Prices

December 1, 2022

October Steel Imports Up 7%, 3MMA Slips to 18-Month Low

Written by Brett Linton

Preliminary Census data indicates that steel imports will have totaled 2.41 million net tons for the month of October. While up 7% from the prior month, October levels are on the low side compared to the previous 18 months. Recall that monthly import levels declined 11% month-on-month (MoM) in September, having also fallen 6% both months before that. October figures are down 22% compared to March’s 26-month high of 3.09 million tons.

Broken down by product category, long product imports in October are preliminarily up 21% from the previous month. Semifinished product imports also rebounded 19% MoM. Imports of finished steel products rose 5% MoM, flat-rolled imports increased 3%, and stainless imports were up 1%. The only category to decrease MoM was pipe and tube, falling 2%.

Total November import licenses are currently at 1.79 million tons through Nov. 27th data, potentially the lowest level since December 2020 when imports were 1.50 million tons.

Although imports have declined for multiple months, average levels for this year are still relatively strong compared to recent years. The average monthly import rate for 2022 is now 2.66 million tons per month through preliminary October data. Compare this to the monthly averages of previous years: 2021 at 2.63 million tons, 2020 at 1.84 million tons, 2019 at 2.32 million tons, 2018 at 2.81 million tons, and 2017 at 3.17 million tons. The average import level over the last twelve months is now 2.70 million tons.

