Prices

June 17, 2022

HRC-Scrap Spread Shrinking as Prices Decline

Written by Brett Linton

The spread between hot-rolled coil (HRC) and prime scrap prices is resuming the downward trend seen prior to the Russia-Ukraine war, according to the latest Steel Market Update data. The HRC-scrap spread reached an 18-month low in early March. The latest spread, calculated through June 14, is less than half what it was this time last year but is still higher than pre-pandemic levels.

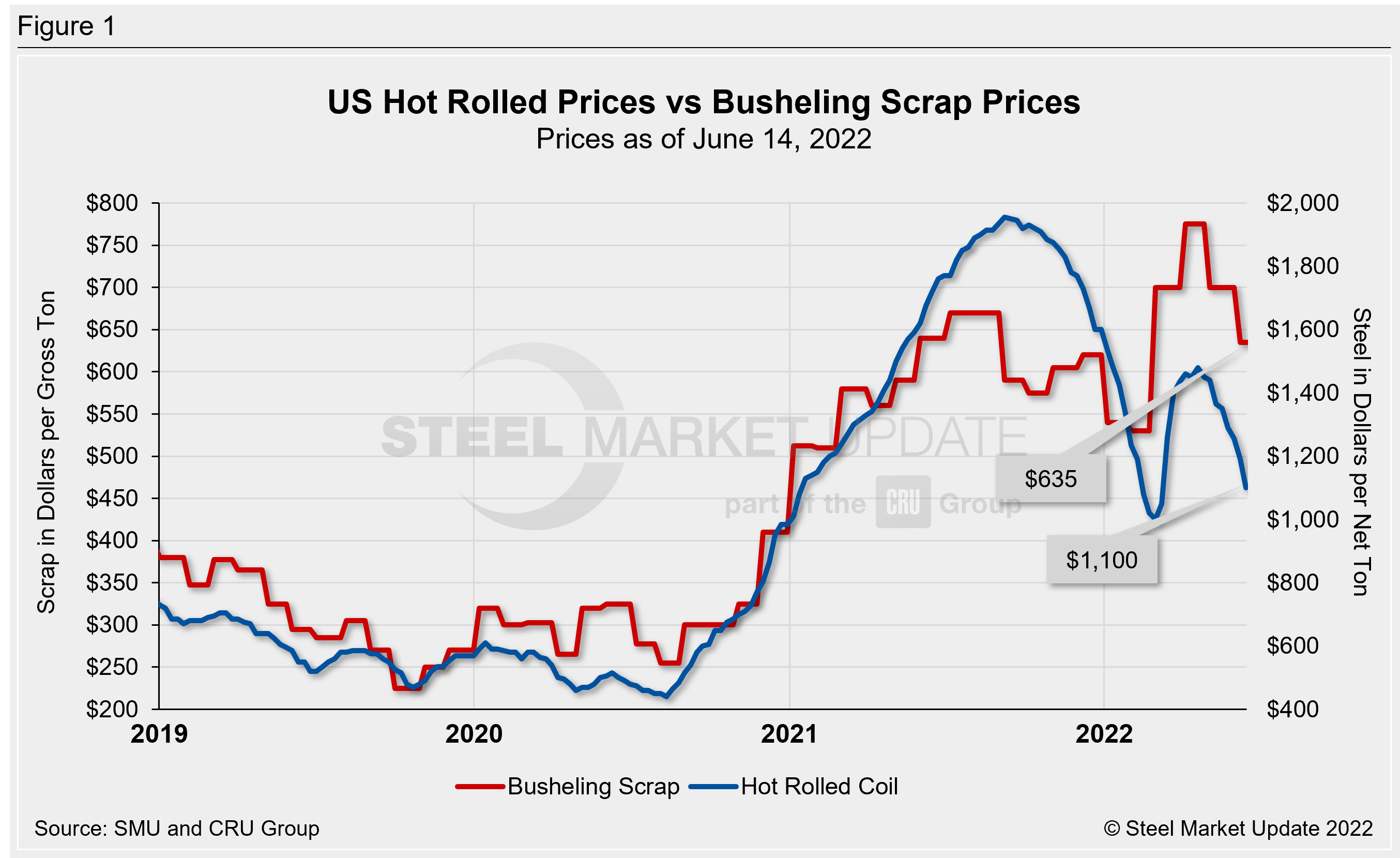

The SMU hot rolled coil price average fell $90 per ton to $1,100 per net ton ($55.00 per cwt) as of last Tuesday, and is now at a 14-week low. This was the largest week-over-week decline in steel prices since mid-February. Recall our HRC price peaked last September at $1,955 per ton, gradually falling to a low of $1,000 per ton in early-March. HRC prices then rapidly rose following the Russia-Ukraine war to $1,480 per ton in mid-April.

Busheling scrap prices settled last week at $635 per gross ton for June, down $65 per ton from May and down $140 per ton from April’s historical high. Prior to 2022, the previous high for busheling was $670 per ton in July and August 2021. Figure 1 shows price histories for each product.

