Prices

June 24, 2022

Raw Materials Prices Decline Through June

Written by Brett Linton

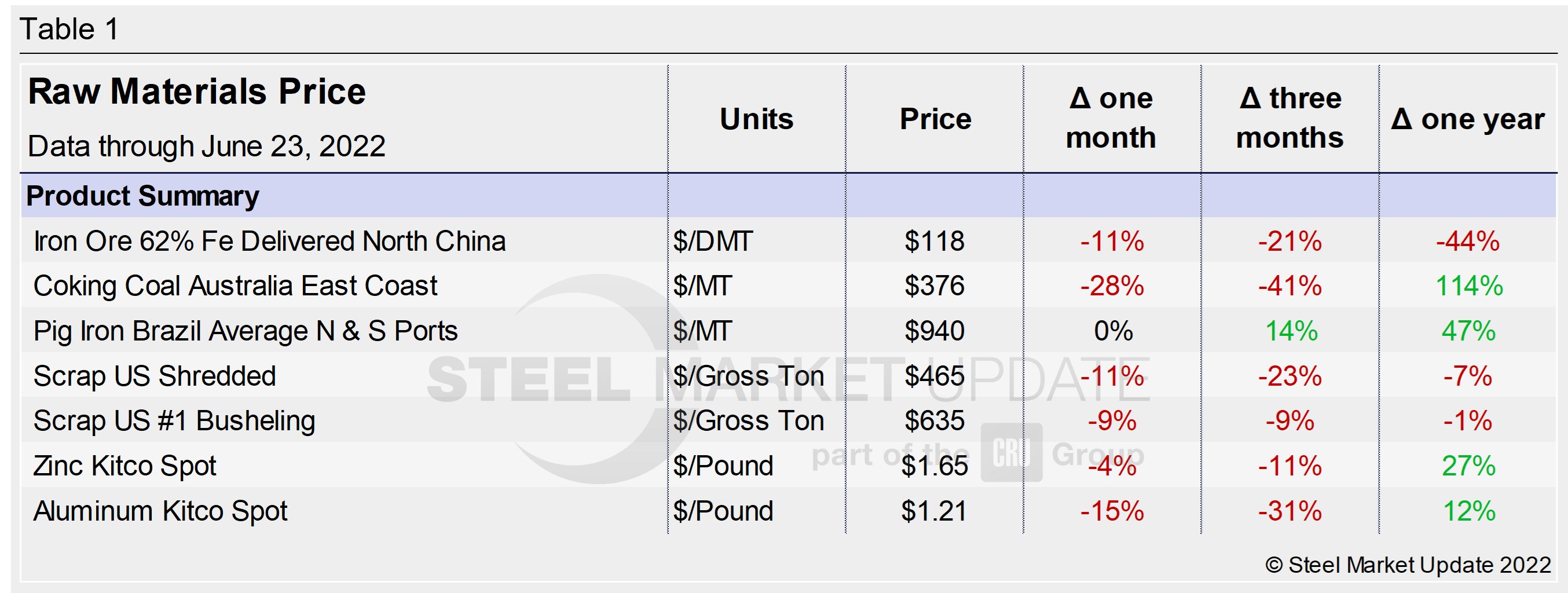

Prices for six of the seven steelmaking raw materials tracked in this SMU analysis declined over the last 30 days, again receding from record-high levels seen 2-3 months prior. Through the latest data available as of June 23, coking coal prices decreased 28% compared to one month prior, aluminum prices fell 15%, iron ore and shredded scrap prices were both down 11%, busheling scrap prices declined 9%, and zinc prices eased 4%. Pig iron was the only product that did not decline, remaining unchanged from May.

Table 1 summarizes the price changes of the seven materials considered in this analysis. It reports the percentage change from one month prior, three months prior, and one year prior for each product.

