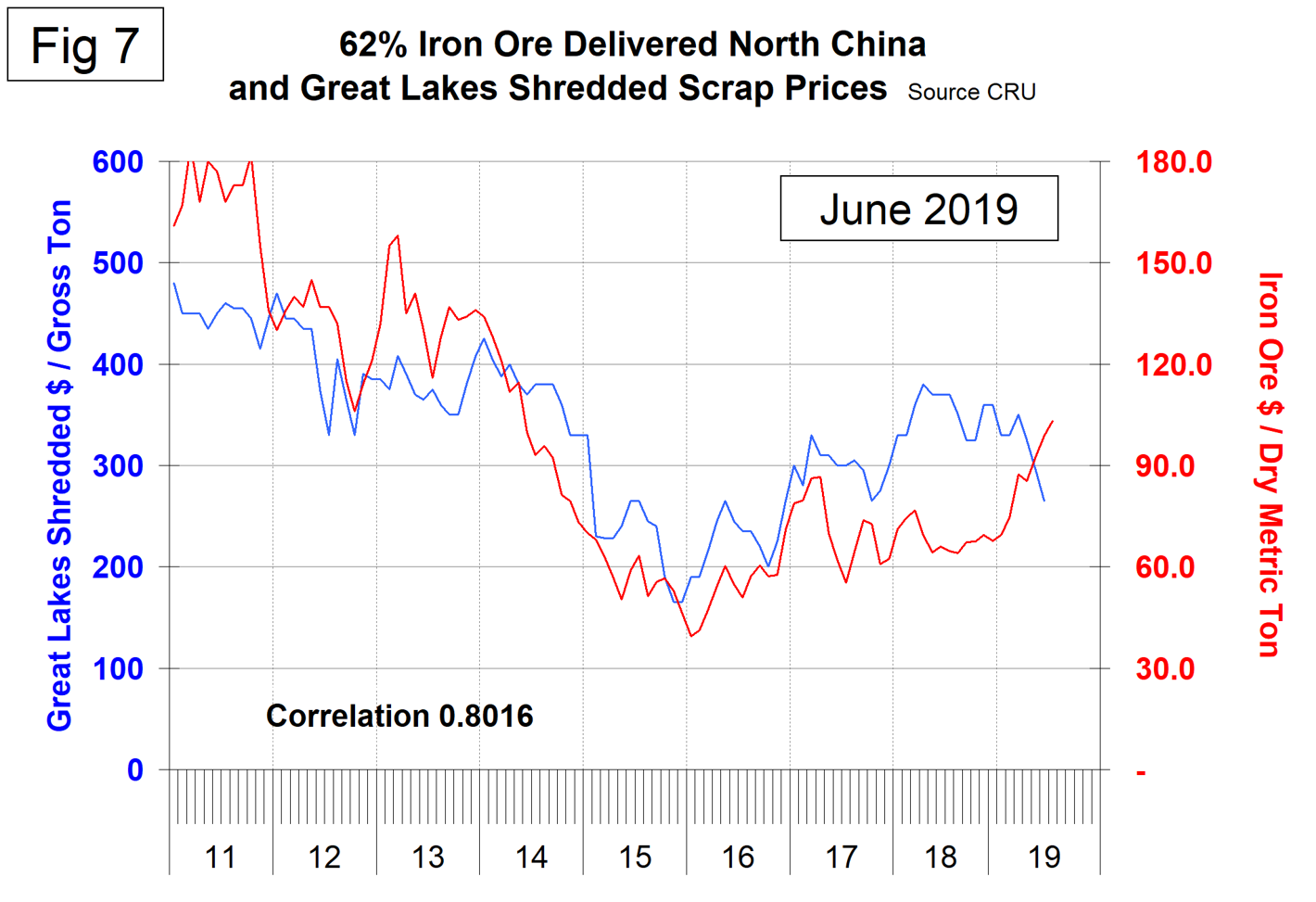

There is a long-term relationship between the prices of iron ore and scrap. Figure 7 shows the prices of 62% iron ore fines delivered North China and the price of shredded scrap in the Great Lakes region through mid-June 2019. The correlation since January 2006 has been over 80 percent. There has been a very unusual divergence in these prices since Q2 2017 that benefited the integrated producers, but that advantage has now reversed.

