Market Data

March 15, 2021

SMU Analysis: Key Market Indicators Looking Up

Written by David Schollaert

Editor’s note: Steel Market Update is pleased to share this Premium content–an edited version of our Key Market Indicators analysis–with Executive members. For information on how to upgrade to a Premium-level subscription, email Info@SteelMarketUpdate.com.

Steel Market Update’s monthly analysis of Key Market Indicators–a host of data on the economy, raw materials, manufacturing, construction, and steel sheet and long products–shows that the marketplace continues to improve, albeit cautiously. At the onset of COVID-19 a year ago, the impact of the pandemic on the economy was delayed, with only 3 of 38 indicators reflecting the dire situation the United States was facing. At the worst of the pandemic a few months later, 18 of 38 indicators had shifted negative. In the data released through March 15 this year, only 8 of the 38 indicators are negative, highlighting the ongoing rebound.

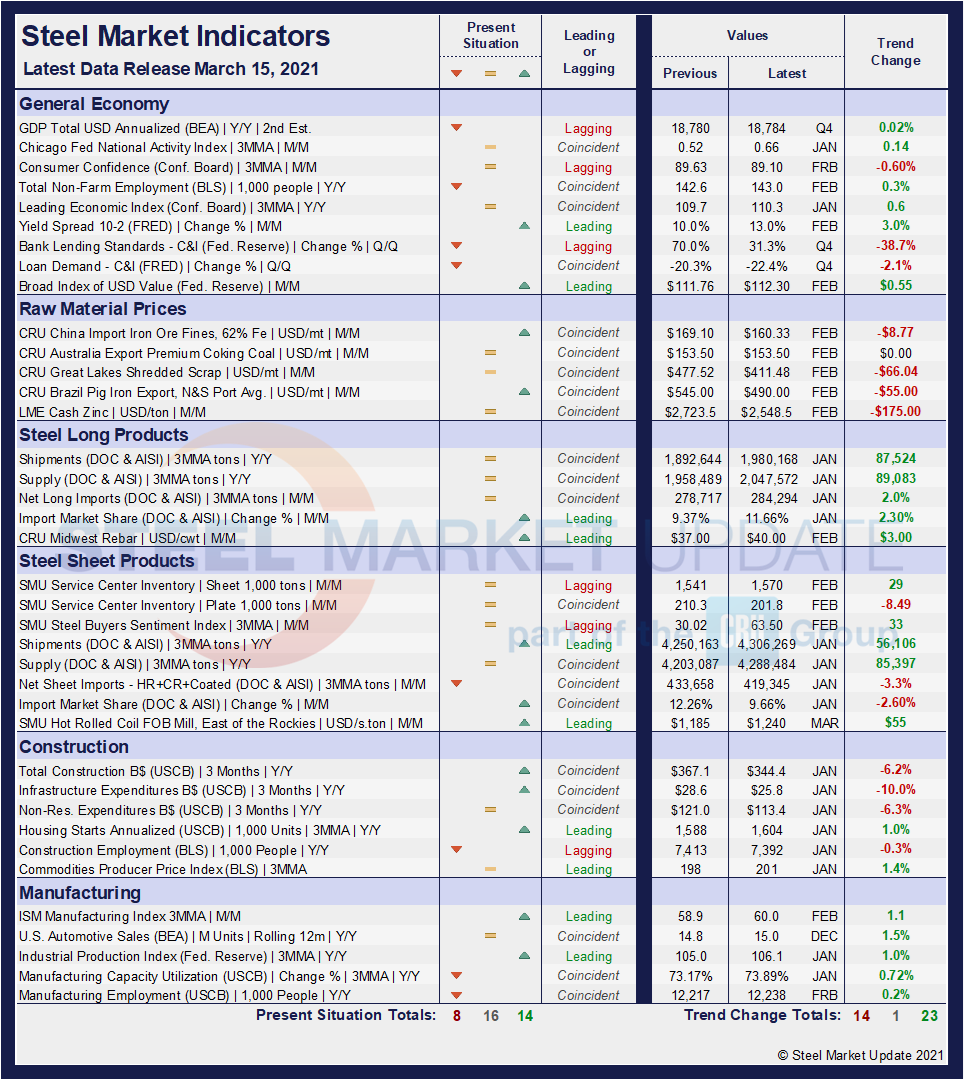

SMU’s Present Situation and Trends analysis in the table below offers a snapshot of current sentiment and the near-term expected trajectory of the economy. All results are the latest available as of March 15, 2021. Readers should regard the color codes in the “Present Situation” column as a visual summary of the current market condition. The “Trend” columns are also color coded to give a quick visual appreciation of the market’s direction. All data included in this table was released within the past month. The month or specific date to which the data refers is shown in the second column from the far right. Click on the below table to expand it.