Iron Ore

After rising to record-high levels last summer, the Chinese import price of 62% Fe content iron ore fines declined to an 18-month low last November. Prices then increased through April but have since began to decline. Figure 1 shows the price of 62% Fe delivered North China at $118 per dry metric ton as of June 22, now in line with levels last seen in December 2021. Iron ore prices have decreased 11% in the last 30 days, down 21% compared to three months prior, and down 44% from the record-high prices seen this time last year.

Coking Coal

The price of premium hard coking coal FOB east coast of Australia surged in March to a record high of $660 per dry metric ton, with the latest figure down 43% from that peak to $376 per ton (Figure 2). Prices have decreased 28% in the last 30 days, down 41% compared to three months prior, but up 114% from prices one year ago. In 2021, coking coal prices reached a record-high $405 per ton in October/ November. Prior to that, the average coking coal price in 2019-2020 was $151 per ton, and the previous record for coking coal prices was $400 per ton in July 2008.

Pig Iron

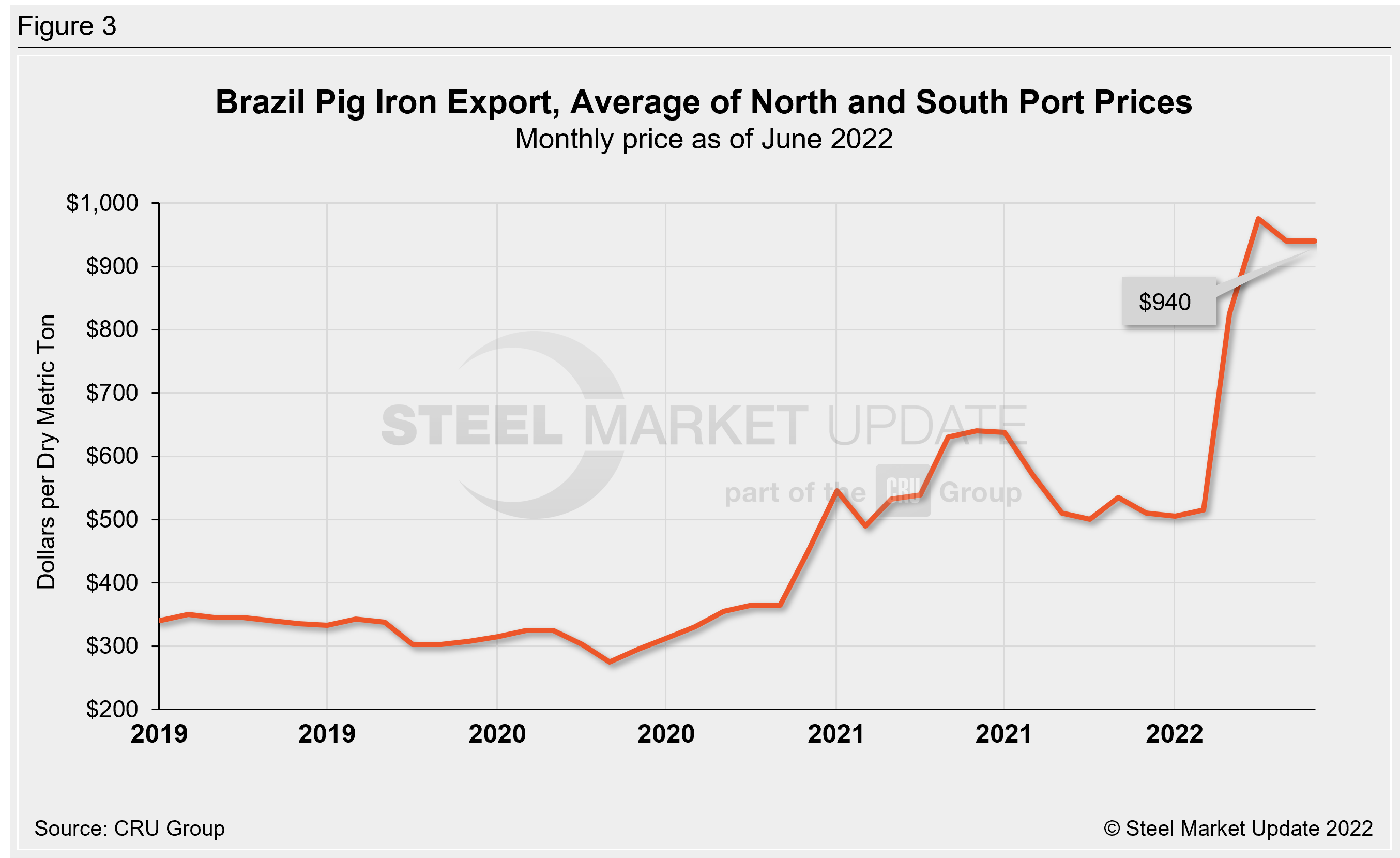

Most of the pig iron imported to the US had come from Russia, Ukraine and Brazil. This report summarizes prices out of Brazil and averages the FOB value from the north and south ports. Pig iron prices had been elevated but relatively stable for most of 2021 and early 2022. Prices jumped 60% in March following the invasion of Ukraine by Russian forces – which limited or halted supplies from both nations. April saw record-high pig iron prices at $975 per metric ton. The average price for June is unchanged from May at $940 per metric ton, up 14% from three months ago and up 47% from one year prior. Recall that pig iron prices had reached a multiyear low of $275 per metric ton in June 2020 (Figure 3).

