Product

March 8, 2021

SMU CEO on Steel Demand, Steel Price Peak & More

Written by John Packard

Last week, we conducted one of our flat rolled and plate steel market trends analyses. Or, to put it another way (that the search engines don’t like), we conducted one of our surveys that we do ever other week. We invited over 500+ market participants, most of whom are steel buyers in the manufacturing and service center segments of the industry. The exact statistics from last week show that 44 percent of the respondents were service centers, 36 percent were manufacturing companies, 10 percent were steel mills, 8 percent were trading companies and the remaining 2 percent were toll processors. I think this gives us a good solid overview of the market.

By the way, the results of each survey are available to Premium level subscribers. At the end of the week when we are doing the survey, we put a 50+-page PowerPoint presentation on our website, which can be accessed by our Premium level members, who can find the latest survey results under the Analysis tab on our website (must be logged in). If you would like information on how to become a Premium member, please send an inquiry to: Info@SteelMarketUpdate.com.

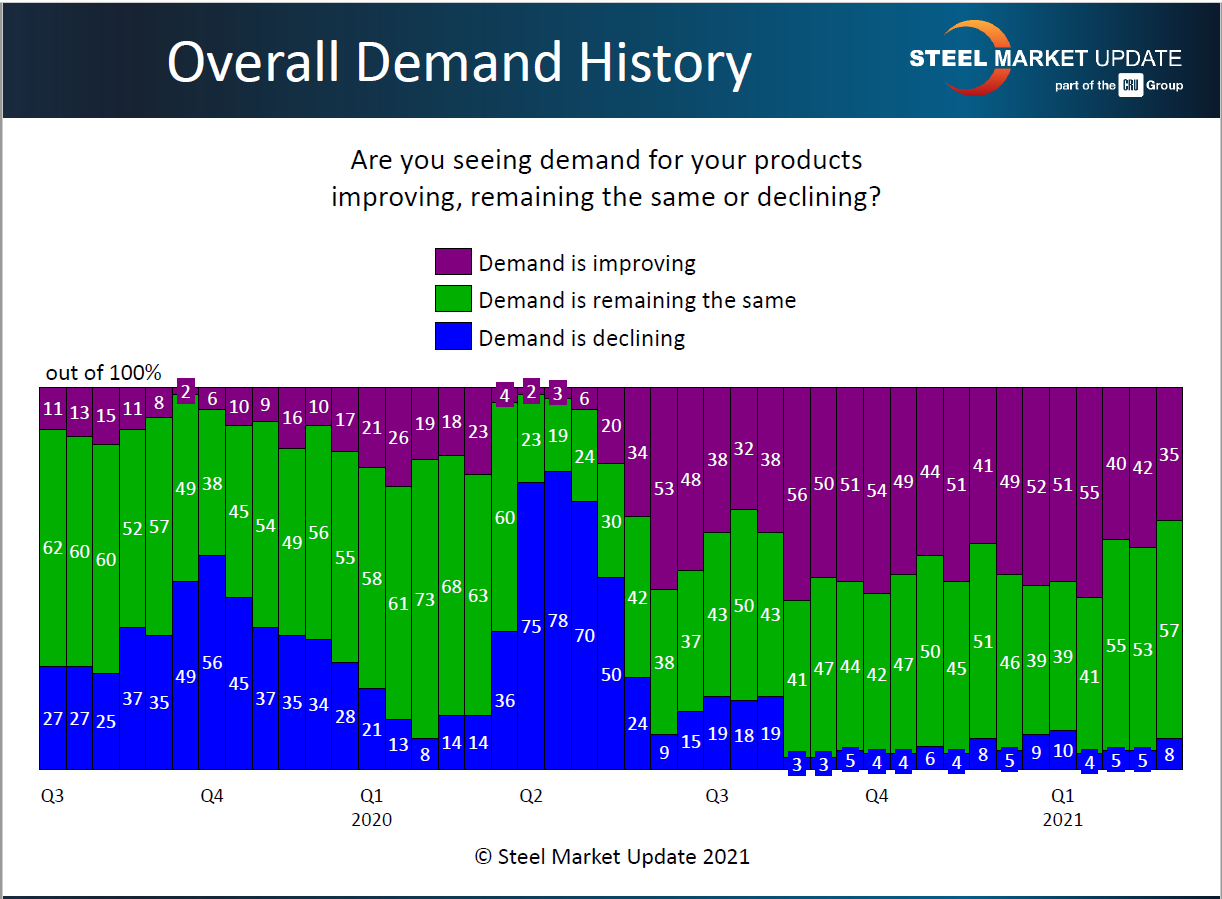

Steel Buyers Sentiment, both Current and Future Sentiment, have started 2021 at levels above where we were one year ago (pre-pandemic). Even with high steel prices, we have a very optimistic industry. We are very close to the highest levels we have ever recorded going back to 2008.

I know I have shared the graphic below with you in the not-too-distant past. It measures demand based on the responses from all of the market segments that I listed above. What this graphic does clearly show is the strength of demand and how quickly it recovered after the bleak days of second-quarter 2020. It also provides an insight as to why the market, and market prices, continue to surge.