Present Situation

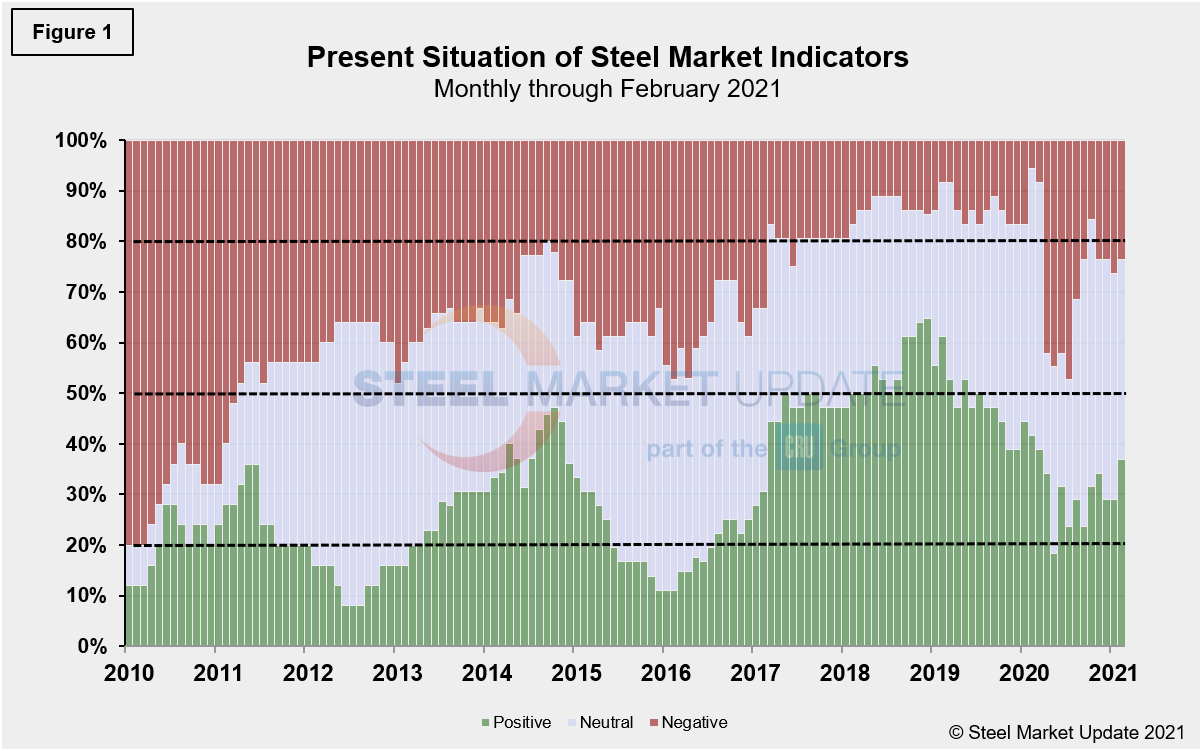

SMU’s present situation indicators highlight the differences between the fallout from the 2008-2009 economic recession and the health pandemic that has plagued the global marketplace, and in specific the U.S., over the past year. In 2010, as the market was working itself out of the recession doldrums, the present situation was 80.0% negative and only 12.0% positive. At its worst during the COVID pandemic, negative sentiment reached a low of 47.4%, while 23.7% remained positive. In that comparison, the Great Recession was far worse for the economy than the current pandemic. The marketplace has continued to respond to re-opening efforts and mass vaccinations, as our most recent assessment indicates a 36.8% positive situation; however, nearly 40.0% remain neutral as they keep a watchful eye on the economic progress.

We currently view 14 of the 38 indicators as positive, 15 as neutral and 9 as negative. Our monthly assessment of the present situation since January 2010 on a percentage basis is shown in Figure 1. Although early on in the pandemic a shift in our indicators from positive to negative was clearly seen; of late the shift has been toward the neutral category. We believe this highlights the hopeful but wait-and-see attitude in the marketplace.

By David Schollaert, David@SteelMarketUpdate.com