Market Data

July 15, 2021

Shipments and Supply of Steel Products Steady in May

Written by David Schollaert

Mill shipments of steel products rose in May by 1.9%, rebounding from the 2.0% decline seen the month prior, while apparent supply was up 1.7% compared to April. Although mill shipments and apparent supply gains have decelerated from the nearly 20.0% rally seen in March, May’s gains were the third increase in as many months after February’s double-digit contraction.

This analysis is based on steel mill shipment data from the American Iron and Steel Institute (AISI) and import-export data from the U.S. Department of Commerce (DOC). The analysis summarizes total steel supply by product from 2008 through April 2021 and year-on-year changes.

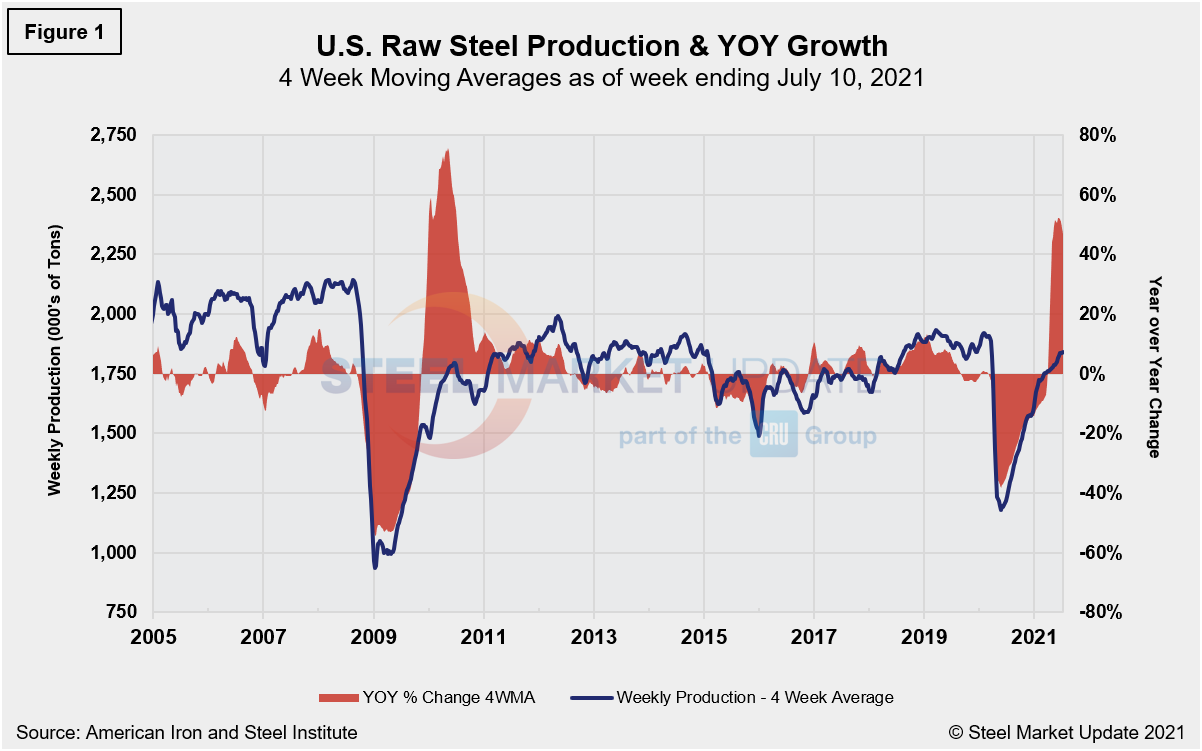

Although rebounding demand from last year’s COVID-19 doldrums has certainly played a role in pushing steel prices to record heights, supply limitations have been the primary driver. While domestic mill utilization reached the highest average rate in more than a decade—83.6% in the week ending July 10—steel supplies, including domestic production and imports, continue to lag demand, extending the price rally. HRC prices range from $1,800-$1,840 per net ton, according to SMU’s latest survey of the market, a new all-time high with few signs the market is slowing down. Raw steel production shown below in Figure 1 is based on weekly data from the AISI and displayed on four-week moving averages.

