Prices

July 26, 2019

Raw Materials Prices: Iron Ore, Coking Coal, Pig Iron, Scrap, Zinc

Written by Peter Wright

The surge in the price of iron ore and the decline in the price of scrap continued through mid-July, benefiting the EAF producers in the U.S. over the integrated mills

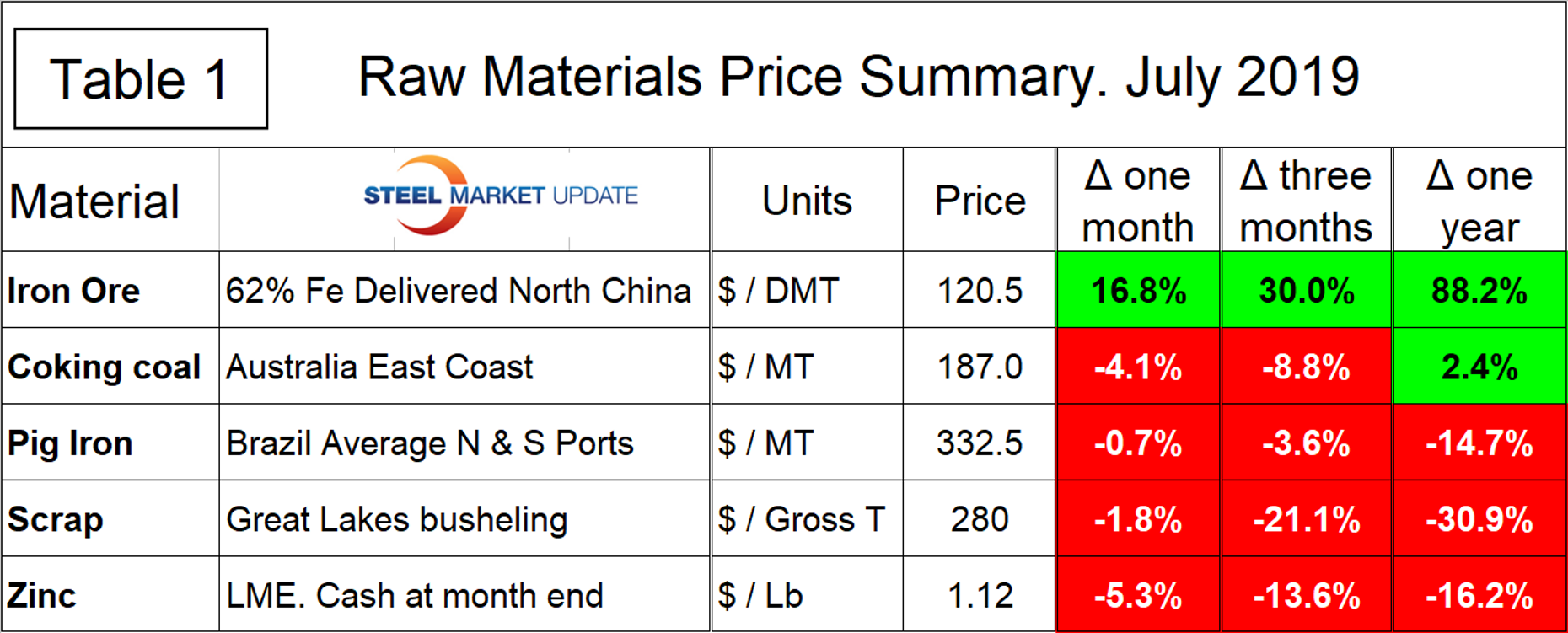

Table 1 summarizes the price changes through July of the five materials considered in this analysis. It reports the month/month, 3 months/3 months and 12 months/12 months changes and tells us that iron ore and scrap have moved in opposite directions for over a year and coking coal, pig iron and zinc prices have declined in the last three months.

Iron Ore

Based on CRU’s data, the weekly average spot price of 62% fines delivered North China was $120.50 per dry metric ton on July 17, up from $103.20 on June 17. The price has increased every month this year and is up from $69.50 in mid-January. Figure 1 shows the price of 62% Fe delivered North China since January 2009. The price of ore has broken out of the $20 range that prior to February 2019 had existed for a year and a half.