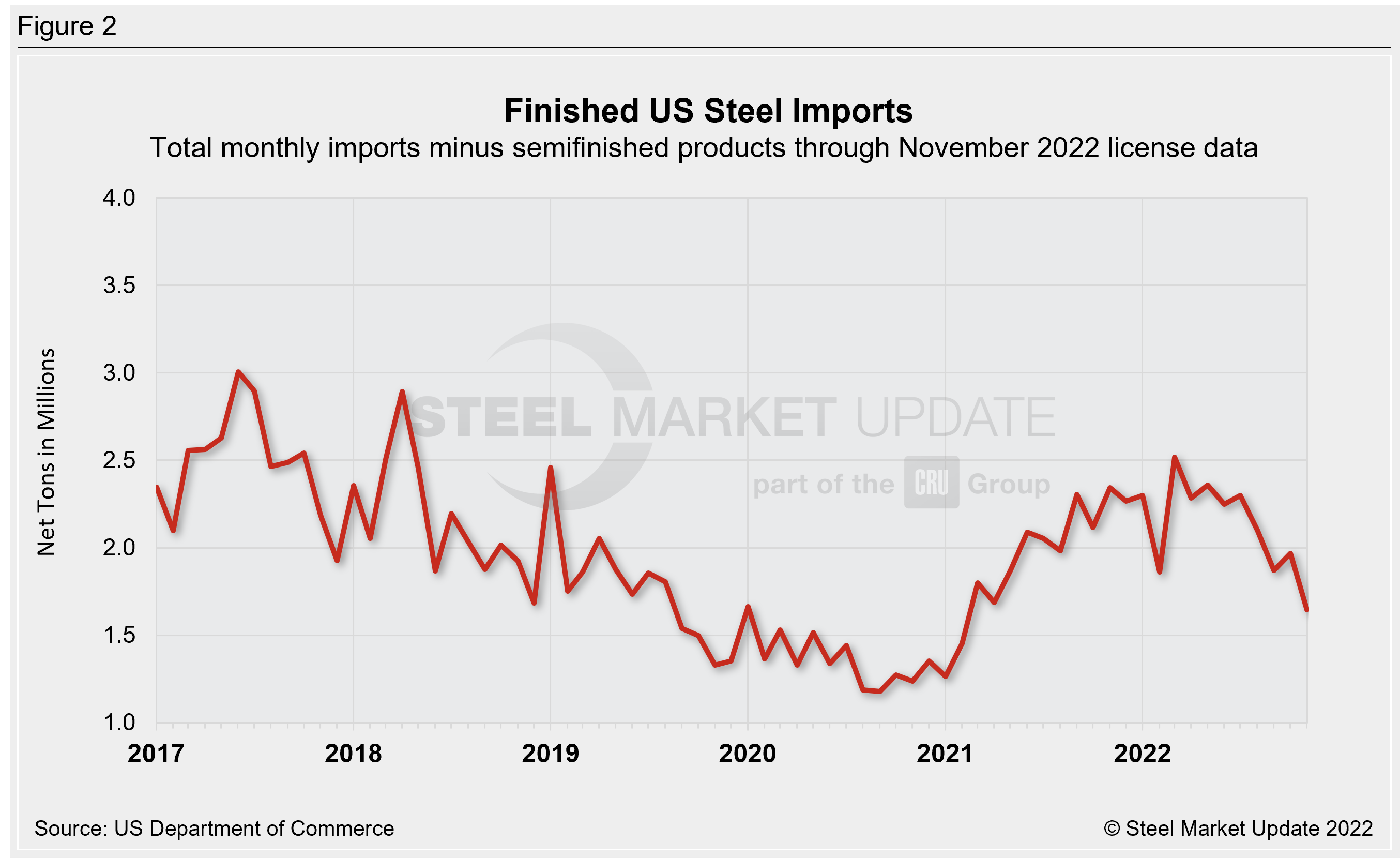

Preliminary imports of finished steels rose from 1.87 million tons in September to 1.97 million tons in October. The latest license data shows finished steel imports at 1.64 million tons in November, potentially the lowest level seen since February 2021.

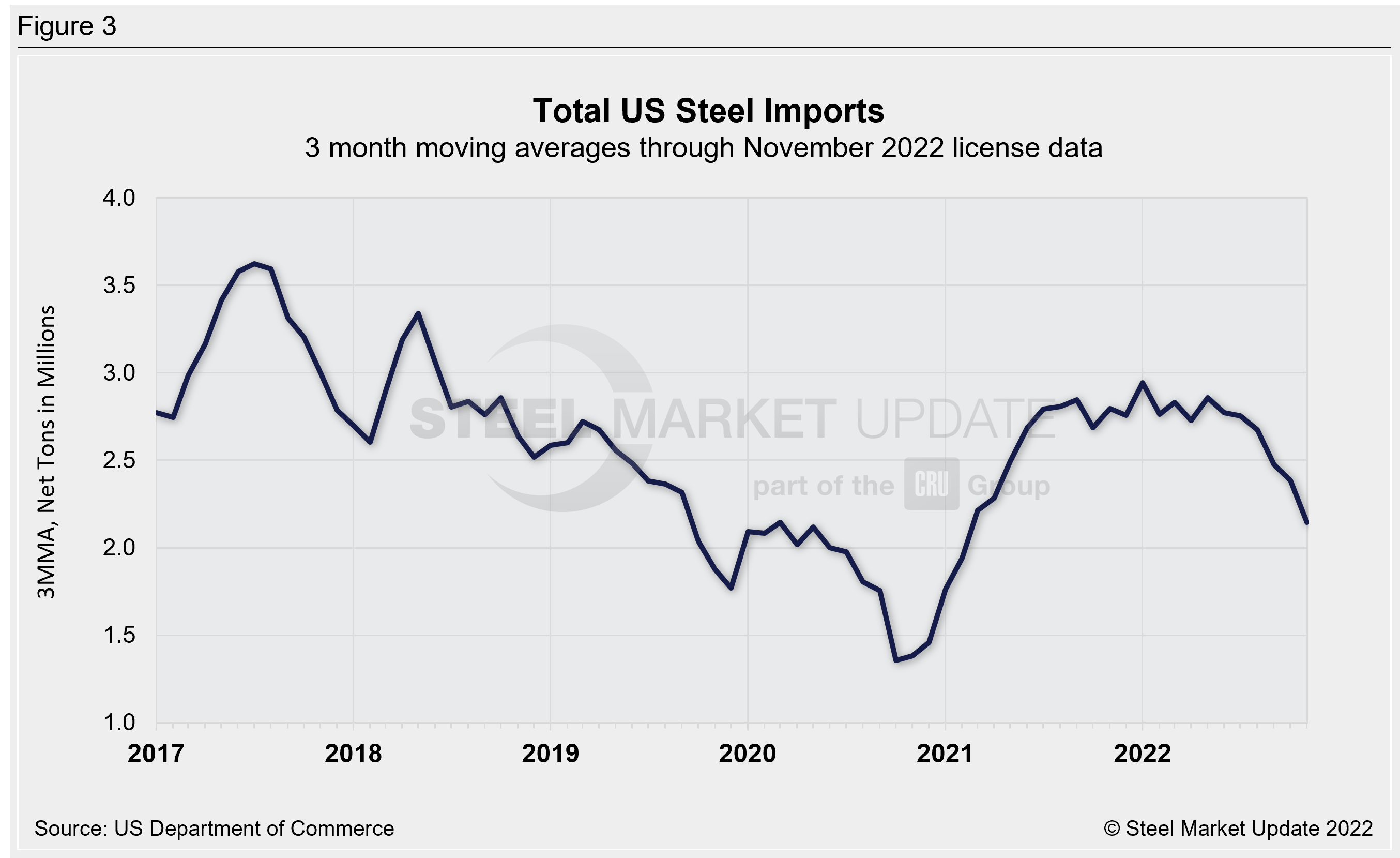

Due to large monthly swings in semifinished imports in recent years, the chart below shows total imports on a three-month moving average (3MMA) basis in an attempt to more accurately display trends. The 3MMA is 2.39 million tons through preliminary October figures, now at an 18-month low. November license data suggests that the 3MMA could decline to 2.14 million tons, potentially the lowest level since February 2021. Recall that in January of this year the 3MMA had reached a 42-month high of 2.94 million tons, while the lowest 3MMA level in SMU’s recent history was November 2020 at 1.36 million tons.

