Market Data

June 3, 2022

US GDP Contracts Further in Q1's 2nd Review

Written by David Schollaert

The US economy contracted in the first quarter of 2022 at a worse rate than expected with gross domestic production declining at a -1.5% annualized pace, according to the second estimate from the US Commerce Department’s Bureau of Economic Analysis (BEA).

The second review for Q1 was a slight downward revision from its first estimate of -1.4%, the worst since the pandemic-induced recession in 2020. The drop was a sharp reversal from an annual growth rate of 6.9% from October through December, the best performance since 1984.

Multiple factors weighed against growth during the first three months of the year. Weak business and private investment failed to offset strong consumer spending. Downward revisions for both private inventory and residential investment offset an upward change in consumer spending. A rising trade deficit also subtracted from the GDP total.

Consumer spending as gauged by personal consumption expenditures increased 3.1%, better than the first estimate of 2.7%. Despite the downgrade, the labor market has remained strong and wages are increasing rapidly, albeit still below the pace of inflation.

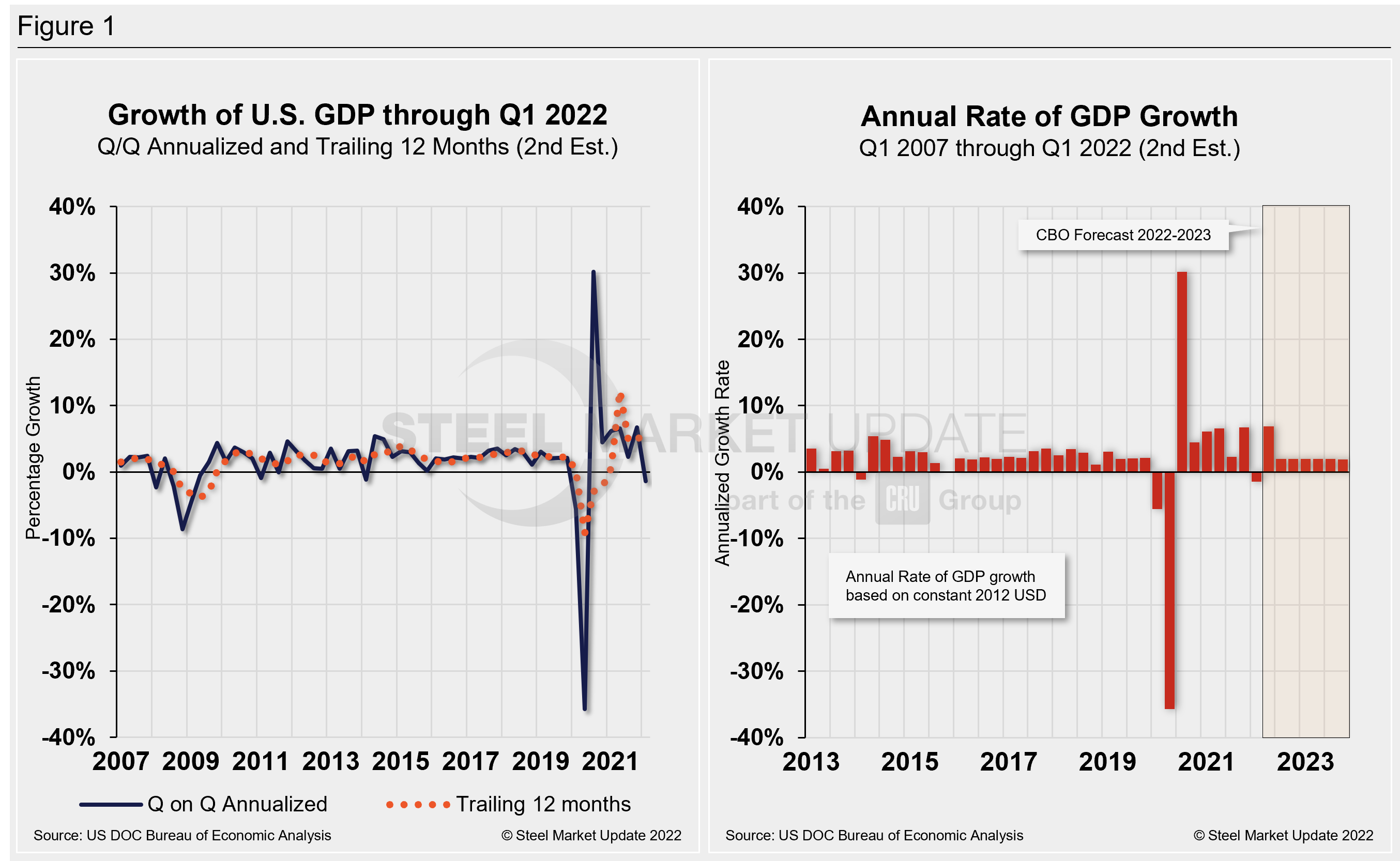

Commerce’s second look put total US GDP in Q4 at $24.38 trillion, a 6.5% increase, or $381.5 billion, over the previous quarter. Below in Figure 1 is a side-by-side comparison of US GDP growth and the annual rate of GDP, both through Q1 2022. In the first chart, you’ll see the contrast between the trailing 12-month growth and the headline quarterly result. The chart on the right details the headline quarterly results since Q1 2007, including the Congressional Budget Office’s GDP projection through 2023.