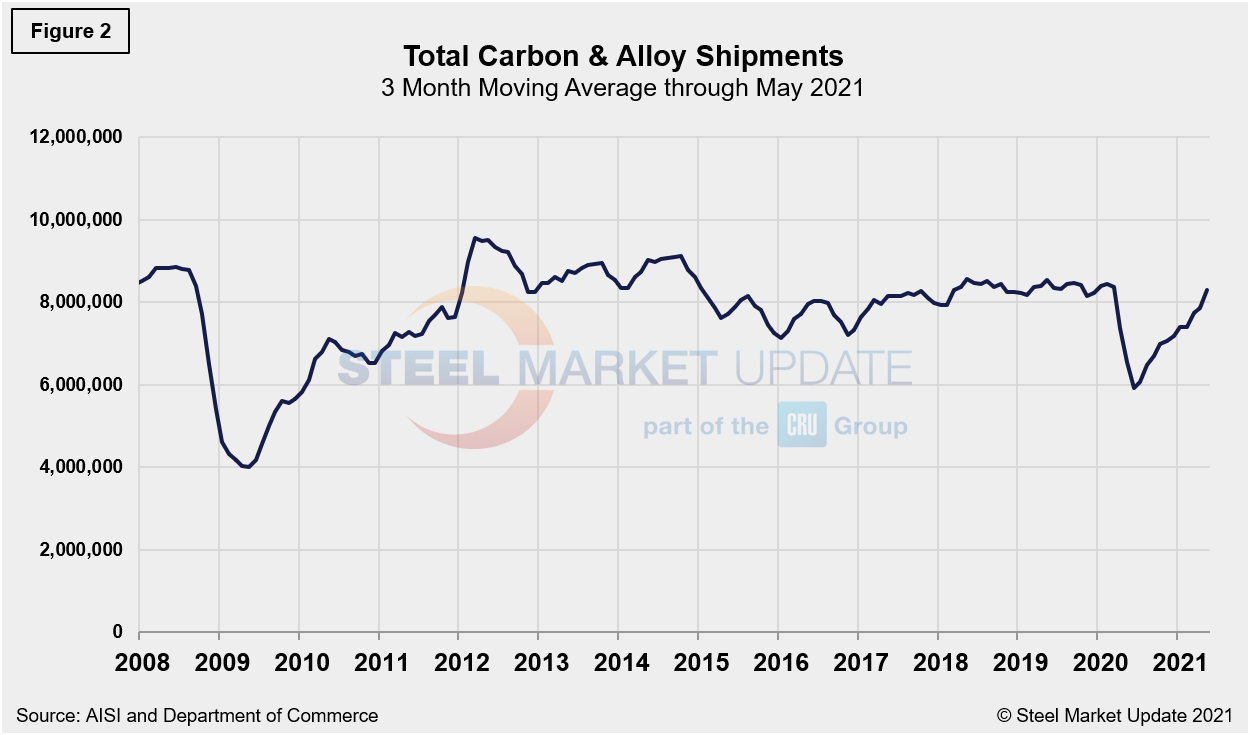

Monthly shipment data for all rolled steel products is noted in Figure 2. The trajectories of the rebounds since Q2 2020 are comparable in Figures 1 and 2. Measured as a three-month moving average (3MMA) of the monthly data, May’s total was 8.397 million tons, compared to 8.241 million tons in April, a 1.9% increase. Shipments were up 49.2% in May compared to the year prior when shipments bottomed at just 5.627 million tons—its lowest mark in over a decade—as the economy was reeling from the worst of the pandemic. The recovery, with shipments nearly doubling in May compared to the same year-ago period, underscores the debilitating impact of the virus and the astounding progress the market has made.