Scrap

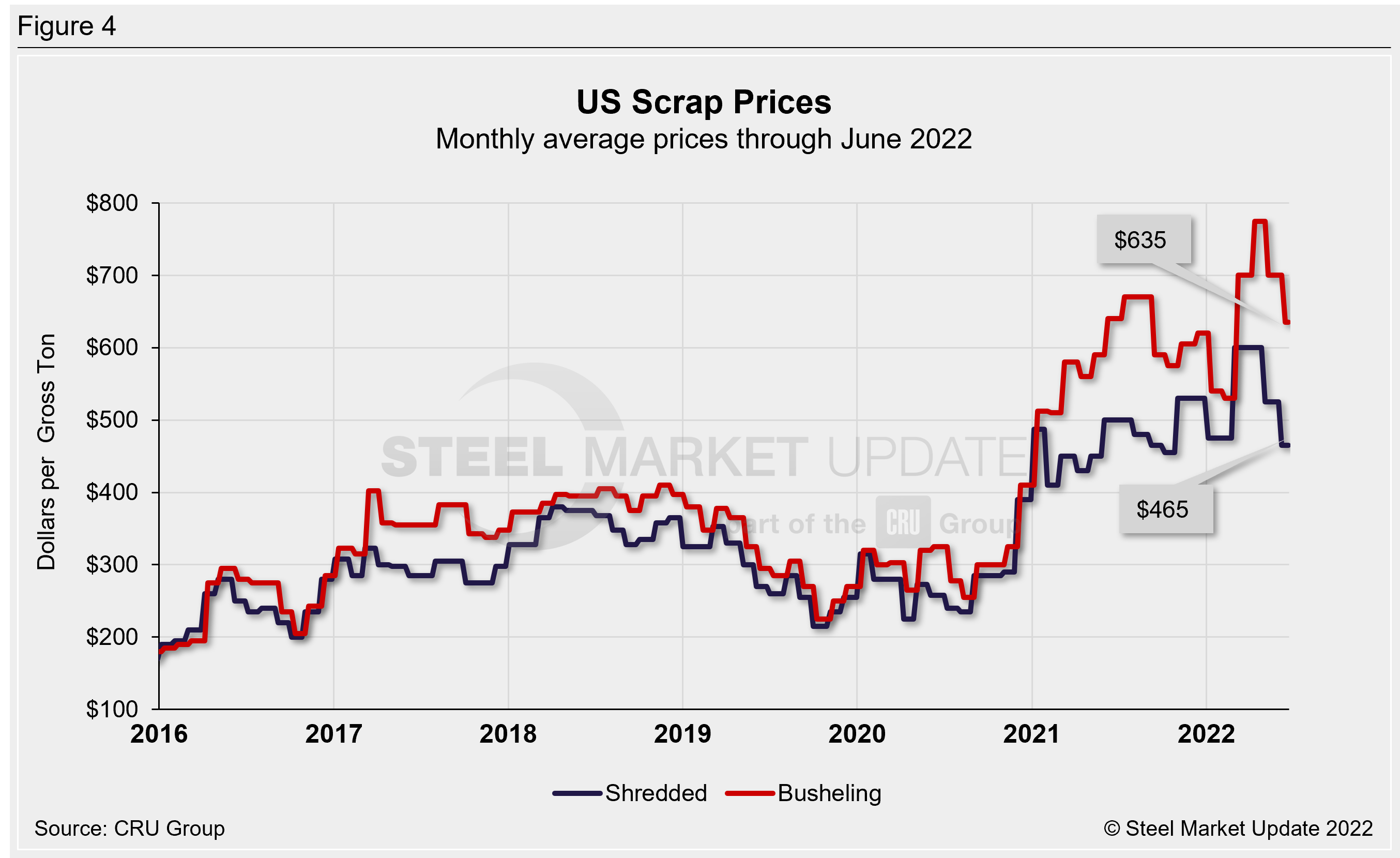

Hot rolled steel prices fluctuate up and down with the price the mills must pay for their raw materials. Changes in the relationship between scrap and iron ore prices offer insights into the competitiveness of integrated mills, whose primary feedstock is iron ore, versus the minimills, whose primary feedstock is scrap. Figure 4 shows the spread between shredded and busheling scrap, priced in dollars per gross ton in the Great Lakes region.

Scrap prices declined $60-65 per ton in June, busheling scrap prices fell to $635 per gross ton, and shredded scrap prices declined to $465 per ton. Recall that March and April saw record-high scrap prices, with busheling reaching $775 per ton and shred $600 per ton. Prior to 2021, the previous record for scrap prices over the last decade was $510 per ton for busheling in 2011 and $473 per ton for shredded in 2012. Our scrap sources expect prices to ease again in July.

Figure 5 shows the prices of mill raw materials over the past four years. Iron ore prices are 47% below the June 2021 peak of $221 per dry metric ton, while shredded scrap prices are down 7% year over year.

