Prices

February 11, 2021

U.S. Steel Imports on the Upswing through January

Written by Brett Linton

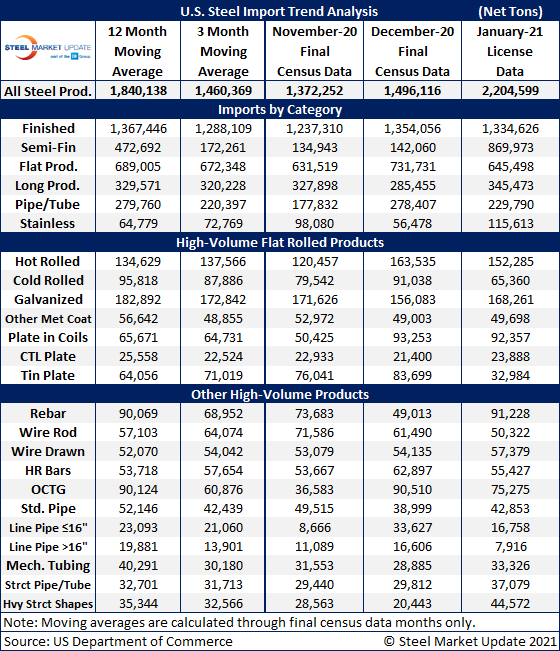

U.S. steel imports are on the upswing. December steel import figures were finalized at 1.50 million net tons, up 9% from one month prior and up 18% over September’s 11-year low of 1.26 million tons. January import licenses are up 47% from the month prior to 2.20 million tons, the highest monthly level seen since July 2020.

The average monthly import level for 2020 is now finalized at 1.84 million tons, down 21% from the 2019 monthly average of 2.32 million tons, and down 35% from the 2018 monthly average of 2.81 million tons.

Due to SMU member comments, we have expanded the import table below to include other high-volume products in addition to our normal focus on flat rolled products. We now show a brief history on products such as rebar, tin plate, wire rod, structural pipe and tube, and other long products. We also provide data on categorized imports, divided into semi-finished, finished, flat rolled, longs, pipe and tube, and stainless products. We welcome your comments.

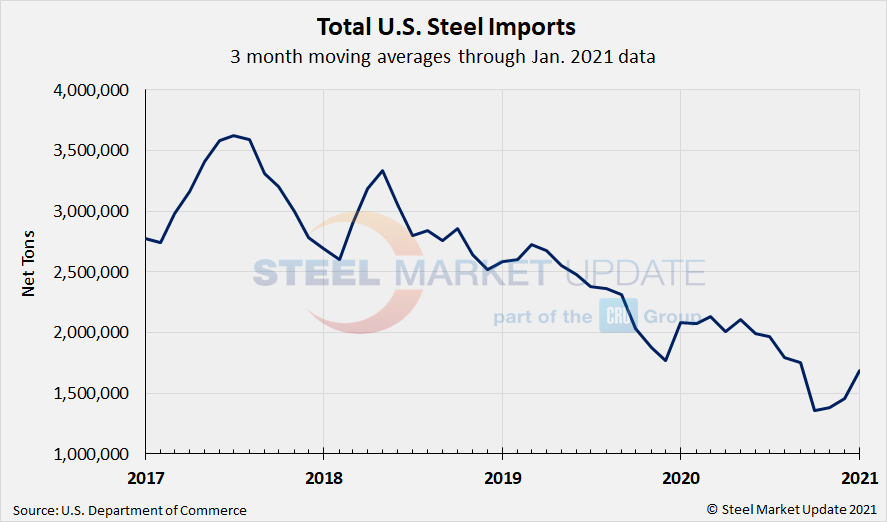

Due to large month-to-month swings in semifinished imports, the chart below shows total monthly imports on a three-month moving average (3MMA) basis in an attempt to more accurately display the U.S. steel import trend. The 3MMA through final-December data is now 1.46 million tons, up from 1.38 million tons in November.

Total finished imports in December are up 15% from the prior month at 1.43 million tons. Imports of semifinished products (mostly slabs) are at 677,000 tons, up from 135,000 tons in November.

