Market Data

April 30, 2021

CRU Macro Themes: Mid-Year Update

Written by CRU Americas

By CRU Research Manager Charlie Durant and Peter Ghilchik, CRU Head of Multi-Commodity Analysis

2021 is shaping up to be a year of economic recovery. CRU is forecasting the fastest annual growth in the world economy for 40 years, underpinned by successful vaccination programs and supportive fiscal and monetary policy.

3+1 Macro Themes

In January, we presented CRU’s three Macro Themes for the year. Now, mid-year, we are reviewing and updating our themes. Carbon Emissions and Sustainability remain important themes for our customers in the run-up to COP26. China remains an important player in the commodity industry – but its role is changing due to the Five-Year Plan. In this mid-year update CRU has decided to add a fourth theme: “Supercycle or business cycle.” This reflects the lively debate around whether we are at the foothills of a new commodity Supercycle.

Carbon Emissions

The growth in renewables as the energy source for power, together with the electrification of mining equipment, is a key enabler for decarbonization. New technologies, including carbon capture, hydrogen/ammonia as a fuel, process and supply-chain optimization, and recycling, will be important levers. CRU is continuing to examine the implications of applying these approaches across value chains to optimize emissions abatement.

In 2021, governments have started to shift from rhetoric to policy implementation. The U.S. has re-joined the Paris Agreement. The EU has announced plans around its carbon border adjustment mechanisms (CBAM). China is expected to announce further decarbonization policies ahead of COP26. CRU will continue to investigate the following questions: How will other countries respond to increasing climate ambitions in these major economies? How will this impact trade flows and metal prices when implemented? How effective will climate policies be in supporting the uptake of EVs and the rise of recycling rates of end-of-life goods?

Global carbon prices and regulations will escalate costs of high emitters and alter value-in-use assessments. CRU’s analysis of costs will explain how this will tilt and reshuffle global cost curves and reshape supply pipelines. We will continue to highlight assets that are at risk of becoming stranded due to escalating costs. Meanwhile, where there are downstream manufacturers who are increasingly demanding “green metal” to meet sustainability targets – we will be assessing if low carbon products attract a premium.

China 5-Year Plan

2021 marks the launch of China’s 14th Five-Year Plan (FYP). The new FYP puts emphasis on internal circulation and domestic consumption as the main pillar of economic growth and discusses a pivot away from infrastructure investment and trade. If these changes take effect as planned, it will mean China will play a very different role in global commodity markets in the next decade than it has over the previous decade. The changing role of China is one to watch.

There was slight disappointment that the government did not announce a faster path of decarbonization at the National People’s Congress in March. For steel, our expectation is that steel supply will be reduced, and the means of production changed, though without impacting demand (i.e. lower economic activity), there is limited scope for outright cutbacks in the medium-term.

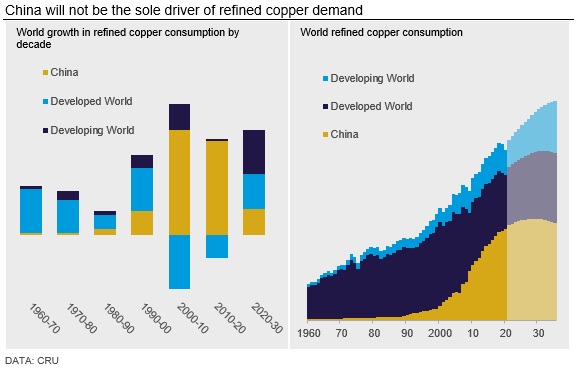

Early this year, Beijing shifted to a tightening phase of policy the effect of which can now be observed in metals demand. China accounts for over 50% of global refined copper and primary aluminum consumption, up from under 20% just two decades ago. However, our forecast growth rates for Chinese metals demand – including steel and copper – over the next decade is substantially lower than the past decade.

China’s 14th FYP will see increased focus on green living and high-quality growth. The aspiration is to achieve this through greater self-reliance and technological innovation. Smarter use of investment and regional supply chains will allow Chinese industry to move up the value chain. CRU is looking at how high-quality growth and green living might coexist in China, and which commodities the green energy transition will support.

China is also looking to increase its self-reliance. Overseas investment in mining and metal resources will continue to guarantee the supply of critical materials. Which strategic assets might China purchase next? Will it prefer to buy greenfield projects or M&A? CRU will seek to answer these questions and consider how these actions could result in displacement of countries that currently export commodities to China – and how these decisions affect global supply chains and commodity prices.

Reshaping Global Trade

The prevalence of regulatory trade protectionism has been increasing – and COVID-19 exacerbated this. Will the rapid change in industry structure (decarbonization), COVID-19 paranoia, and shifting attitudes to populism fortify or destroy commodity trade barriers? These were the questions posed when we established our third theme of “reshaping global trade.”

While trade tensions remain, skyrocketing commodity prices have demonstrated the need for diverse supply chains, rather than a narrowing of them. With fast moving markets comes arbitrage opportunities, and traders across all commodity markets have been capturing these through the year, spurring global trade. Global freight rates have moved to astonishingly high levels as a result.

Recent sanctions imposed on Belarus represent an example of watering down of trade weaponization. Sanctions were imposed by the EU in response to continued discontent with the actions of its president Alexander Lukashenko. But these sanctions were much weaker than anticipated, likely due to the EU’s reliance on potash from the country and already ballooning fertilizer prices.

China is increasingly looking to offshore its emissions. This has the potential to reshape global steel and aluminum trade over the longer term. Governments around the world may have touted the benefits of regionalization and protectionism through the darkest days of the pandemic. But the recent surge in commodity prices and tight supply chains has shone a light on the benefits of efficient global trade.

Supercycle or Business Cycle?

The hottest debate through 2021 has been focused on one question – are we in a new commodity price supercycle or is this just a shorter-term business cycle? With commodity prices increasing sharply, and governments across the world stimulating their economies with a green policy agenda with a decarbonization focus, there is a strong argument suggesting a new commodity supercycle has already been triggered.

However, CRU maintains this is not yet a supercycle. The impact of COVID-19 on inflation and market supply and demand fundamentals is likely to be transitory. And, while governments have noble intentions to decarbonize, they are yet to fully commit via robust policies.

Our cross-commodity supply and demand analysis show, in general, there is still enough supply to meet demand. Our base case is this will remain the case in the long run also. The increasing focus on ESG in commodity markets will create supply headwinds and drive some demand opportunities. Commodity markets might be running hot right now, but a longer-term perspective is important when discussing supercycles, which run for 20+ years, not just 20 months.

Request more information about this topic.

Learn more about CRU’s services at www.crugroup.com