Community Events

June 10, 2021

Steel Prices To Fall, Steelmageddon® Still Coming: Tanners

Written by Sandy Williams

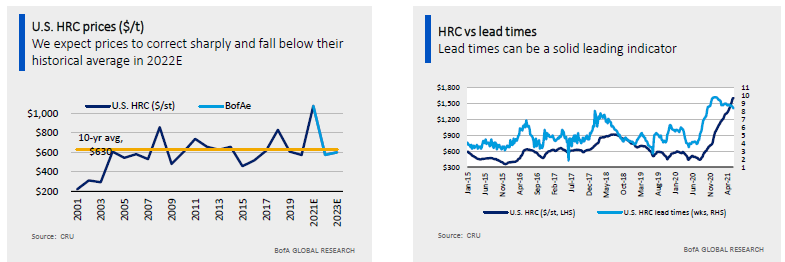

Steel prices will correct sharply as supply catches up with demand, potentially falling back to an average of $575 per ton ($28.75 per cwt) in 2022, according to one leading industry analyst.

“This too will pass,” was the title chosen by Timna Tanners, metals and mining analyst at Bank of America, for her SMU Community Chat Webinar.

Steel prices have skyrocketed more than 70% this year and now average $1,675 per ton ($83.75 per cwt), according to SMU data. Demand is outpacing supply, and lead times for HRC are out more than 10 weeks on average.

“There is no time in history where prices go up and just stay there. It just doesn’t happen,” Tanners said.

Historically, when lead times start to turn, prices correct two to three months later, she noted.

And it makes no sense to say that the new normal is $1,600 per ton or more. “There is no basis in iron ore, no basis in scrap, there is no basis on the cost side that explains why prices would stay high,” Tanners said.

Also, the impact of industry consolidation is not so significant that it would impact prices to such an extent, she said.

A lag effect in passing along higher prices is probably what is keeping consumers from “screaming bloody murder” about $1,600-$1,700 HRC prices, Tanners said.

High prices are not as much of a demand issue as a supply and lead time issue. Difficulty procuring steel has led to higher order quantities to ensure that firms have at least a minimum supply of steel on hand. Transportation logjams have resulted in late delivery times, which is another reason for customers to increase orders. “That is what is causing the demand shift,” said Tanners, “not really underlying demand.”

Production is back to normal following pandemic shutdowns, and there is also some new capacity in the mix as well. And margins have exploded from historical averages with steel mills making “crazy amount of profits.”

Mills are using the extra cash to add production lines and improve performance. But “no one is talking about additional HRC or hot melt supply,” said Tanners. Why? In part because planned new capacity, other than that from Big River Steel, has yet to hit the market. Projects to add new capacity in the U.S, Canada and Mexico were pushed back because of pandemic, but those tons are still coming.

Is Steelmageddon® still in play? Tanners thinks it is. But it just hasn’t played out yet. She notes that steel consumption is not dramatically different in the U.S. than it has been in the past. Tanners said she is not convinced that Americans will continue to consume more steel-intensive goods, and she warned of the potential for an infrastructure bill to be watered down. “That is a rebar story anyway,” said Tanners, “rebar, and to some extent plate and beam, but much less of a sheet driver.”

Tanners appears correct in her estimation that Section 232 tariffs would be removed on the EU by the end of the year. Shortly after the webinar, news of an agreement between the U.S. and EU to left the tariffs and quotas by Dec. 1 hit the media.

Politicians have an uncanny ability to respond to issues at the wrong time. Chinese exports to the U.S. had largely been curbed by traditional trade cases before Section 232 was implemented. And by the end of the year, when the tariffs are set to be removed, steel prices might already be falling, she said.

Still, any fears about a flood of steel exports from the EU to the U.S. are unfounded. Tanners noted that the EU is generally a balanced market and primarily exports steel products to the U.S. that are not made domestically. If the EU implements a carbon border tax , it will result in even less European steel hitting U.S. shores.

Green steel is a hot topic right not just in the EU but across the industry. The problem: “If we want greener steel, who will pay for it?” Tanners asked. The carbon emissions focus is, for the time being, primarily a European story and doesn’t necessarily impact other major steel producing regions. “The U.S. has the greenest steel—I get it. But do you really want to go down to Brazil and tell them they can’t use coal anymore and they have to build EAFs when they have captive iron ore? It makes no sense, right? They can’t just rejig their entire steel industry any time soon, and, they have the lowest-cost steel in the world.”

Tanners is not particularly concerned about mill maintenance outages in the latter half of the year further tightening supply. Mills prepare for planned outages, and so they are not that disruptive.

What could tighten the market is if auto production takes off and demands more incremental tons. BoA has heard that the auto manufacturers are taking in steady amounts of steel so they don’t get caught short as they did last year.

Tanners also noted that many in the auto industry are not happy with the consolidation by Cliffs and U.S. Steel. Auto companies prefer as many suppliers as possible and are contacting Steel Dynamics and Nucor to develop exterior applications using EAF-produced steel. And EAFs might pursue such applications more aggressively over the next several years, she said.

On the scrap side, the new EAFs coming online will mean increased demand. But so far, prices have been steady due to DR, HBI and pig iron tempering the market. Mills have been managing scrap supply admirably and more prime scrap is on the way once automotive activity, delayed by the chip shortage, returns to normal in third quarter, Tanners said.

By Sandy Williams, Sandy@SteelMarketUpdate.com