Overseas

March 5, 2020

CRU: Sheet Markets Steady in U.S. and Europe, But Asia Still Bearish

Written by George Pearson

Sheet prices in the U.S. Midwest market fell by $5-9 /s.ton, w/w with HR coil losing the most, assessed at $560 /s.ton. These prices reflect transactions from last week, which were primarily conducted ahead of recently announced mill price increases. While prices fell, the overall volume component fell at a faster rate. Until the price increase was announced, prices had been on a downtrend as service center buyers continued to limit purchase activity, with near-term demand well-covered by inventory or material already on order. The mill price increase comes ahead of somewhat bullish expectations for the March scrap settlement. Overall, steel market participants remain concerned about domestic and regional industrial activity as well as how forthcoming supply chain disruptions may affect end use demand.

USS-POSCO Industries (UPI) announced a $40 /s.ton price increase for all sheet products, which was in line with Midwest mill price increases. California Steel Industries (CSI) closed its April book on March 3. Customers are speculating CSI may announce an increase when its May order book opens. Due to longer lead times, price increase announcements and strength in the construction market, imports are becoming more attractive, particularly for HDG coil. Several companies reported they are expecting import shipments between April and June. Customers expressed hope that U.S. Steel’s buyout of POSCAL’s 50 percent ownership of UPI, which was finalized Feb. 29, and its involvement in Big River Steel, will lead to opportunities for new product availability and quicker lead times.

Europe

Overall, prices are creeping higher in Europe on buying in the north and low import penetration. German HR coil rose €2 /t to €479 /t this week, supported by consistent restocking requirements. We have heard several bookings at €470-480 /t in the last two weeks, and offers since the middle of last week have been €10 /t higher than this, with lead times now in May. German HDG fell back €1 /t w/w. This is unlikely to be indicative of a trend, since lead times for HDG now stretch out to May for re-rollers and June for mills.

Italian HDG coil moved up €6 /t w/w to €529 /t, supported by northern demand, while CR coil was up €2 /t. In contrast to Germany, Italian service centers restocked heavily at the end of last year and are yet to return to the spot market in large numbers. If there were to be a new round of buying in Italy over the next month it could see CR coil and HDG coil prices increase. The average price spread between HR coil and CR coil was €86 /t last year. It currently stands at €73 /t, indicating potential to move higher.

Deliveries from Italy to northern Europe were not delayed last week, despite concern because of the coronavirus. Some truck drivers from eastern Europe have decided not to drive into the “red zone” of quarantined towns in Italy to collect material, but the major Italian flat product suppliers and consumers are outside this zone. That said, risk of production stops and weaker demand remain while the virus continues to spread and the prospects for renewed buying are accordingly still uncertain.

China

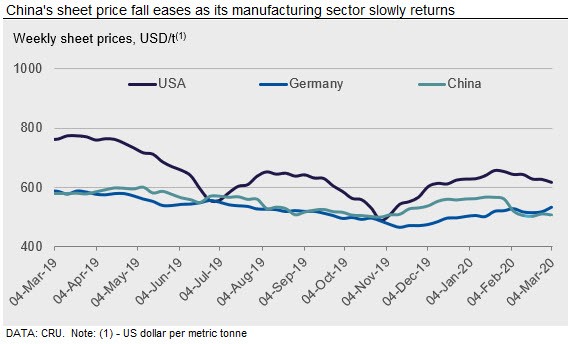

Prices fell by RMB20-50 /t over the past week. Positive information about the Covid-19 epidemic such as increasing recoveries and a lower number of daily new cases have helped domestic participants to regain confidence, though still insufficient to lift prices. Some regions outside Wuhan reported small recovery in HR coil transactions, but downstream sheet demand was still weak as downstream buyers generally hold a “wait-and-see” attitude. Sheet inventories kept rising to historically high levels and were 6 percent higher w/w, suggesting continuous supply pressure. But total inventories rose at a slower rate because of production cuts and slow improvement in demand. We expect sheet prices to remain weak next week with destocking the main theme.

Asia

Prices of imported sheet products in Asia dropped slightly as steel buyers in South East Asia became bearish.

For HR coil SAE1006, Chinese mills were heard to have been offering rerolling material at $475-480/CFR Vietnam, unchanged w/w. However, buying indications were $5-10/t lower and buyers believe it is only a matter of time until another price drop given the high Chinese mill inventories. A Japanese steel mill was heard to have sold HR coil to a regular customer in Vietnam at $470/t CFR.

For HR coil/sheet SS400, official offers from Chinese mills were at $473-478/t CFR Vietnam while traders were trying to induce buying interest at $470/t.

According to buyers in Vietnam, they will have no issue with receiving cargos from China if they follow disinfection guidance from the local government.

CRU assessed HR coil prices at $468/t, CFR Far East Asia, down by $7/t w/w. CR coil prices were assessed at $530/t CFR Far East Asia, flat w/w, while HDG prices were assessed at $560/t CFR Far East Asia, unchanged w/w.

Request more information about this topic.

Learn more about CRU’s services at www.crugroup.com