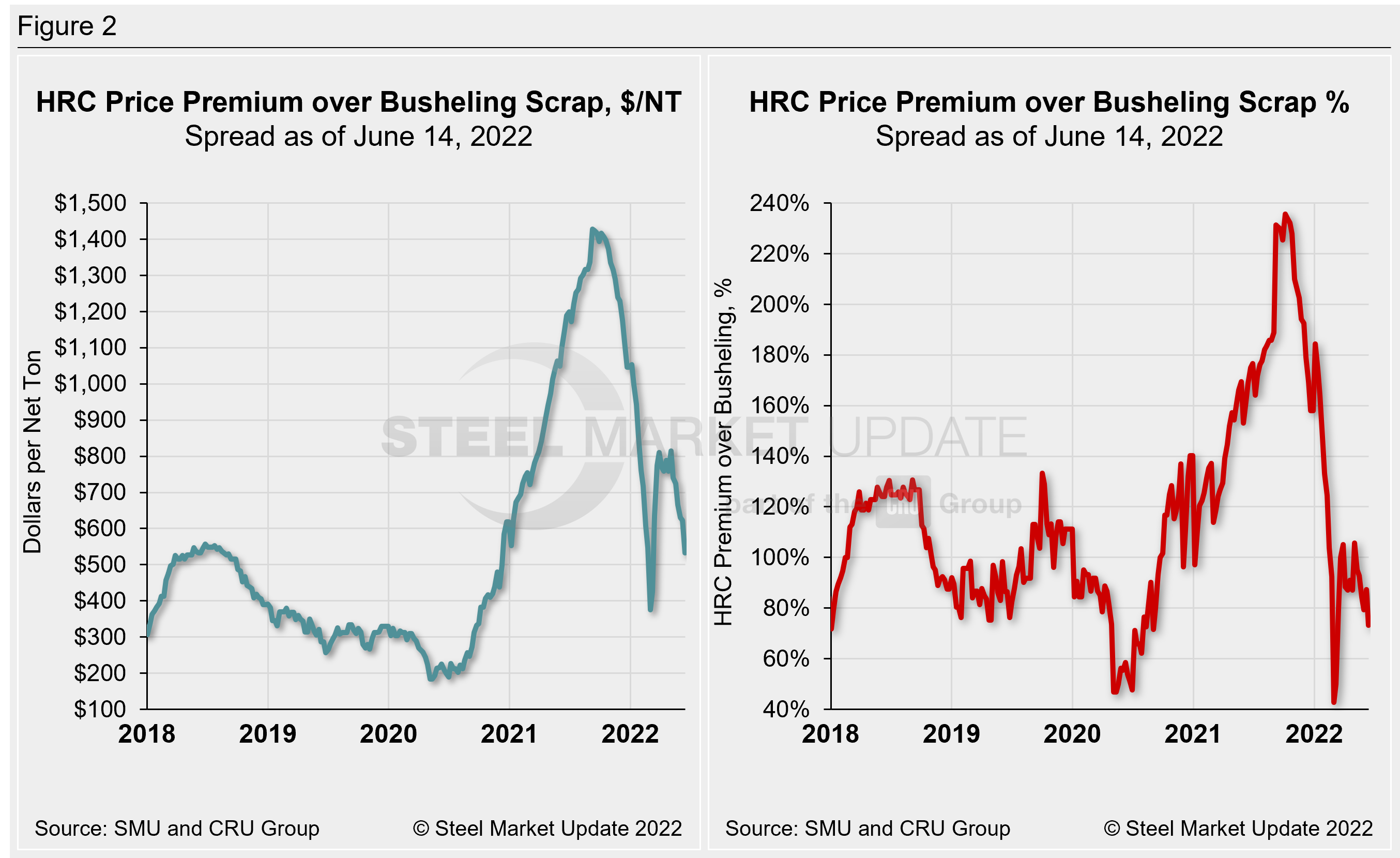

Converting scrap prices to dollars per net ton for an apples-to-apples comparison, the differential between hot rolled coil and busheling scrap prices is now $533 per net ton, as shown in the left chart of Figure 2. The spread has averaged $613 per ton over the last four weeks, having peaked at $815 per ton in early May. Recall we saw an 18-month low spread of $375 per ton in early March, and a record-high spread of $1,428 per ton six months prior to that. This time last year, the spread was $1,149 per ton, while in June 2020 it was just $210 per ton. For comparison, the average spread throughout 2021 was $1,080 per ton, with 2020 averaging $310 and 2019 averaging $324.

PSA: Did you know our Interactive Pricing Tool has the capability to show steel and scrap prices in dollars per net ton, dollars per metric ton, and dollars per gross ton?

The right chart in Figure 2 explores this relationship in a different way – we have graphed the spread between hot rolled coil and busheling scrap prices as a percentage premium over scrap prices. HRC prices now carry a 73% premium over prime scrap, having reached 105% in late March. Weeks prior to that, in early March, this premium reached a low of 43%, having fallen from a record 236% last October. This time last year, HRC held a 169% premium over scrap, while June 2020 saw a 54% premium. HRC held the lowest premium over busheling scrap back in November 2011, when it reached 29%.

This comparison was inspired by reader suggestions; if you would like to chime in with topics you want us to explore, reach out to our team at News@SteelMarketUpdate.com.

By Brett Linton, Brett@SteelMarketUpdate.com