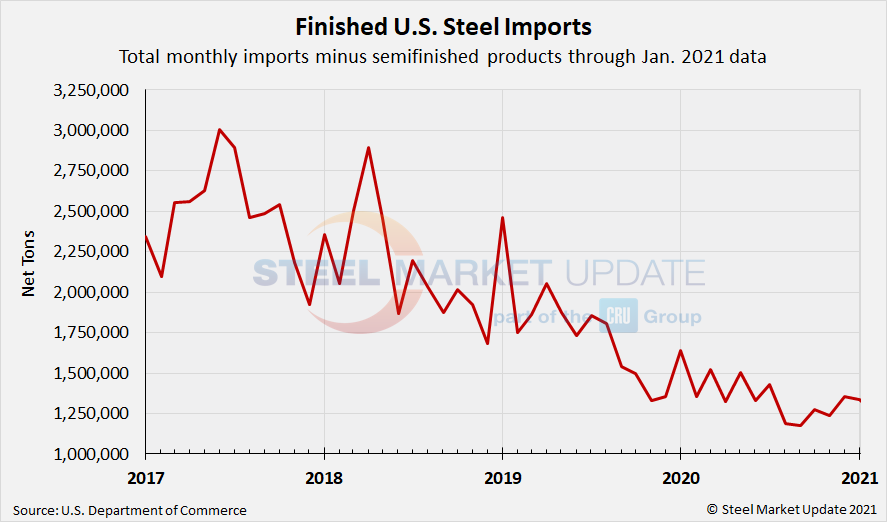

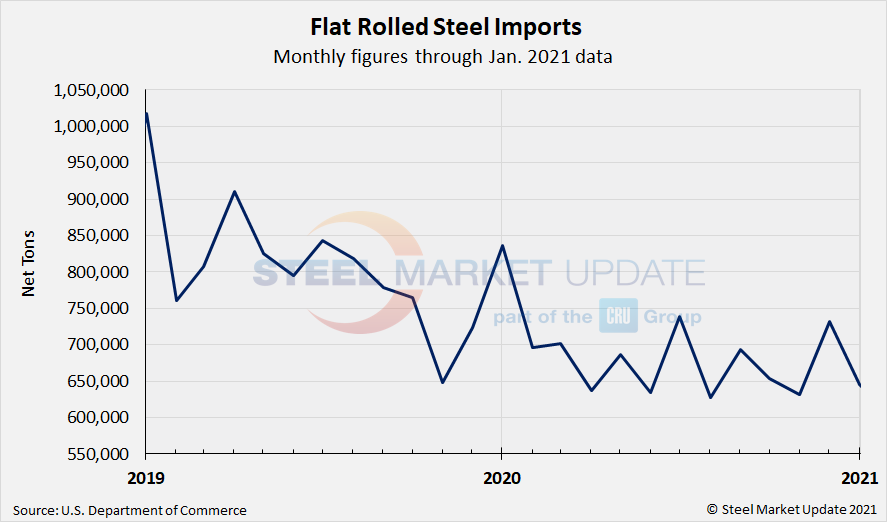

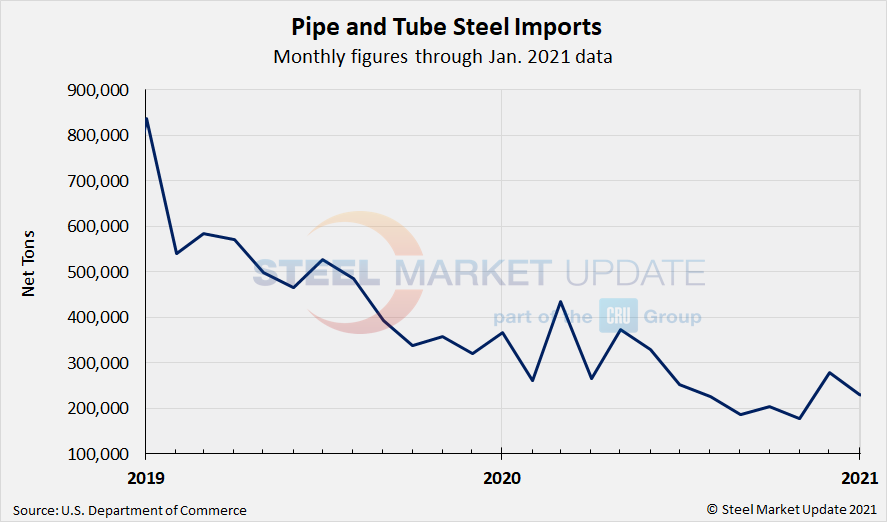

The two charts below show monthly imports grouped by product category: flat rolled imports and pipe and tube imports.

By Brett Linton, Brett@SteelMarketUpdate.com