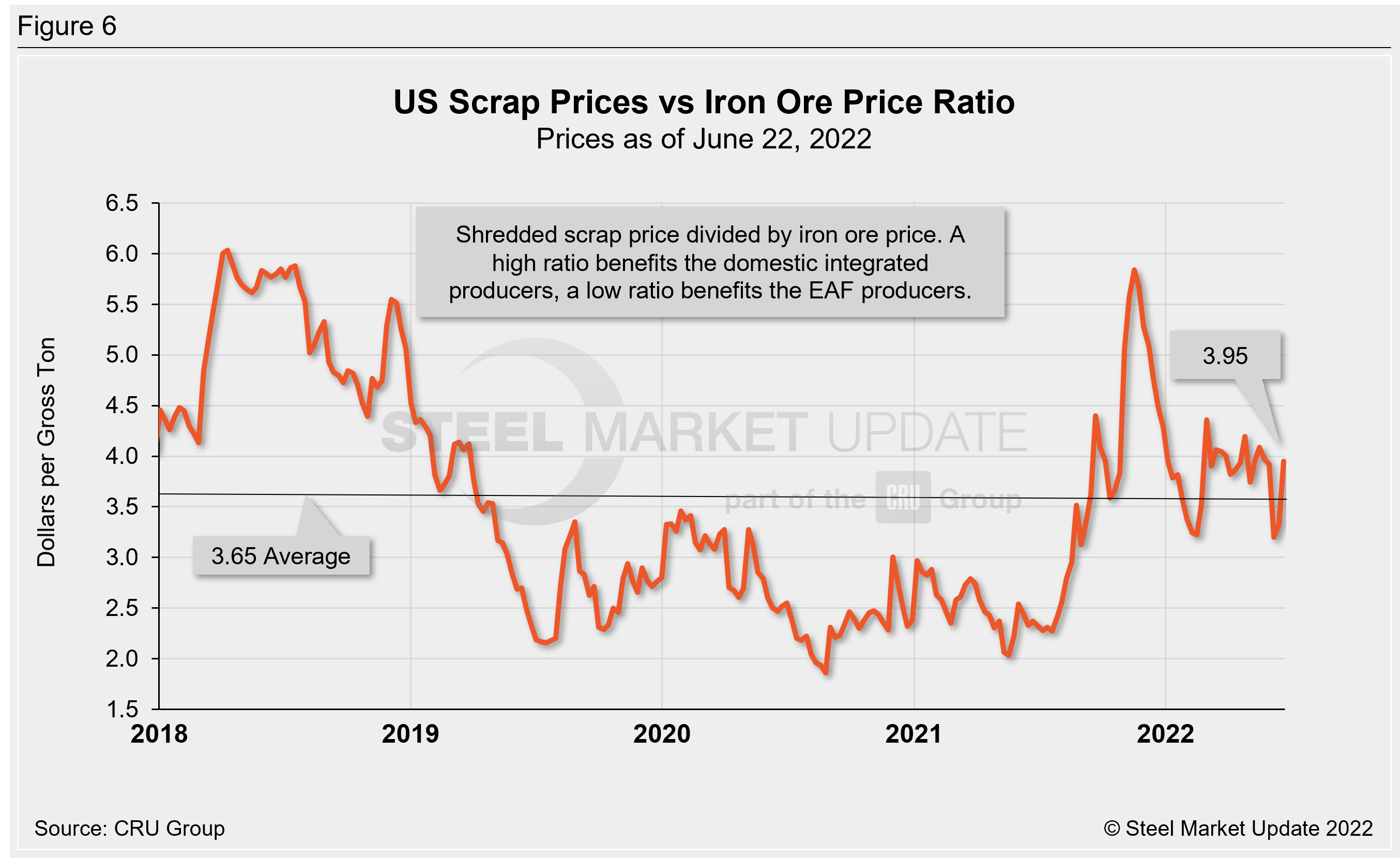

To compare the two, Steel Market Update divides the shredded scrap price by the iron ore price to calculate a ratio (Figure 6). A high ratio favors the integrated/BF producers, a lower ratio favors the minimill/EAF producers. At the current 3.95 ratio shown below, integrated producers currently hold the cost advantage and have mostly held this position since early March. Seven months ago we saw a ratio of 5.84, the highest seen since mid-2018. The scrap to iron ore ratio reached a record low of 1.86 in August 2020 (within SMU’s 12-year data history).