On a trailing 12-month basis, GDP accelerated to 3.57% in the first quarter, down from 5.53% in the prior quarter but still well behind 12.23% growth in Q2. Yet, it’s a vast improvement from -9.27% in Q2 2020 at the height of the pandemic. For comparison, the average in 49 quarters since Q1 2010 has been a growth rate of 2.17%.

Two years after the pandemic first struck, the US economy faces many challenges, including supply disruptions related to the pandemic and the war in Ukraine, labor shortages, and high inflation.

Current forecasts estimate GDP to rise 2.3% in the second quarter and 2.5% for all of 2022. That’s still a sharp decline from the original 4.2% growth estimate signaled at the beginning of the year, according to a survey from the Federal Reserve Bank of Philadelphia.

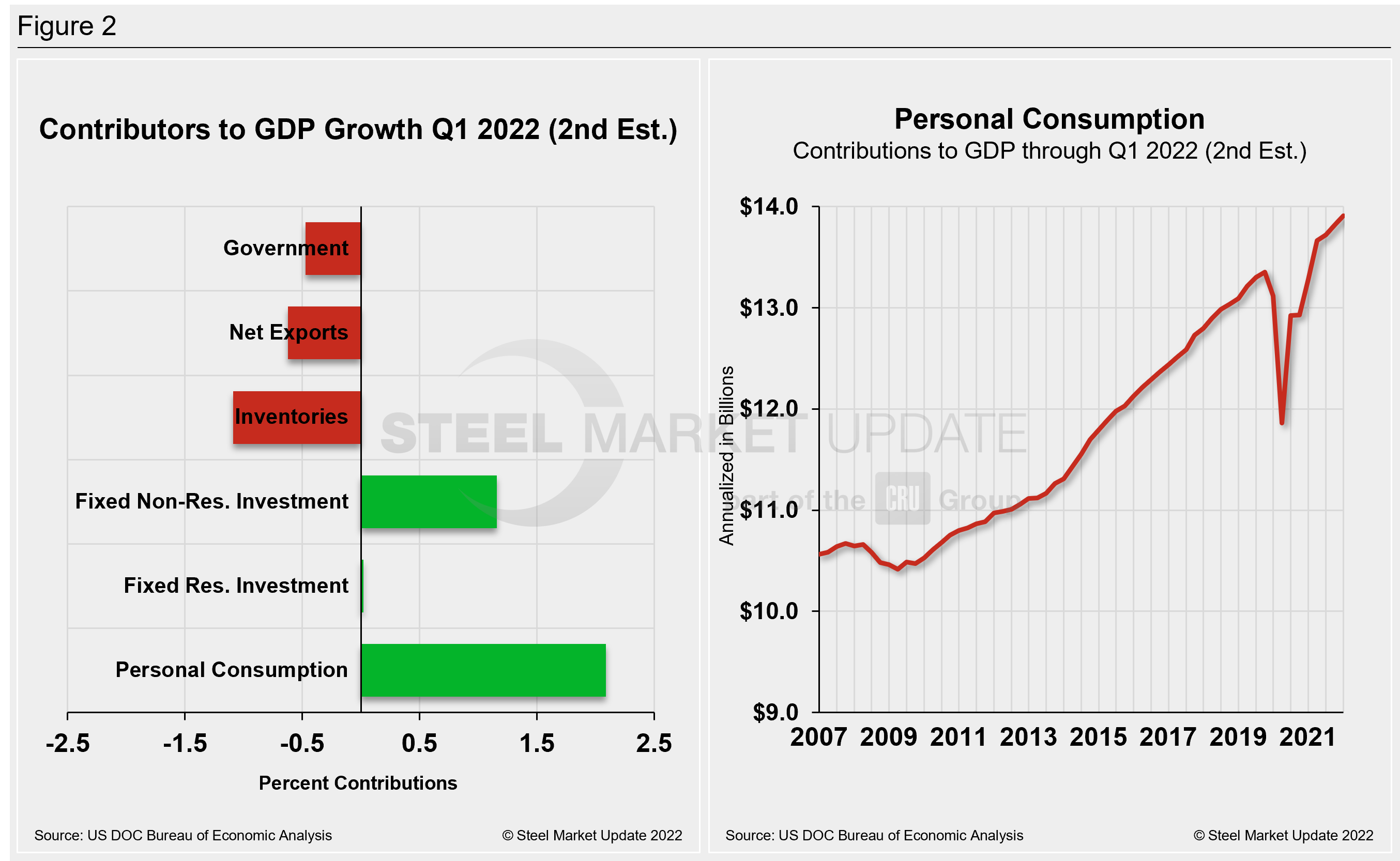

Shown below in Figure 2 is a side-by-side comparison of two charts. On the left is the mix of the six major components in the GDP growth calculation. The chart on the right puts a spotlight on personal consumption, a measure of consumer confidence and spending engagement.

