Prices

May 3, 2022

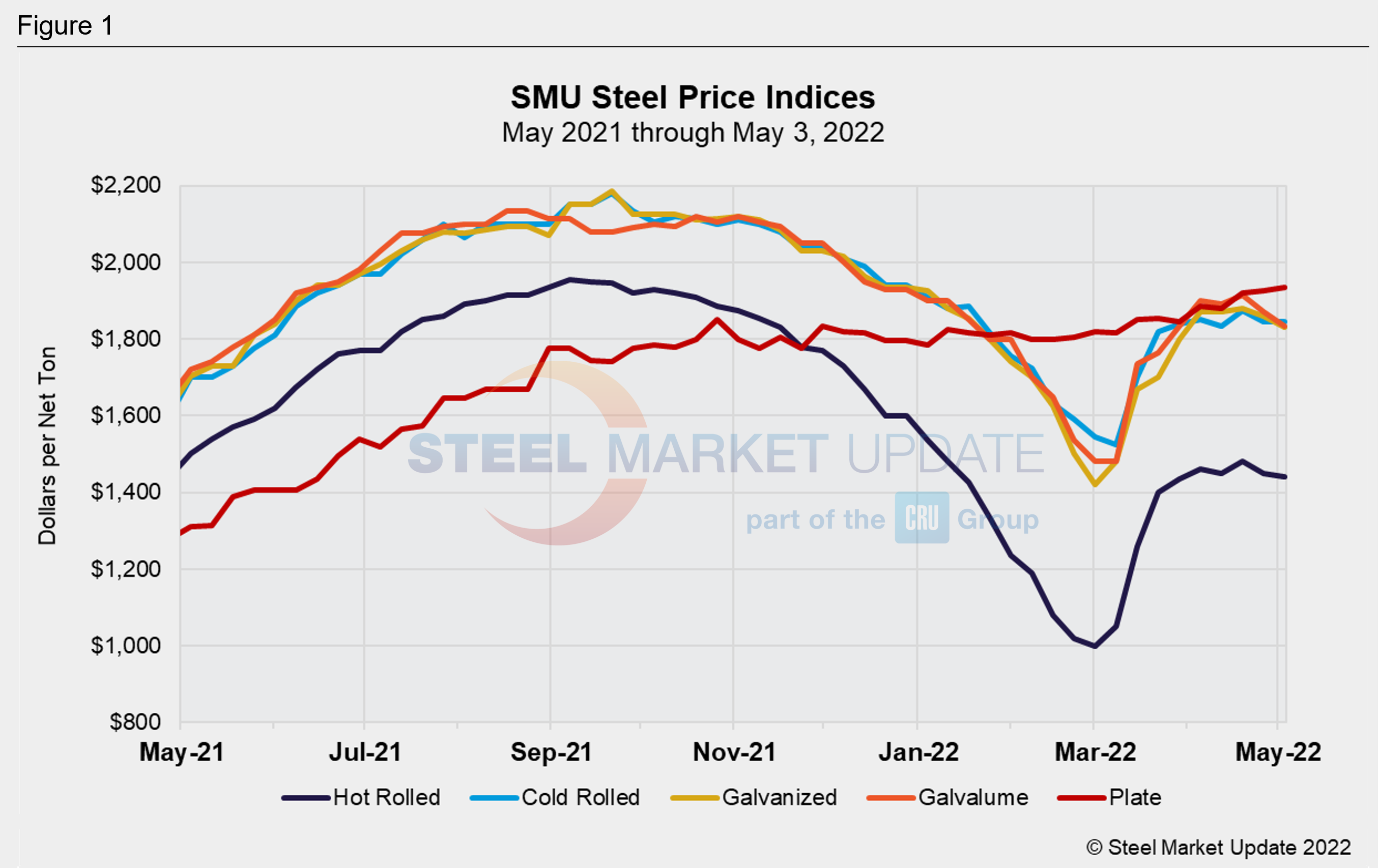

SMU Price Ranges & Indices: Another Week of (Mostly) Weaker Steel Tags

Written by Brett Linton

Sheet prices were flat or lower again this week on expectations of lower scrap prices and concerns about increased import competition over the summer months.