Coking Coal

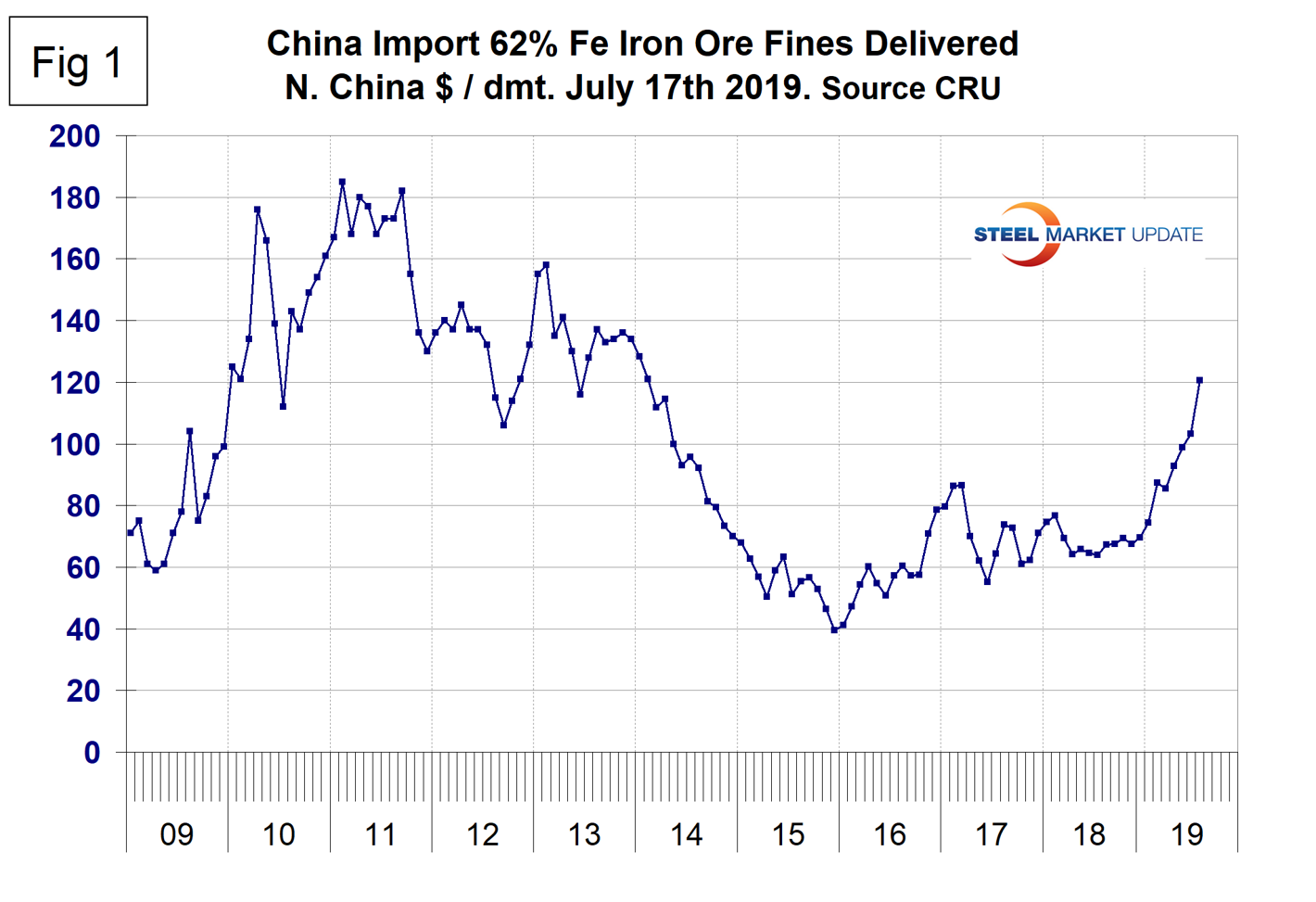

The price of premium low volatile coking coal FOB east coast of Australia declined in June and July and has been trading in a $23 range for the first half of 2019. The July price is $187 per metric ton, down from $210 in May (Figure 2).