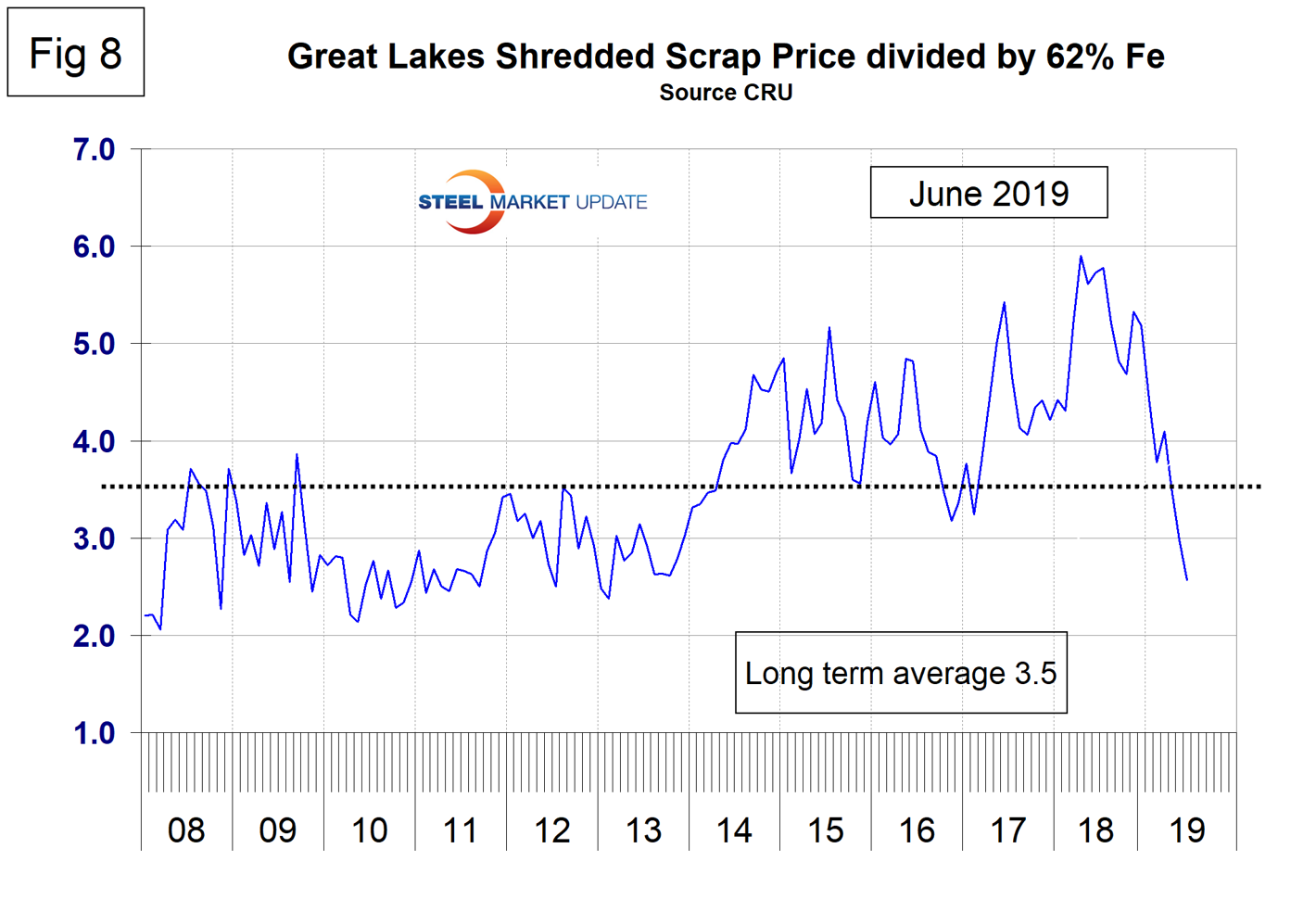

In the last 10 years, scrap in dollars per gross ton has been on average 3.4 times as expensive as ore in dollars per dry metric ton (dmt). The ratio has been erratic since mid-2014, but at 2.6 in June has reverted to a level not seen since 2013 (Figure 8). A high ratio benefits the domestic integrated producers, and since Chinese steel manufacture is 95 percent BOF, China is more competitive on the global steel market when this ratio is high. In the last four years, there have been times when China could supply semi-finished to the global market at prices competitive with scrap. This is no longer the case.