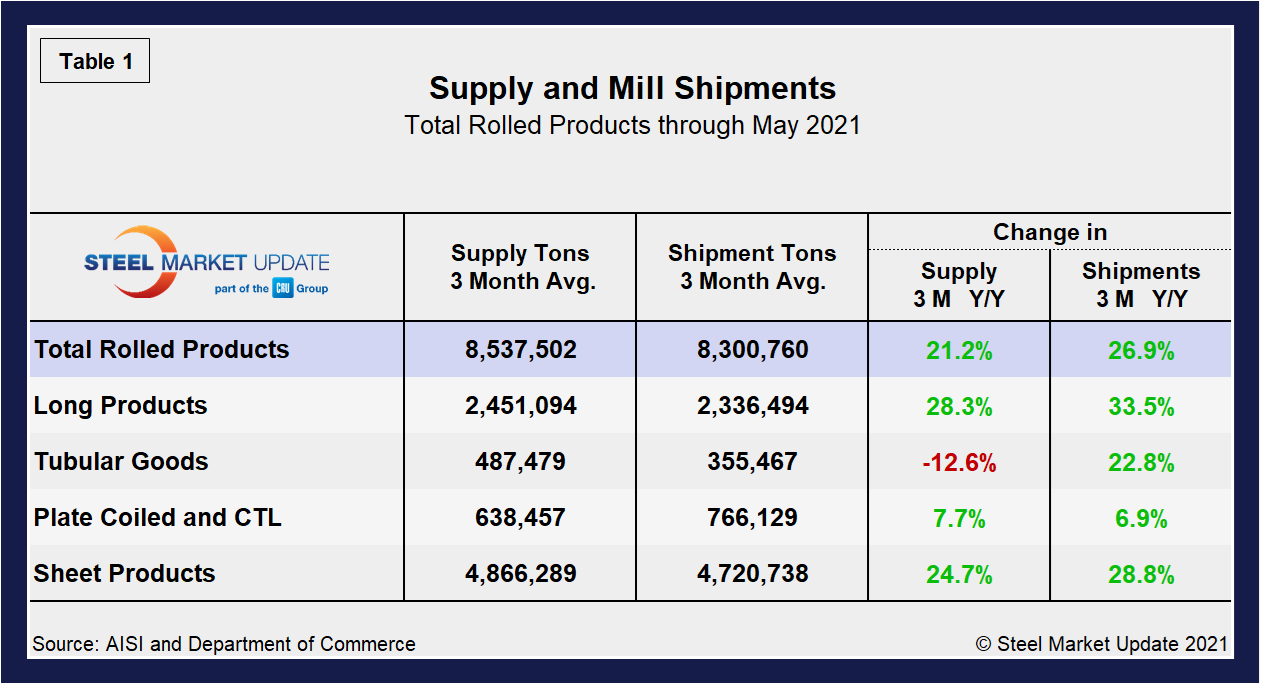

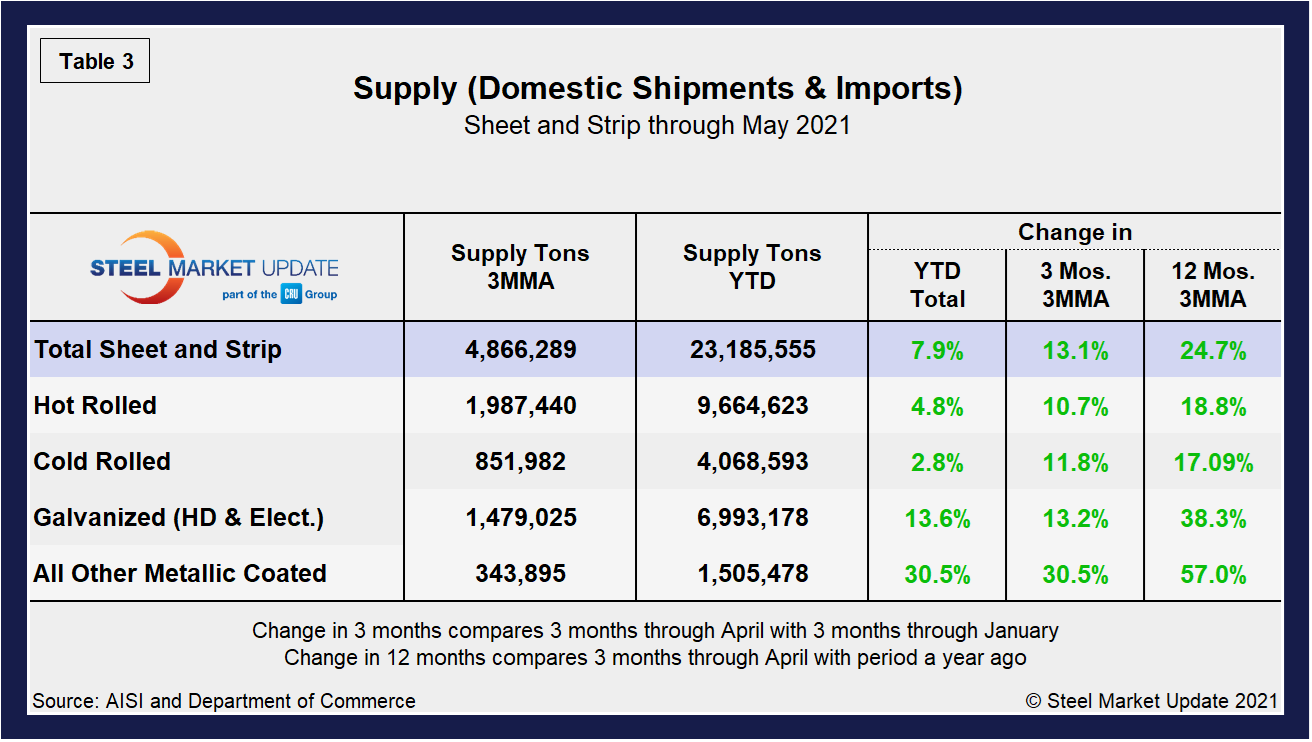

Shipment and supply details for all product groups are noted in Table 1, followed by individual sheet products in Table 2, and domestic supply (shipments and imports) in Table 3. Total supply (proxy for market demand) as a 3MMA was up 21.2% year over year in May, a big turnaround from the 28.1% decline last June when the market hit bottom. Apparent supply is defined as domestic mill shipments to domestic locations plus imports. Mill shipments improved by 26.9% in May, up from 6.6% in April in the three-month comparison. The recovery has varied significantly among various products, with tubular goods lagging most others.

