Prices

April 22, 2022

SMU Deep Dive: Hot Rolled vs Galvanized Prices

Written by Brett Linton

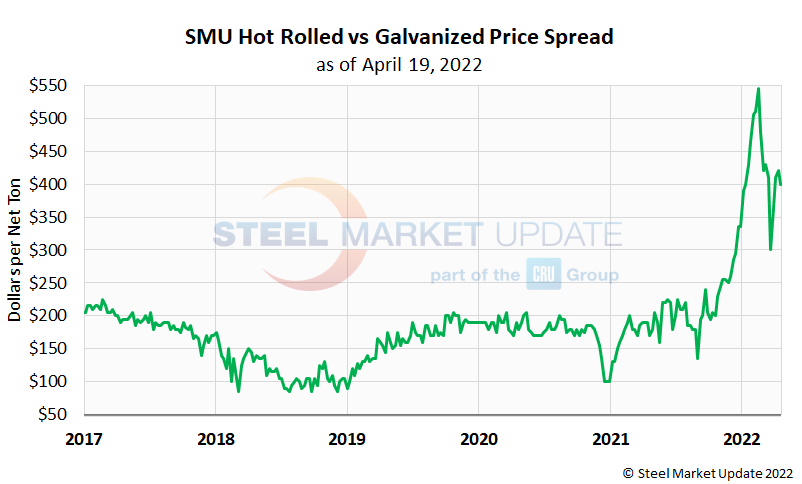

The relationship between hot rolled and galvanized steel prices has fluctuated heavily over the past six months, with galvanized selling between a $200-545 per ton premium over hot rolled in that time frame. The premium reached record high levels as steel prices declined earlier this year, only beginning to dial back when steel prices reversed course in early March.

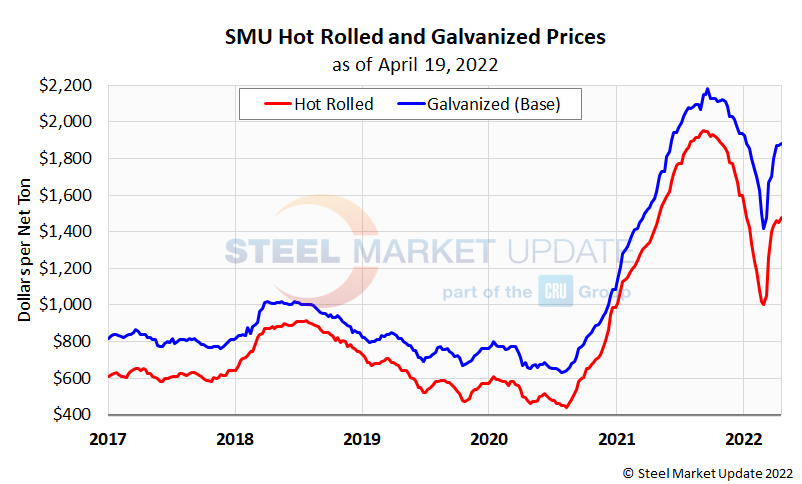

SMU’s hot rolled coil price averaged $1,480 per ton ($74 per cwt) last week and has risen six of the past seven weeks. Recall our index had reached a 14-month low of $1,000 per ton in the first week of March, following a record-high $1,955 per ton in September 2021. Our latest galvanized price index averaged $1,880 per ton ($94 per cwt) last week, and has remained steady or increased each of the past seven weeks. Galvanized prices peaked at $2,185 per ton last September, falling to a 12-month low of $1,420 in early March.

As shown in the graph below, galvanized held a premium between $80-220 per ton over hot rolled for the last few years, exceeding that range in late 2021. The premium rapidly rose to peak at $545 per ton in mid-February, marginally declining thereafter. The spread last week was $400 per ton, having dipped to a 3-month low of $300 per ton in late March.

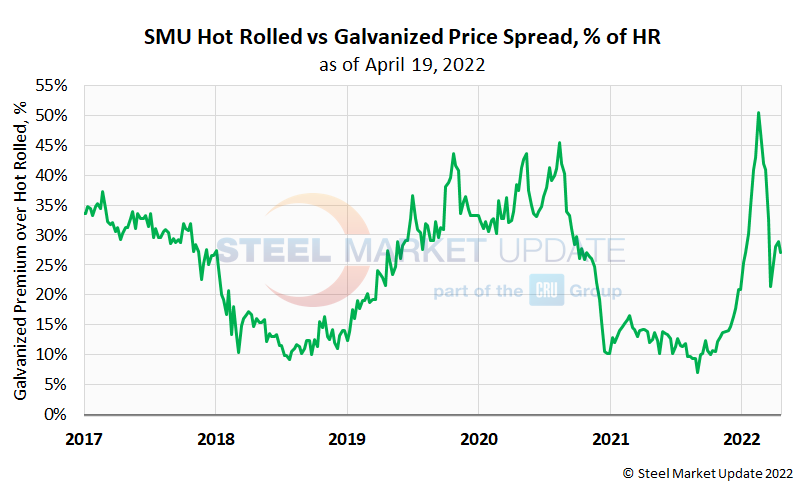

To better compare this price spread, we graphed the galvanized price premium over hot rolled as a percentage of the hot rolled price. This is an attempt to paint a clearer comparison against historical pricing data. As shown in the below graphic, the percentage premium is not as alarming compared to the dollar value premium. Galvanized prices held an average premium of 24% above hot rolled prices from 2017 through the end of 2021. 2021 averaged just 13%, while 2022 YTD now averages a 34% premium through last week. The premium rose to a record high in mid-February 2022 of 50%. The latest spread has softened to 27% and has been roughly in that ballpark for the last three weeks.

By Brett Linton, Brett@SteelMarketUpdate.com