Pig Iron

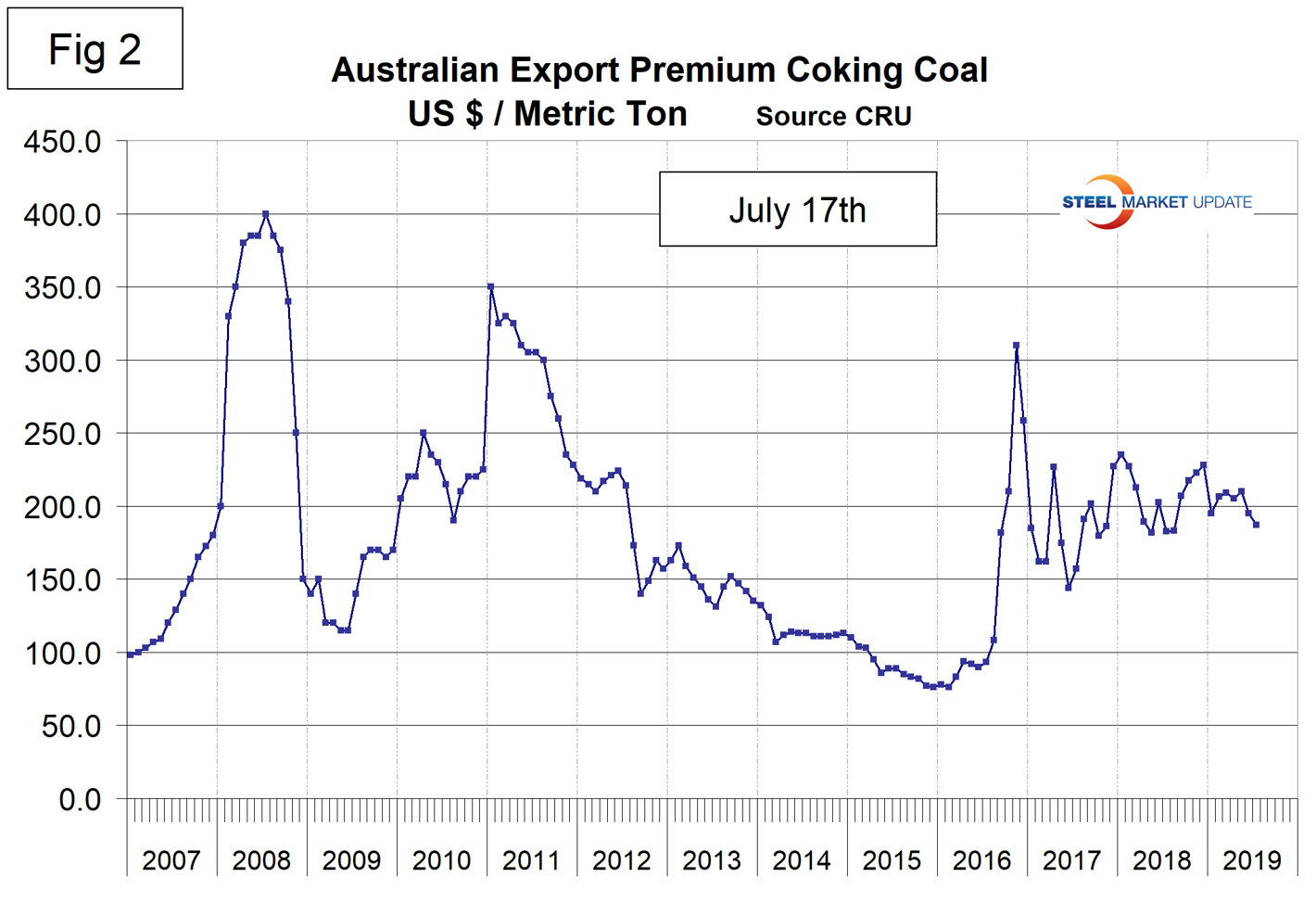

Most of the pig iron imported to the U.S. currently comes from Russia, Ukraine and Brazil with additional material from South Africa and Latvia. In this report, we summarize prices out of Brazil and average the FOB value from the north and south ports. The price had a recent peak of $400 per metric ton in May and June last year and had fallen to $332.50 in July this year. The average price in July was 14.7 percent lower than in July last year (Figure 3).