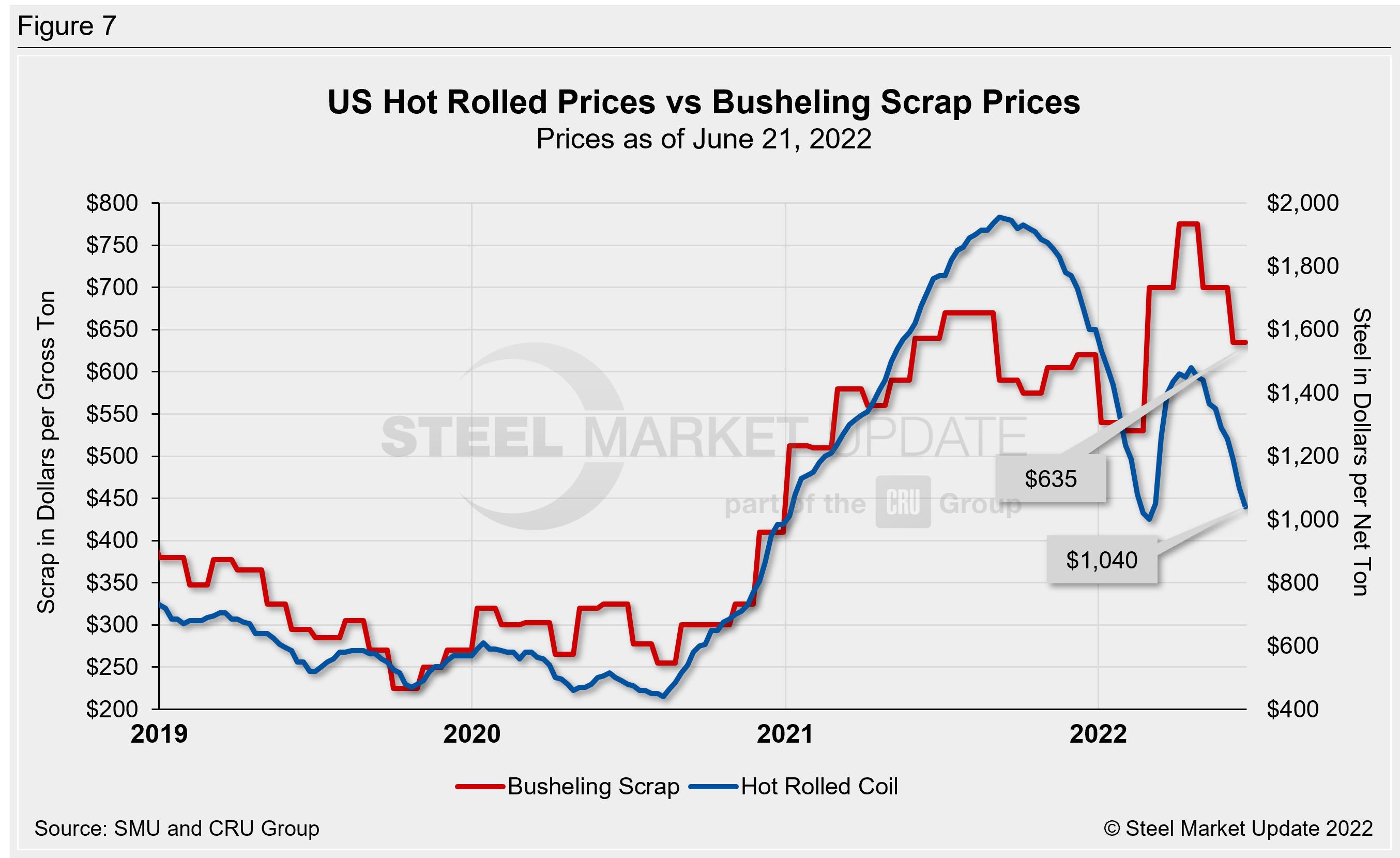

Figure 7 shows how the price of hot rolled steel generally tracks with the price of busheling scrap. Bush fell $60 per gross ton from May to June, back in line with levels seen this time last year. As of Tuesday, the SMU hot rolled price average decreased $60 per ton week over week to $1,040 per ton. This is a decrease of $250 per ton compared to one month ago, nearing prices seen in late February and early March, and down $720 per ton compared to levels seen one year prior.