Hot-rolled coil prices were down $10 per ton, cold-rolled prices were unchanged, galvanized base prices down $30 per ton, and Galvalume base prices down $35 per ton.

Plate prices were up $10 per ton, although effectively unchanged given base prices north of $1,900 per ton. Some sources said that they felt they were being gouged by such lofty figures and that they might shift more plate volume to mills outside the US.

SMU is keeping its pricing momentum indicators at neutral despite those generally downward trends. Why? Because sources noted that supply chain issues and shortages could surprise the market in the weeks ahead – notably potential shortages of zinc and aluminum, which could force some coaters to run at significantly less than full capacity.

Hot Rolled Coil: SMU price range is $1,400-$1,480 per net ton ($70.00-$74.00/cwt) with an average of $1,440 per ton ($72.00/cwt) FOB mill, east of the Rockies. The lower end of our range increased $10 per ton compared to one week ago, while the upper end declined $30 per ton. Our overall average is down $10 per ton from last week. Our price momentum indicator on hot rolled steel points to Neutral until the market establishes a clear direction.

Hot Rolled Lead Times: 4-8 weeks

Cold Rolled Coil: SMU price range is $1,800-$1,890 per net ton ($90.00-$94.50/cwt) with an average of $1,845 per ton ($92.25/cwt) FOB mill, east of the Rockies. The lower end of our range increased $10 per ton compared to last week, while the upper end declined $10 per ton. Our overall average is unchanged compared to one week ago. Our price momentum indicator on cold rolled steel points to Neutral until the market establishes a clear direction.

Cold Rolled Lead Times: 5-9 weeks

Galvanized Coil: SMU price range is $1,780-$1,880 per net ton ($89.00-$94.00/cwt) with an average of $1,830 per ton ($91.50/cwt) FOB mill, east of the Rockies. The lower end of our range declined $20 per ton compared to one week ago, while the upper end decreased $40 per ton. Our overall average is down $30 per ton from last week. Our price momentum indicator on galvanized steel points to Neutral until the market establishes a clear direction.

Galvanized .060” G90 Benchmark: SMU price range is $1,886-$1,986 per ton with an average of $1,936 per ton FOB mill, east of the Rockies.

Galvanized Lead Times: 5-10 weeks

Galvalume Coil: SMU price range is $1,780-$1,890 per net ton ($89.00-$94.50/cwt) with an average of $1,835 per ton ($91.75/cwt) FOB mill, east of the Rockies. The lower end of our range decreased $50 per ton compared to last week, while the upper end decreased $20 per ton. Our overall average is down $35 per ton from one week ago. Our price momentum indicator on Galvalume steel points to Neutral until the market establishes a clear direction.

Galvalume .0142” AZ50, Grade 80 Benchmark: SMU price range is $2,099-$2,209 per ton with an average of $2,154 per ton FOB mill, east of the Rockies.

Galvalume Lead Times: 8-11 weeks

Plate: SMU price range is $1,910-$1,960 per net ton ($95.50-$98.00/cwt) with an average of $1,935 per ton ($96.75/cwt) FOB mill. Both the lower and upper ends of our range increased $10 per ton compared to one week ago. Our overall average is up $10 per ton from last week. Our price momentum indicator on plate steel points to Neutral until the market establishes a clear direction

Plate Lead Times: 5-8 weeks

SMU Note: Below is a graphic showing our hot rolled, cold rolled, galvanized, Galvalume, and plate price history. This data is available here on our website with our interactive pricing tool. If you need help navigating the website or need to know your login information, contact us at info@SteelMarketUpdate.com.

By Brett Linton, Brett@SteelMarketUpdate.com