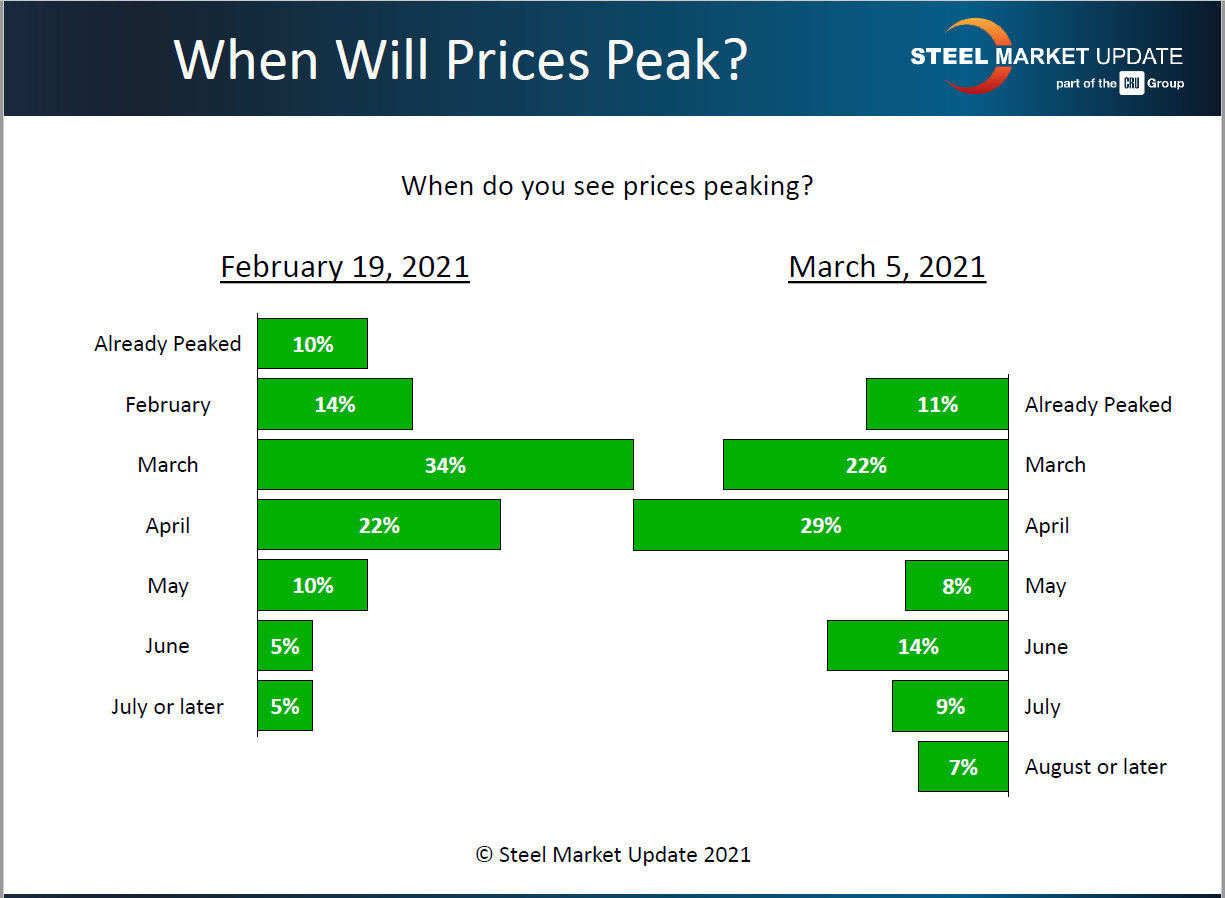

Another area we have been asking our respondents about is when they forecast steel prices will “peak.” I always smile when I ask this question because over my 44 years in this business, I have found everyone is either too optimistic or too pessimistic when it comes to forecasting peaks to the market. If you remember back a few months, many of our respondents believed prices would peak by the end of fourth-quarter 2020 or at worst the beginning of 2021. We are now in March and prices are continuing to rise…. So, take this information with a grain of salt:

The one thing that is known, based on my years of experience, is that we can anticipate unexpected steel price fluctuations as the year goes by, and the prices expected for August and December may be much different than what was expected at the beginning of this year.

Tomorrow (Monday, March 8) I will receive my second COVID-19 vaccine. Here in Florida, it seems like most of the seniors (hard to believe I am 65 or older) have received at least one shot and in many cases have already gotten two. The process of making the original appointment and then going through the steps and time associated with getting vaccinated helps give me the optimism needed to plan for a live SMU Steel Summit Conference at the end of August (23, 24, 25).

The timing of our first live event since the beginning of the pandemic will be at a critical point for the flat rolled steel industry and in the economic fortunes of North America. We will have new capacity coming online at Steel Dynamics (Mark Millett to speak), and Nucor (Leon Topalian to speak), and there will be much discussion and forecasts as to what the fourth quarter of 2021 as well as calendar 2022 will look like. We will have analysts like Timna Tanners of Bank of America, Josh