Scrap

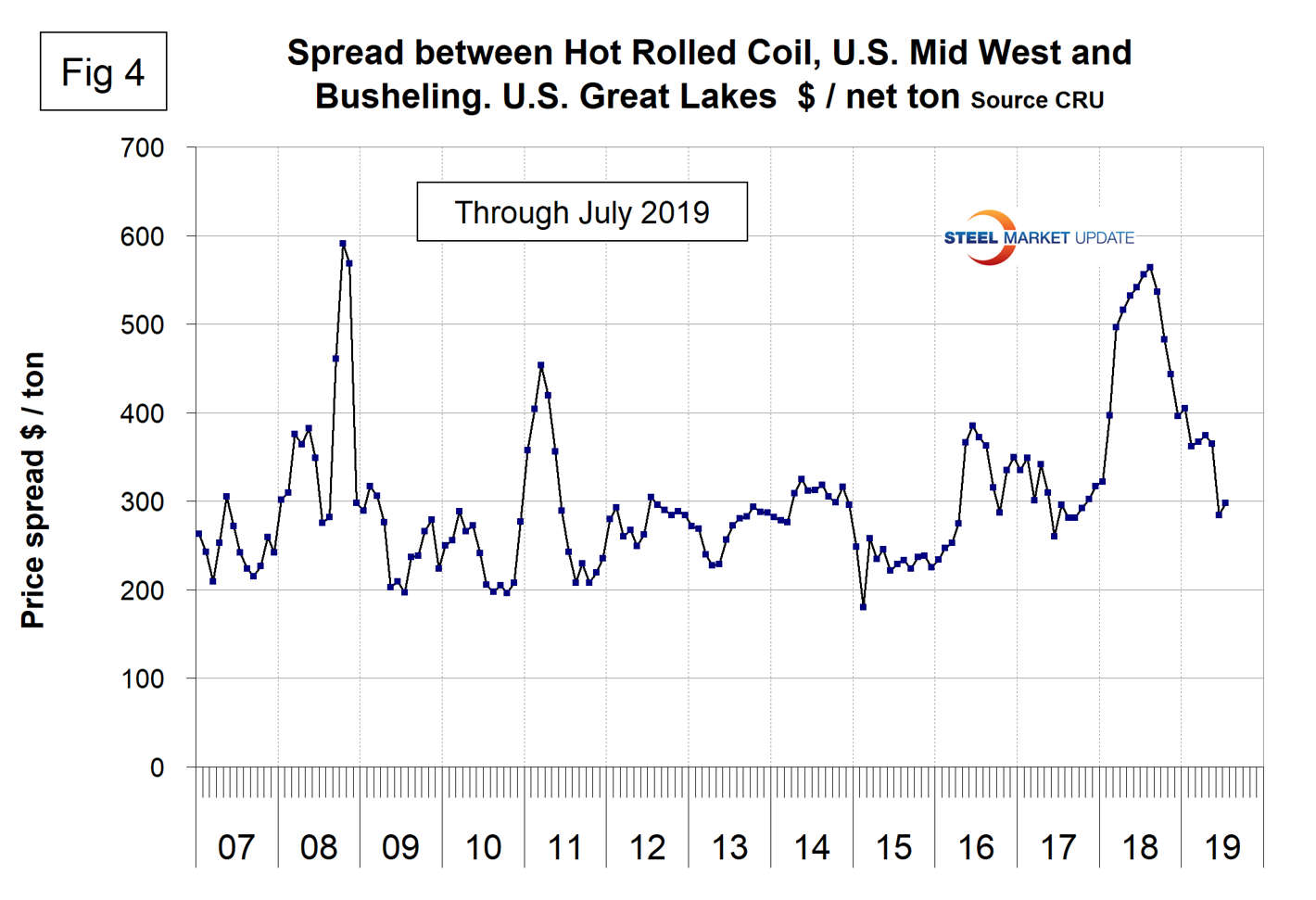

To put this raw materials commentary into perspective, we include here Figure 4, which shows the spread between busheling in the Great Lakes region and hot rolled coil Midwest U.S. through mid-July 2019, both in dollars per net ton. The spread has collapsed from $564 in August last year to $298 in July 2019 and is now in a range more historically normal for the last 12 years.

