Prices

June 29, 2021

SMU Price Ranges & Indices: Benchmark Hot Rolled Up Only $10/ton

Written by Brett Linton

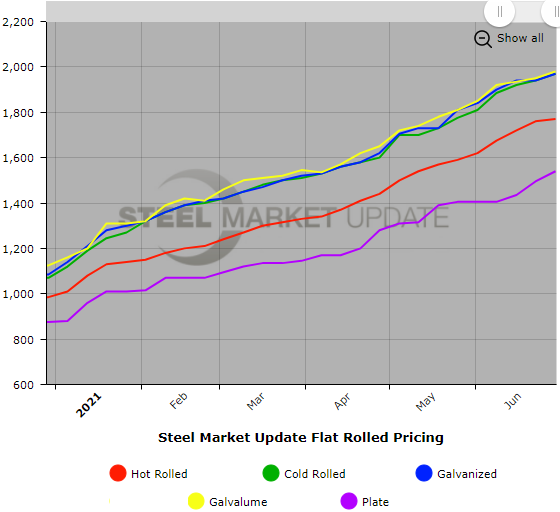

Flat rolled steel prices continued to move higher with benchmark hot rolled coil spot prices now up for the 47th week in a row.

But when we looked at HRC, we found prices up only by $10 per ton. This is the lowest rate of increase since mid-March/early April, when we saw HRC increase by a modest (by 2021 standards) $40 per ton over a four-week period.

SMU is not reading too much into the HRC number because other flat-rolled and plate products were much higher this week. We saw cold rolled, galvanized, and Galvalume all up $30 per ton. Steel plate prices rose a more significant $45 per ton following a round of price hikes announced by domestic steel mills last week.

We will continue to watch the spreads and for any signs of a retreat in pricing in the coming weeks.

The number of data points we received this week from flat rolled buyers was lower than usual. (We assume summer vacations are beginning to affect our pool of data providers). But the number of plate inputs was within the normal range.

Here is how we see prices this week:

Hot Rolled Coil: SMU price range is $1,700-$1,840 per net ton ($85.00-$92.00/cwt) with an average of $1,770 per ton ($88.50/cwt) FOB mill, east of the Rockies. The lower end of our range increased $30 per ton compared to one week ago, while the upper end decreased $10 per ton. Our overall average is up $10 per ton from last week. Our price momentum on hot rolled steel is Higher, meaning prices are expected to rise in the next 30 days.

Hot Rolled Lead Times: 8-12 weeks

Cold Rolled Coil: SMU price range is $1,950-$1,990 per net ton ($97.50-$99.50/cwt) with an average of $1,970 per ton ($98.50/cwt) FOB mill, east of the Rockies. The lower end of our range increased $70 per ton compared to last week, while the upper end decreased $10 per ton. Our overall average is up $30 per ton from one week ago. Our price momentum on cold rolled steel is Higher, meaning prices are expected to rise in the next 30 days.

Cold Rolled Lead Times: 8-14 weeks

Galvanized Coil: SMU price range is $1,940-$2,000 per net ton ($97.00-$100.00/cwt) with an average of $1,970 per ton ($98.50/cwt) FOB mill, east of the Rockies. The lower end of our range increased $60 per ton compared to one week ago, while the upper end remained unchanged. Our overall average is up $30 per ton from last week. Our price momentum on galvanized steel is Higher, meaning prices are expected to rise in the next 30 days.

Galvanized .060” G90 Benchmark: SMU price range is $2,009-$2,069 per ton with an average of $2,039 per ton FOB mill, east of the Rockies.

Galvanized Lead Times: 8-16 weeks

Galvalume Coil: SMU price range is $1,900-$2,060 per net ton ($95.00-$103.00/cwt) with an average of $1,980 per ton ($99.00/cwt) FOB mill, east of the Rockies. The lower end of our range remained unchanged compared to last week, while the upper end increased $60 per ton. Our overall average is up $30 per ton from one week ago. Our price momentum on Galvalume steel is Higher, meaning prices are expected to rise in the next 30 days.

Galvalume .0142” AZ50, Grade 80 Benchmark: SMU price range is $2,191-$2,351 per ton with an average of $2,271 per ton FOB mill, east of the Rockies.

Galvalume Lead Times: 11-16 weeks

Plate: SMU price range is $1,440-$1,640 per net ton ($72.00-$82.00/cwt) with an average of $1,540 per ton ($77.00/cwt) FOB mill. The lower end of our range increased $40 per ton compared to one week ago, while the upper end increased $50 per ton. Our overall average is up $45 per ton from one week ago. Our price momentum on plate steel is Higher, meaning prices are expected to rise in the next 30 days.

Plate Lead Times: 8-13 weeks

SMU Note: Below is a graphic showing our hot rolled, cold rolled, galvanized, Galvalume and plate price history. This data is available here on our website with our interactive pricing tool. If you need help navigating the website or need to know your login information, contact us at info@SteelMarketUpdate.com.