Zinc and Aluminum

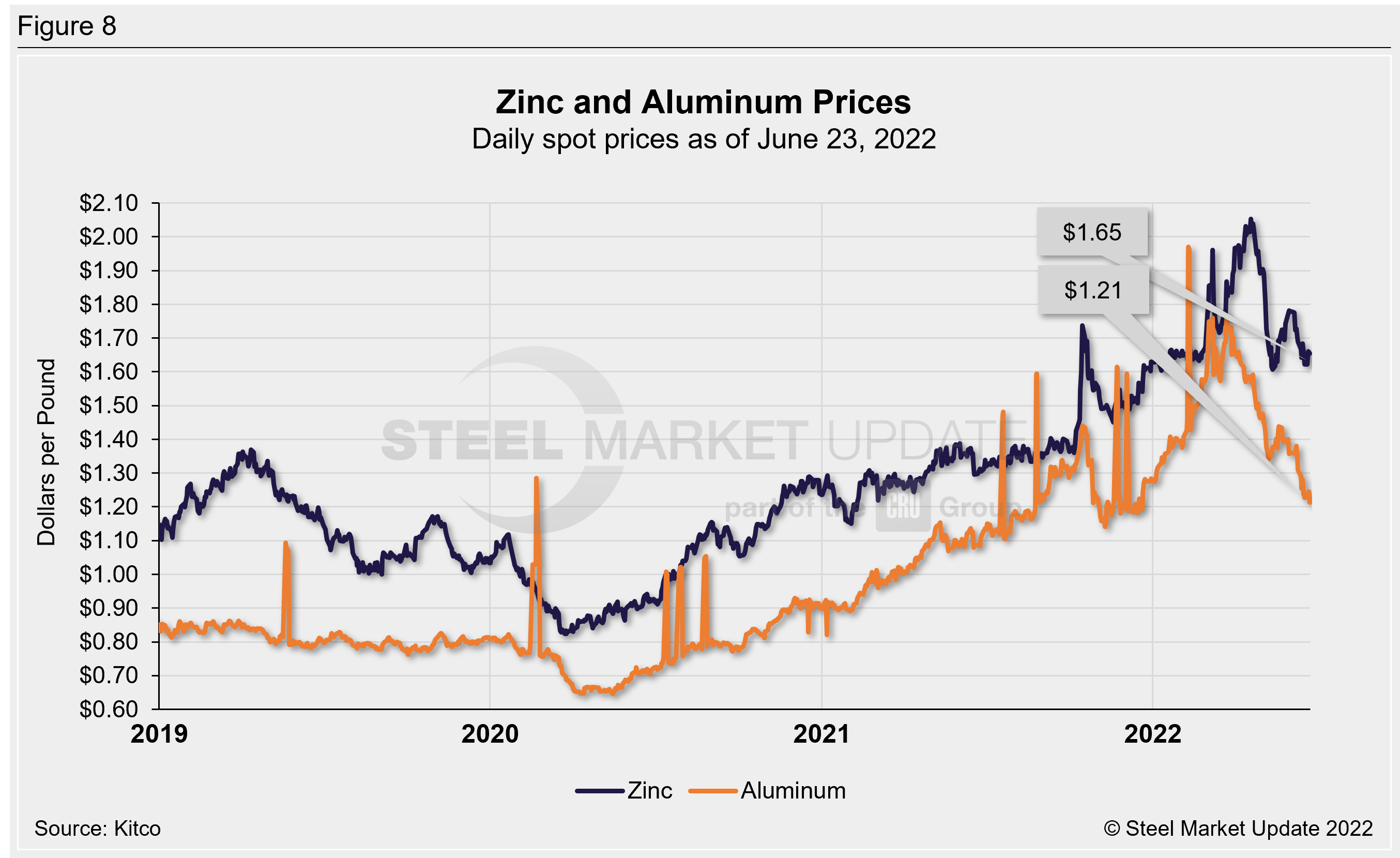

Zinc, used to make galvanized and other products, had rapidly increased in price in March and April, causing many mills to adjust their galvanized coating extras higher at that time. The LME cash price for zinc surpassed $2 per pound on May 13 and peaked at $2.04 per pound as of May 21. Zinc prices have since declined, with the May 13 price falling to a four-month low of $1.61 per pound. The latest price as of June 23 is up to $1.65 per pound, down 11% compared to three months prior but up 27% from levels one year ago (Figure 8).

Aluminum prices, which factor into the price of Galvalume, had been on the rise in 2021 and early 2022, reaching a record-high of $1.76 per pound on March 23. (Note that aluminum spot prices often have large swings and return to typical levels within a few days, as seen in the graphic below. We do not consider those surges in our overall high/low comparisons.) Aluminum prices began to decline in late March and are now at a six-month low of $1.21 per pound as of June 23. This is down 31% from the March record, but up 12% from prices one year prior.

By Brett Linton, Brett@SteelMarketUpdate.com