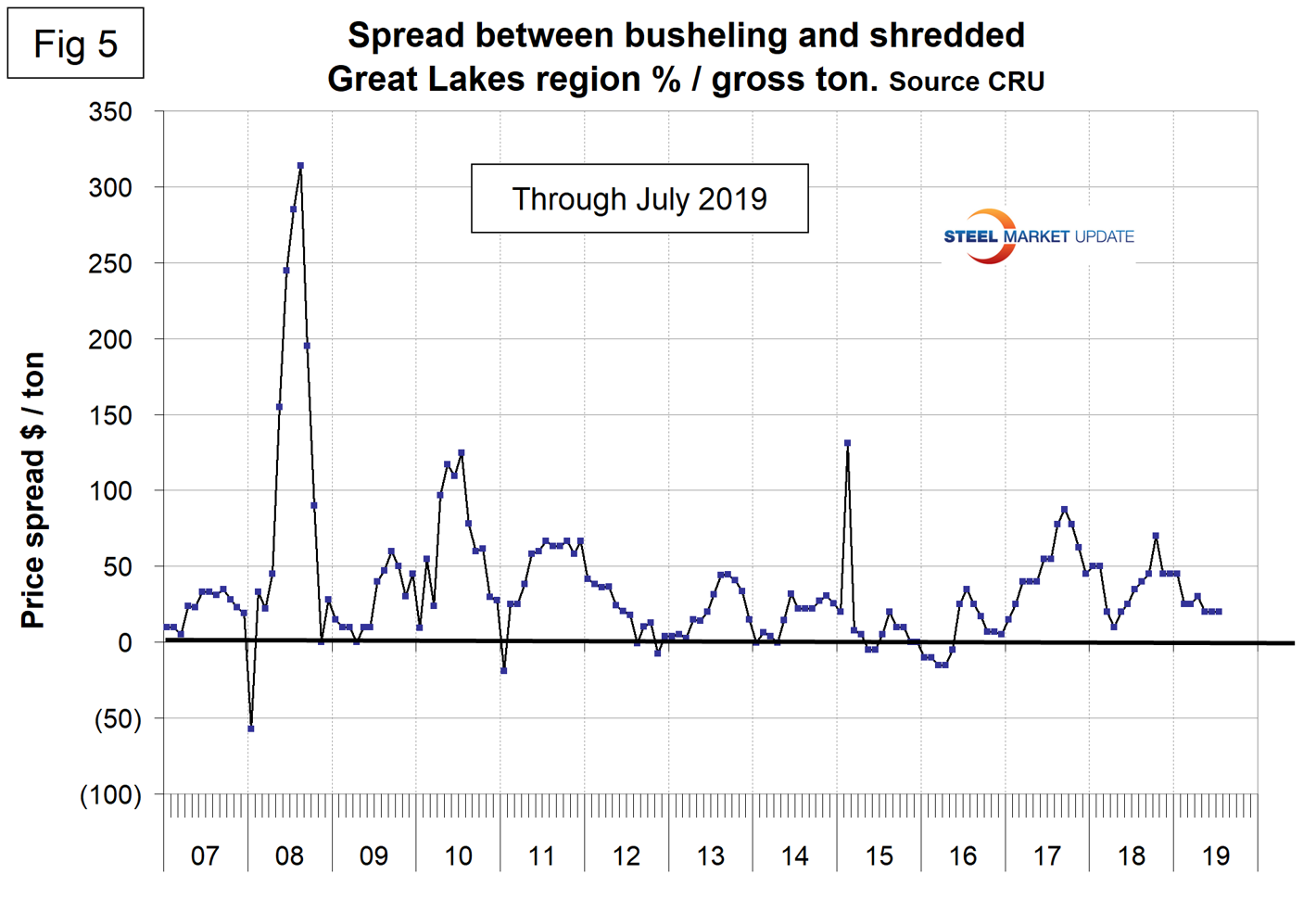

Figure 5 shows the relationship between shredded and busheling both priced in dollars per gross ton in the Great Lakes region. This spread was $20 in May, June and July and was the lowest since April last year.

