Prices

November 22, 2022

SMU Price Ranges: Big Buyers Jump in Hoping for Floor

Written by Michael Cowden

SMU’s sheet prices slipped again this week. But some market participants predicted that sheet was at or near a bottom.

The anticipation of that bottom appeared to pull some big buyers off the sidelines. Large purchases from some pulled the low end of our hot-rolled coil range below $600 per ton ($30 per cwt) and the low end of our cold rolled and galvanized range below $800 per ton.

Such buying — big tons at low prices — often occurs shortly ahead of mill price increase announcements. And some sources think another round is likely in late November or early December as more lead times stretch into January.

Weighing against bullishness about higher prices are continued concerns about demand and about scrap prices. Prime scrap prices remain below shredded scrap, the inverse of the typical structure of the scrap market and perhaps an indication of a glut.

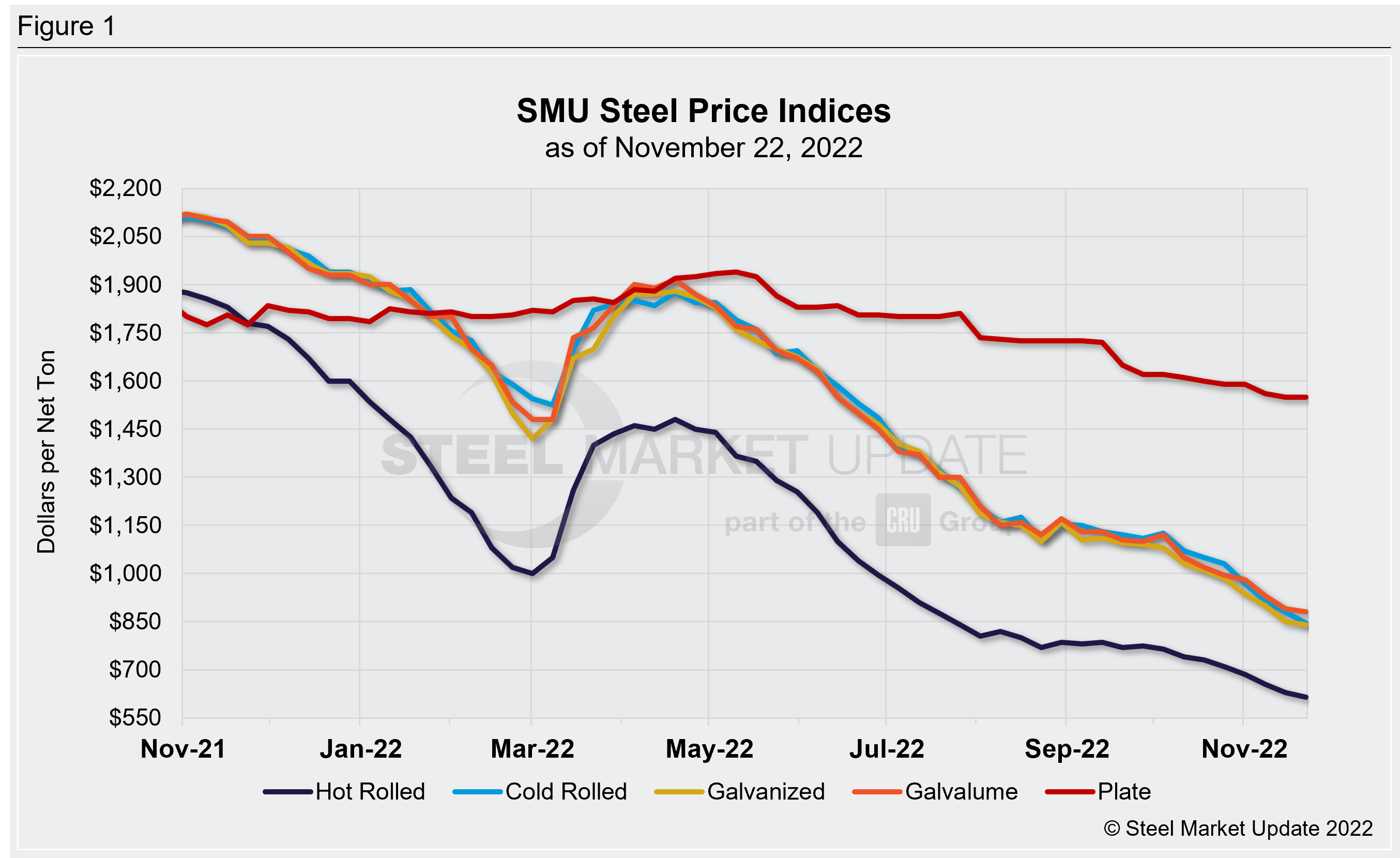

All told, our average HRC price stands at $615 per ton, down $15/ton week-over-week (WoW). Cold rolled is at $845 per ton (-$35/ton WoW), galvanized is at $840 per ton (-$10/ton), and Galvalume is at $800 (-$10/ton). Plate prices are unchanged.

Our price momentum indicators continue to point to Lower. But we are keeping an eye out for any signs of an inflection point.

Hot-Rolled Coil: The SMU price range is $580–650 per net ton ($29.00–32.50/cwt) with an average of $615 per ton ($30.75/cwt) FOB mill, east of the Rockies. The lower end of our range decreased $20 per ton compared to one week ago, while the upper end decreased $10 per ton. Our overall average is down $15 per ton from last week. Our price momentum indicator on hot-rolled steel points to Lower, meaning we expect prices to decrease over the next 30 days.

Hot-Rolled Lead Times: 3–6 weeks

Cold-Rolled Coil: The SMU price range is $790–900 per net ton ($39.50–45.00/cwt) with an average of $845 per ton ($42.25/cwt) FOB mill, east of the Rockies. The lower end of our range decreased $30 per ton compared to last week, while the upper end decreased $40 per ton. Our overall average is down $35 per ton from one week ago. Our price momentum indicator on cold-rolled steel points to Lower, meaning we expect prices to decrease over the next 30 days.