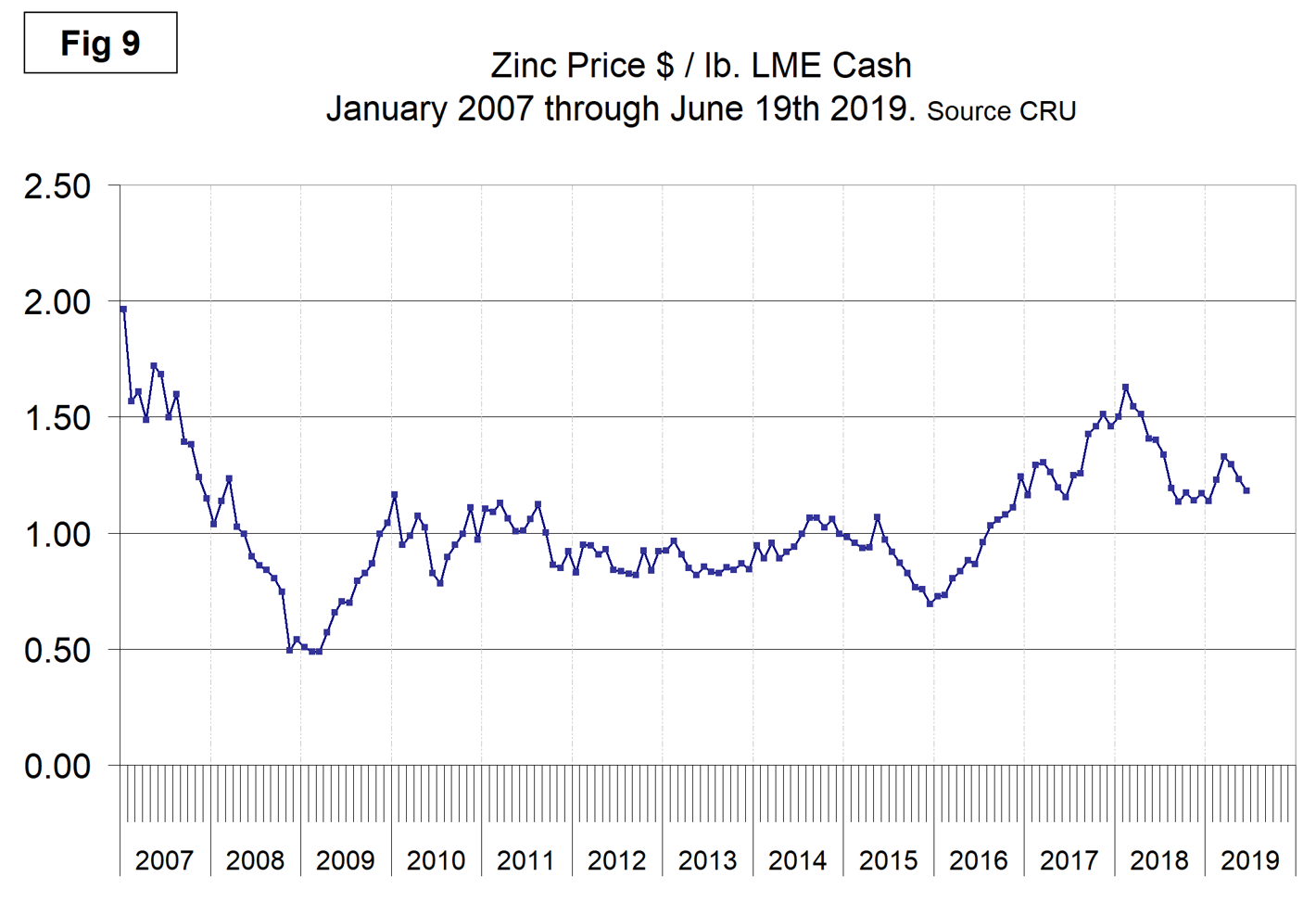

Zinc

The LME cash price for zinc mid-month is shown in Figure 9. The latest data is for June 17 when the price was $1.18 per pound. On May 30, Reuters reported: “The rolling zinc squeeze has upended expectations of a speedy collapse in both spreads and outright prices, but there remains a strong consensus that the market will start to loosen up as the year progresses. The problem is that zinc has been defying expectations for many months. Those trying to capture the shift to surplus by shorting the metal are now paying the painful spreads price. Those still tempted to go short should pay close attention to China’s strong imports and the conspicuous lack of fresh deliveries into LME warehouses. All the available evidence suggests that the supply of refined metal is still struggling to match demand, with ILZSG estimating a global supply shortfall of 15,000 tonnes in the first quarter of 2019. LME spreads are transmitting the same message, even as the outright price weakens under the weight of macroeconomic negativity. The game, in other words, is not yet up and it won’t be until the market sees tangible evidence that the zinc market is genuinely transitioning from supply deficit to surplus.”

Zinc is the fourth most widely used metal in the world after iron, aluminum and copper. Its primary uses are 60 percent for galvanizing steel, 15 percent for zinc-based die castings and about 14 percent in the production of brass and bronze alloys.

SMU Comment: There has been a reversal of fortunes in the U.S., which began last November benefiting the EAF producers over the integrateds. Since March the price of iron ore has increased by 20.7 percent and the price of busheling in the Great Lakes region has declined by 24.0 percent. The price of imported pig iron has also declined to the benefit of the EAF producers.