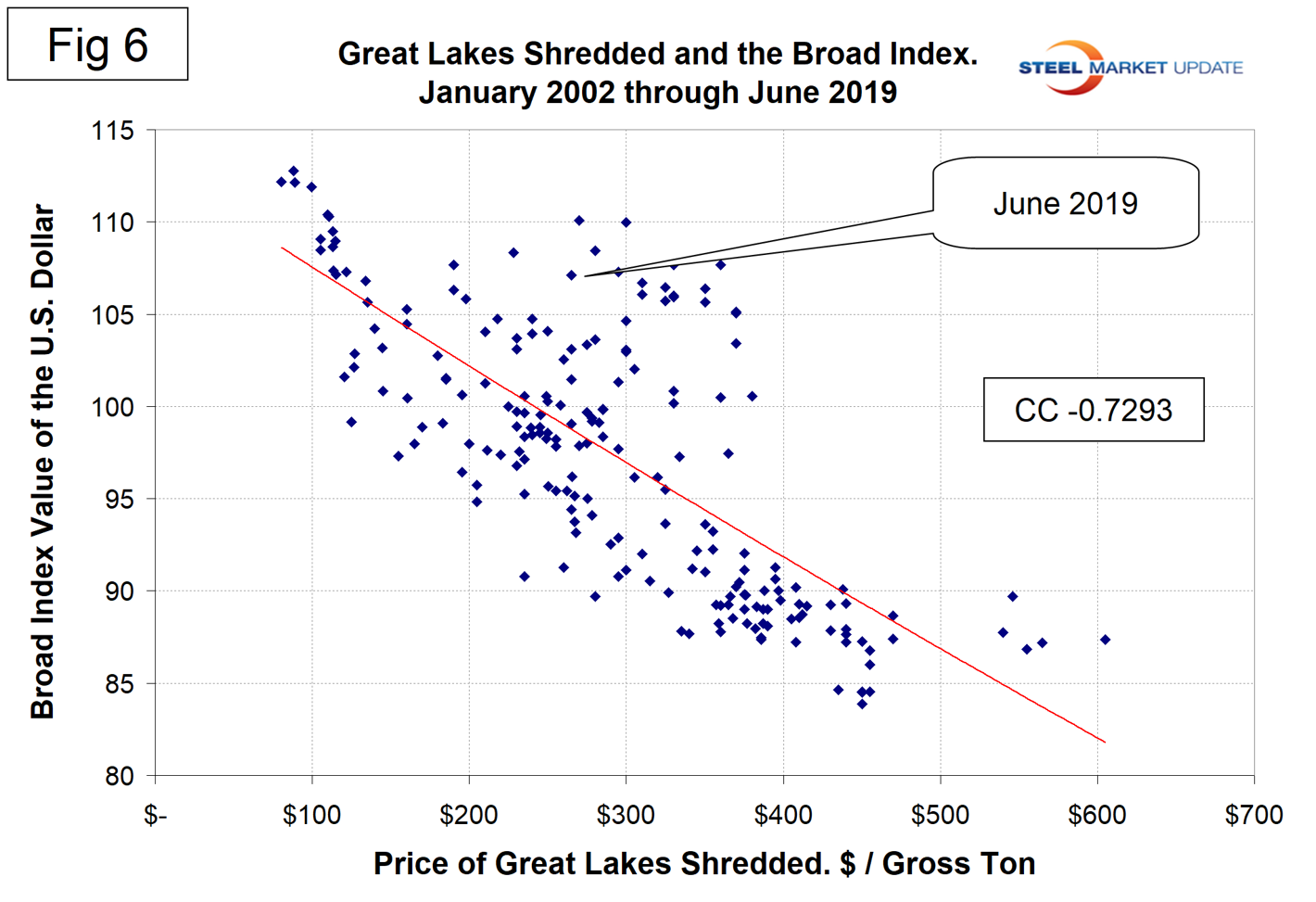

Figure 6 is a scatter gram of the price of Chicago shredded and the monthly Broad Index value of the U.S. dollar as reported by the Federal Reserve. The latest data for the monthly Broad Index was June. This is a causal relationship with a negative correlation of almost 73 percent.

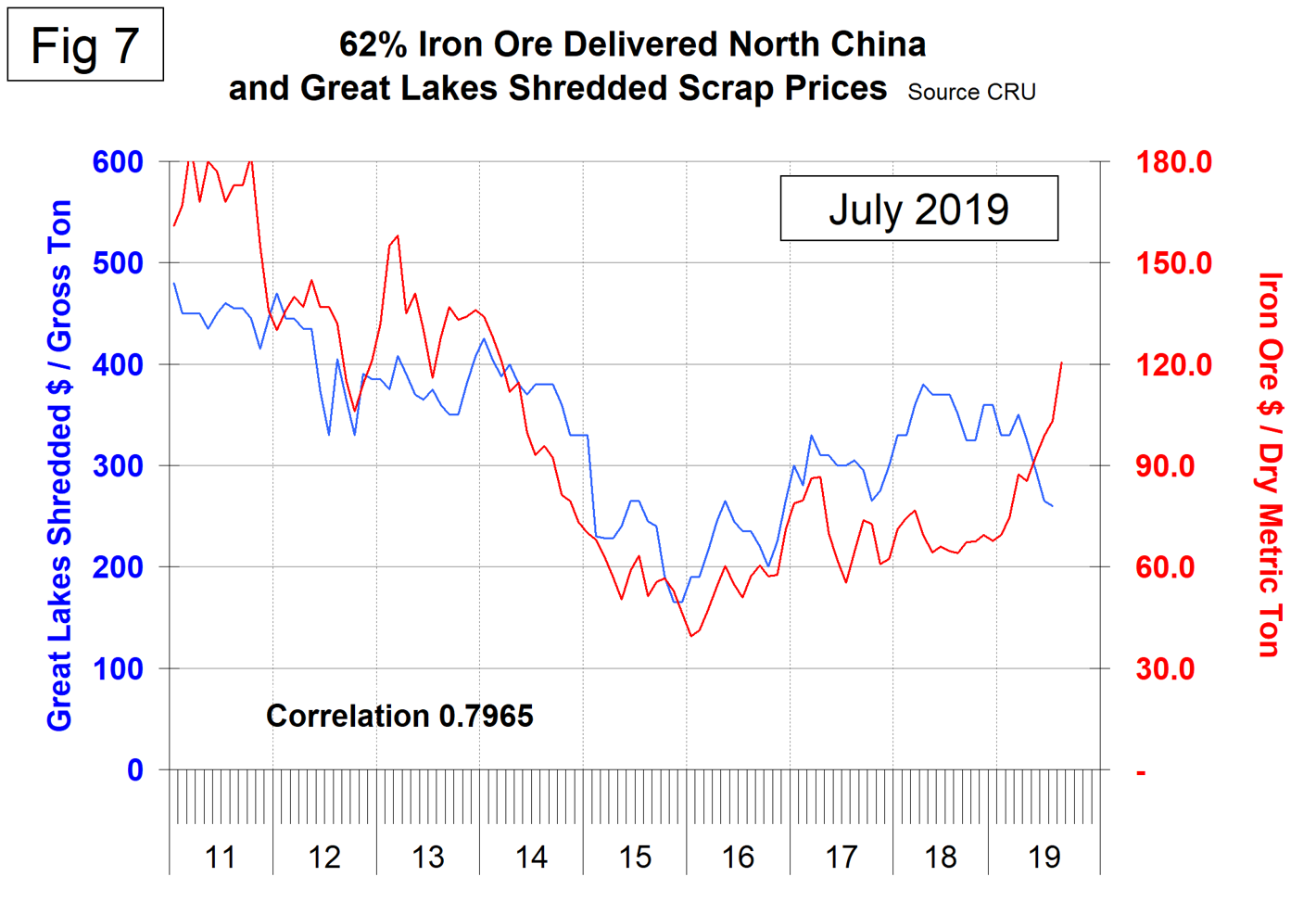

There is a long-term relationship between the prices of iron ore and scrap. Figure 7 shows the prices of 62 percent iron ore fines delivered North China and the price of shredded scrap in the Great Lakes region through mid-July 2019. The correlation since January 2006 has been over 79 percent. There was a very unusual divergence in these prices in 2017 and 2018 that benefited the integrated producers, but that advantage has now reversed to the extent that the EAF producers have the greatest advantage since November 2011.