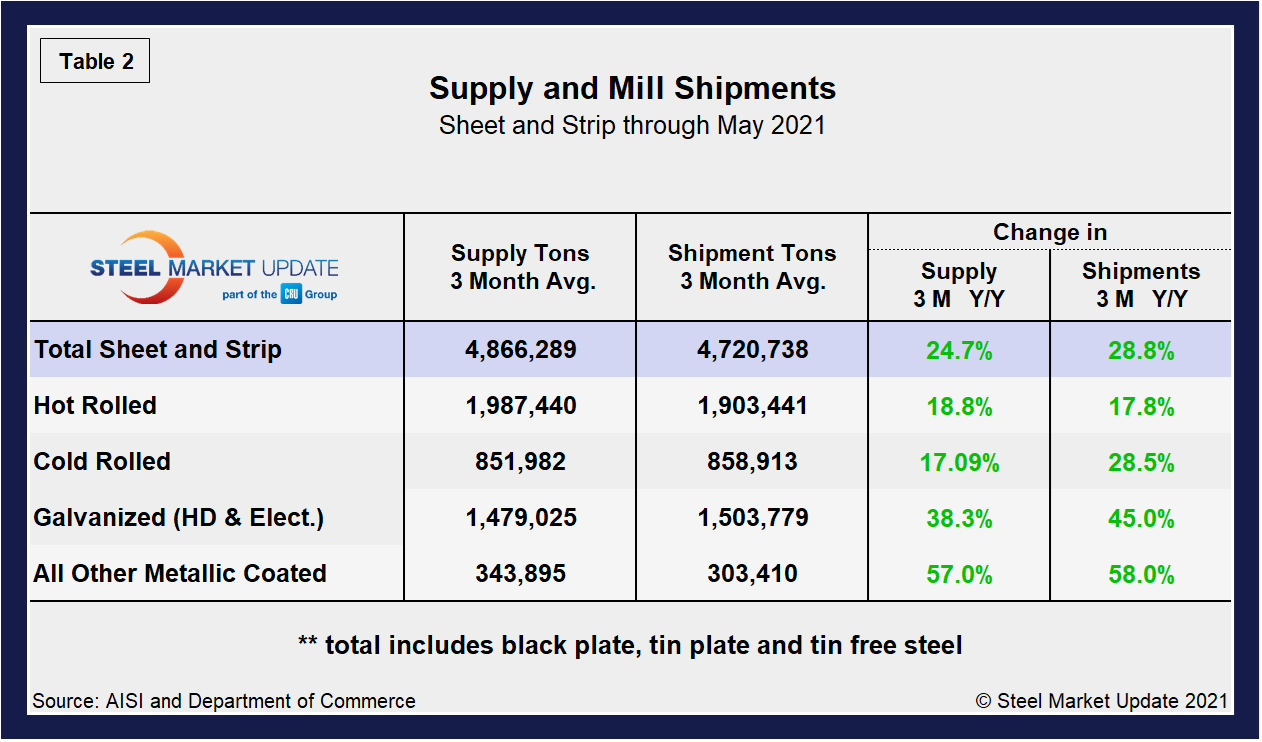

Overall sheet product shipments and supply (Table 2) have improve markedly month on month. Supply increased by 24.7% and shipments by 28.8% in May, a strong recovery from declines of 7.5% and 6.5% in March. In the three months through May 2021, the average monthly supply of sheet and strip was 4.866 million tons, up from 4.586 million tons or 5.4% from the prior month. Total sheet and strip apparent supply is up 7.9% year to date (Table 3) compared to 2020. Note that year-over-year comparisons have seasonality removed.