The most notable change and a major source of GDP fluctuation is personal consumption, which has experienced extreme swings since the onset of Covid. It has been resilient more recently, and a bright spot despite inflation headwinds.

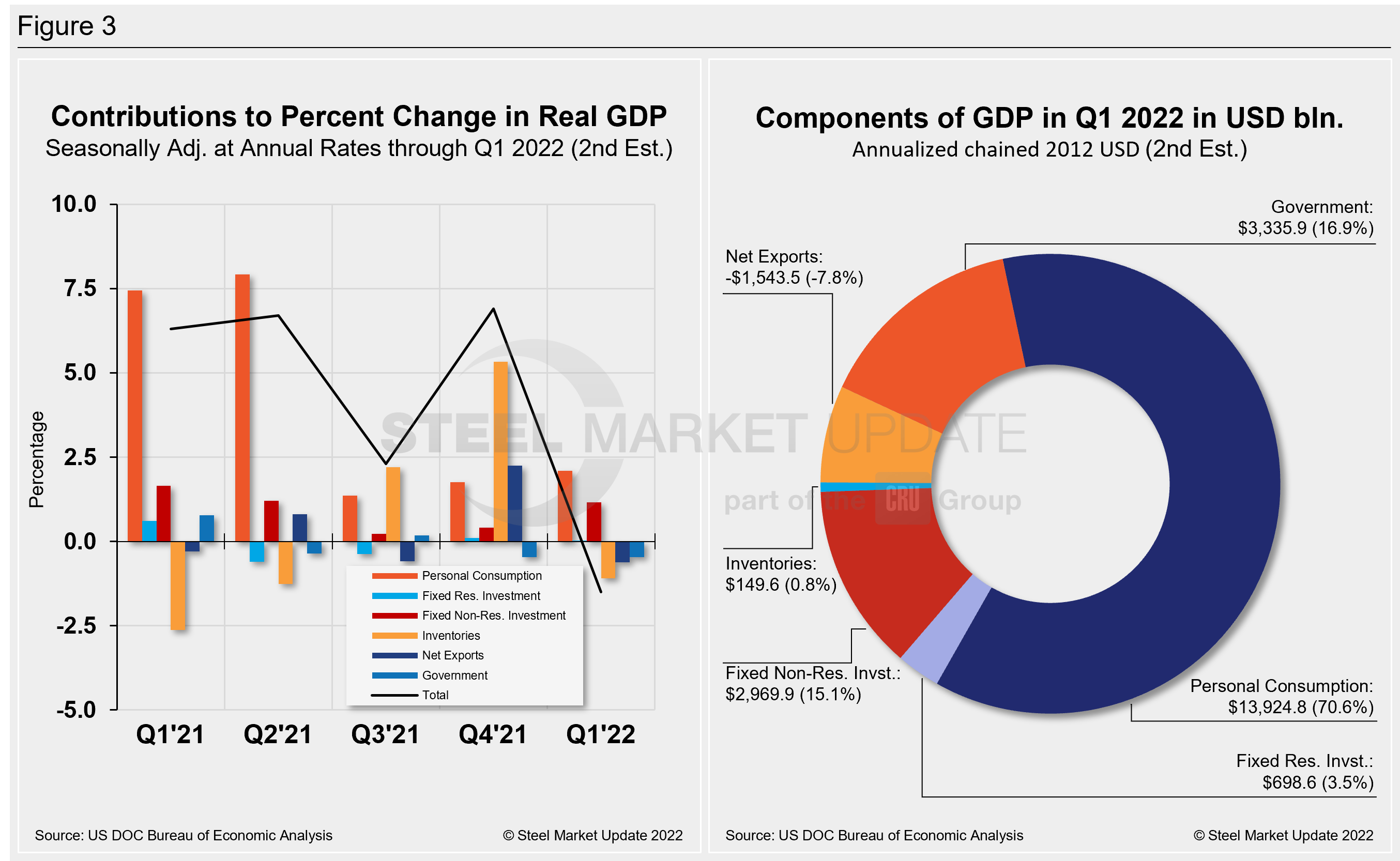

The quarterly contributions of the six major subcomponents of GDP since Q4 2020 and the breakdown of the $24.38 trillion economy in BEA’s second review of Q1 GDP are both shown in Figure 3. The chart on the left is for cross-comparison with Figure 1 above. The chart on the right shows the size of the other components relative to personal consumption.

By David Schollaert, David@SteelMarketUpdate.com