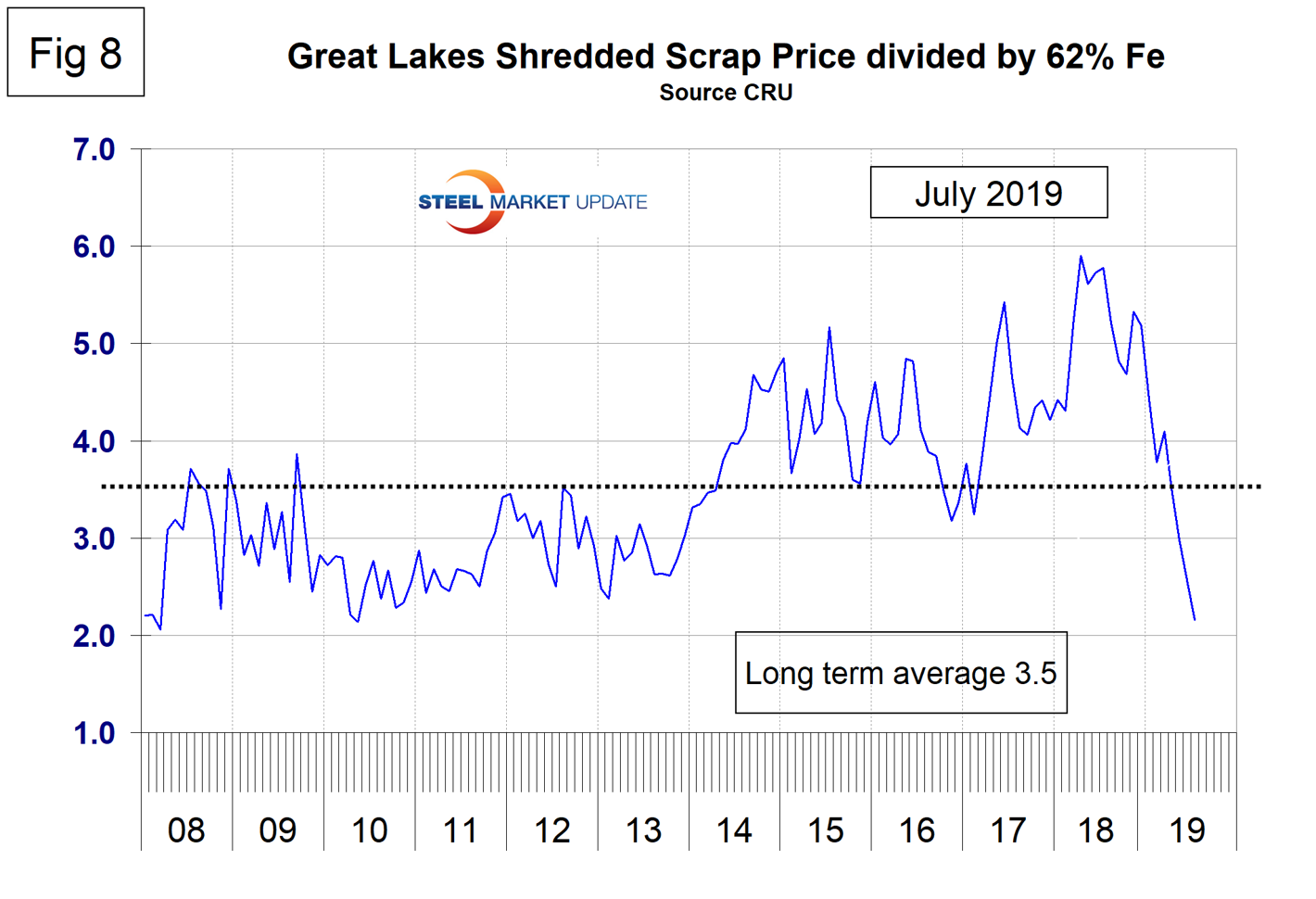

In the last 10 years, scrap in dollars per gross ton has been on average 3.4 times as expensive as iron ore in dollars per dry metric ton (dmt). The ratio has been erratic since mid-2014, but at 2.2 in July has reverted to a level not seen since 2010 (Figure 8). A high ratio benefits the domestic integrated producers and a low ratio benefits the EAF producers.