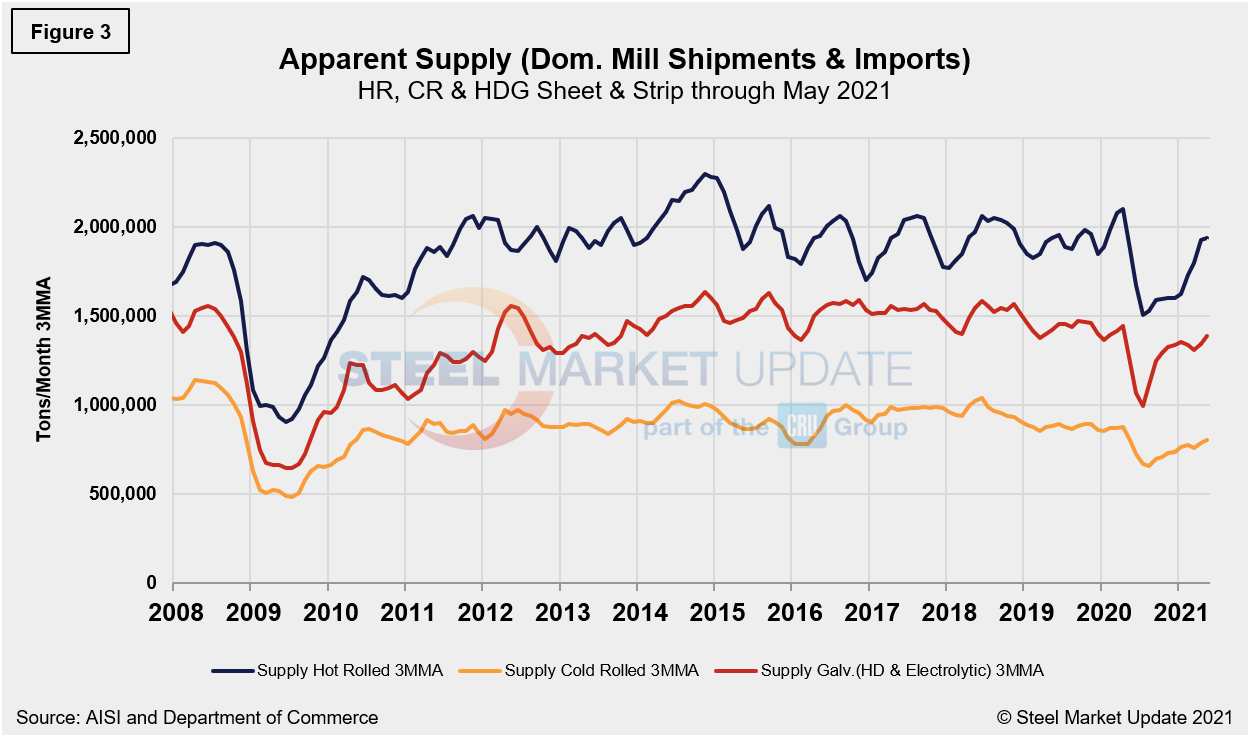

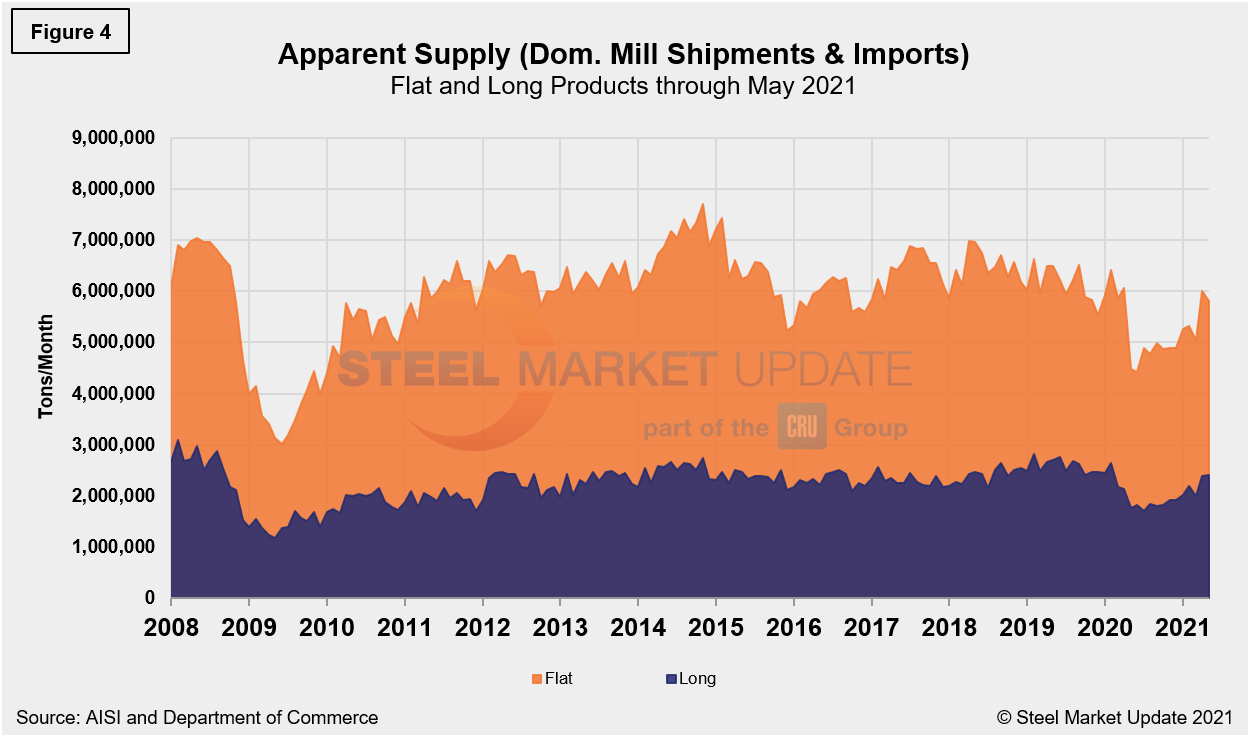

The supply picture for HRC, CRC and HDG since August 2008 as three-month moving averages in Figure 3 and Figure 4 show the long-term comparison between flat and long products. All three sheet products have experienced some improvement since mid-2020, but galvanized (hot-dipped and electrolytic) has seen the strongest rebound, a 48.3% jump since reaching bottom in June 2020, and rose 6.5% month on month in April following an increase of 3.3% the month prior. In Figure 4, note that these are monthly numbers (not 3MMAs), which show the trend difference between longs and flat products including plate.

By David Schollaert, David@SteelMarketUpdate.com