Spoores and others from CRU, and economists like Alan Beaulieu of ITR Research. We will also look at infrastructure and trade; both topics will be quite “hot” in my opinion come Aug. 23-25 when we host the conference in Atlanta. You can learn more about the conference and how to register by clicking here.

When it comes your turn to get the COVID vaccine, please do not hesitate to do so.

The next workshop we have on the schedule is our Steel Hedging 101: Introduction to Managing Price Risk with Spencer Johnson of StoneX as our primary instructor along with executives from the CME Group and CRU. The dates for this workshop are March 30 & 31 (half day each). You can find out more about this workshop’s agenda, instructor biographies, costs and how to register by clicking here.

Lastly, we are going hot and heavy with our SMU Community Chat Webinars. Our intention is to produce them every other week. Since we just did one last week with Rick Preckel of Preston Pipe & Tube (you can view the recording by clicking here), our next one will be on Wednesday, March 17 with Ryan Smith, the CRU analyst who covers global mill costs and clean steels/decarbonization, etc. Because Ryan is based in Sydney, Australia, we will host this Community Chat Webinar at 3:30 p.m. ET. You can register for this FREE event by clicking here.

On March 31, we will host economist Ken Simonson of the Associated General Contractors of America at our normal time of 11 a.m. ET, and we will open registration for this free webinar on March 17.

If you would like information as to how to recieve a free trial to our newsletter, or how to become a new subscriber please contact us at info@SteelMarketUpdate.com

As always, your business is truly appreciated by all of us here at Steel Market Update.

John Packard, President & CEO, John@SteelMarketUpdate.com