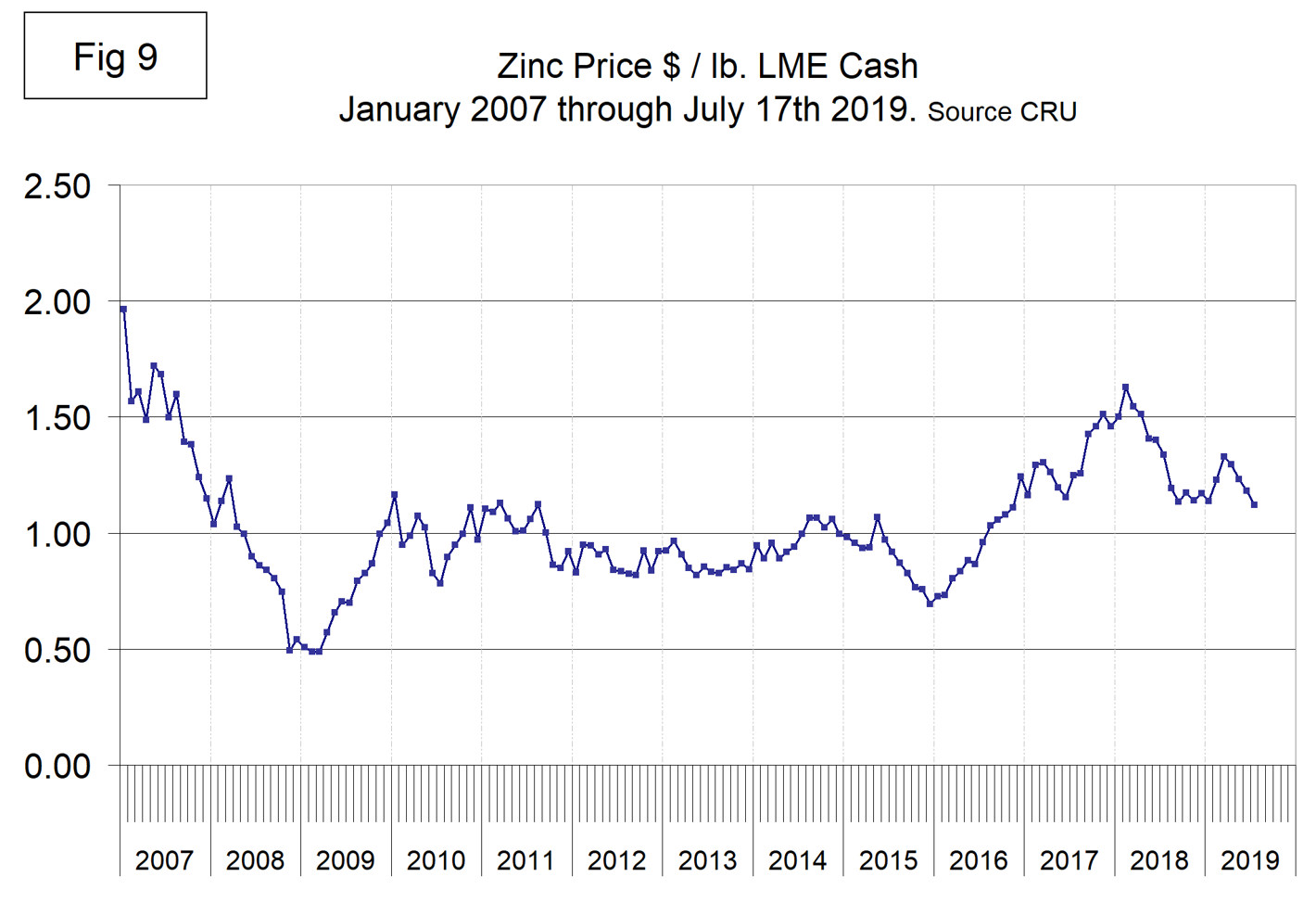

Zinc

The LME cash price for zinc mid-month is shown in Figure 9. The latest data is for July 17 when the price was $1.12 per pound, down from $1.33 in mid-March.

Zinc is the fourth most widely used metal in the world after iron, aluminum and copper. Its primary uses are 60 percent for galvanizing steel, 15 percent for zinc-based die castings and about 14 percent in the production of brass and bronze alloys.

SMU Comment: The remarkable reversal of fortunes in the U.S., which began last November benefiting the EAF producers over the integrateds, continued through July. From an iron units point of view, the EAF producers are now better off than at any time since 2010. Since January this year, the international price of iron ore has increased by 61.7 percent and the price of busheling in the Great Lakes region has declined by 25.3 percent. The price of imported pig iron has also declined to the benefit of the EAF producers.