Cold-Rolled Lead Times: 4–7 weeks

Galvanized Coil: The SMU price range is $780–900 per net ton ($39.00–45.00/cwt) with an average of $840 per ton ($42.00/cwt) FOB mill, east of the Rockies. The lower end of our range decreased $20 per ton compared to one week ago, while the upper end remained unchanged. Our overall average is down $10 per ton from last week. Our price momentum indicator on galvanized steel points to Lower, meaning we expect prices to decrease over the next 30 days.

Galvanized .060” G90 Benchmark: SMU price range is $877–997 per ton with an average of $937 per ton FOB mill, east of the Rockies.

Galvanized Lead Times: 4–7 weeks

Galvalume Coil: The SMU price range is $820–940 per net ton ($41.00-47.00/cwt) with an average of $880 per ton ($44.00/cwt) FOB mill, east of the Rockies. The lower end of our range decreased $40 per ton compared to last week, while the upper end increased $20 per ton. Our overall average is down $10 per ton from one week ago. Our price momentum indicator on Galvalume steel points to Lower, meaning we expect prices to decrease over the next 30 days.

Galvalume .0142” AZ50, Grade 80 Benchmark: SMU price range is $1,114–1,234 per ton with an average of $1,174 per ton FOB mill, east of the Rockies.

Galvalume Lead Times: 4–7 weeks

Plate: The SMU price range is $1,480–1,620 per net ton ($74.00–81.00/cwt) with an average of $1,550 per ton ($77.50/cwt) FOB mill. Both the lower and upper ends of our range remained unchanged compared to one week ago. Our overall average is unchanged from last week. Our price momentum indicator on steel plate points to Lower, meaning we expect prices to decrease over the next 30 days.

Plate Lead Times: 3–6 weeks

SMU Note: Below is a graphic showing our hot rolled, cold rolled, galvanized, Galvalume, and plate price history. This data is available here on our website with our interactive pricing tool. If you need help navigating the website or need to know your login information, contact us at info@SteelMarketUpdate.com.

By Michael Cowden, Michael@SteelMarketUpdate.com