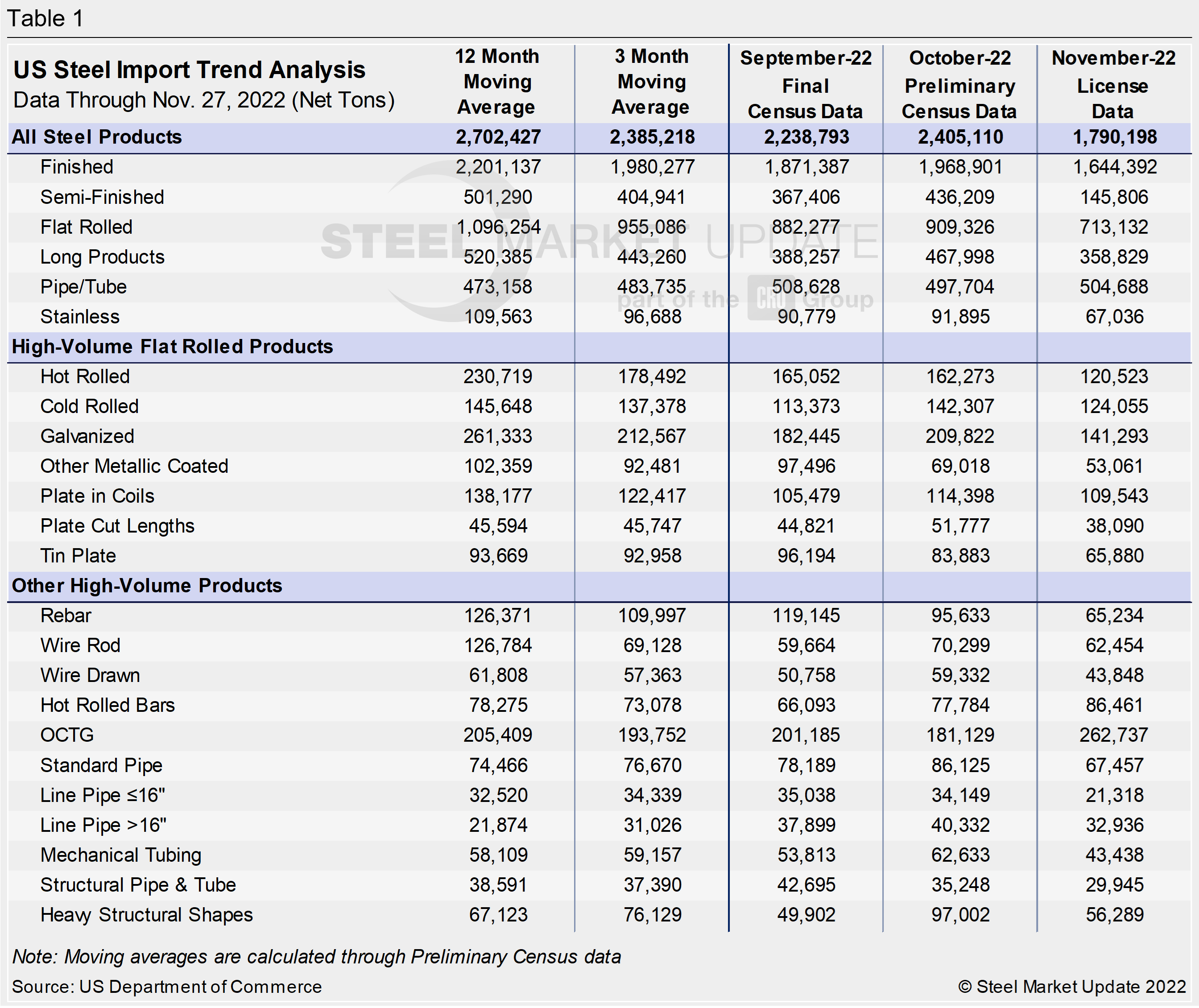

The table below displays flat-rolled product imports as well as other high-volume products, including rebar, tin plate, wire rod, structural pipe and tube, and other long products. We also provide data on imports divided into semifinished, finished, flat rolled, longs, pipe and tube, and stainless products.

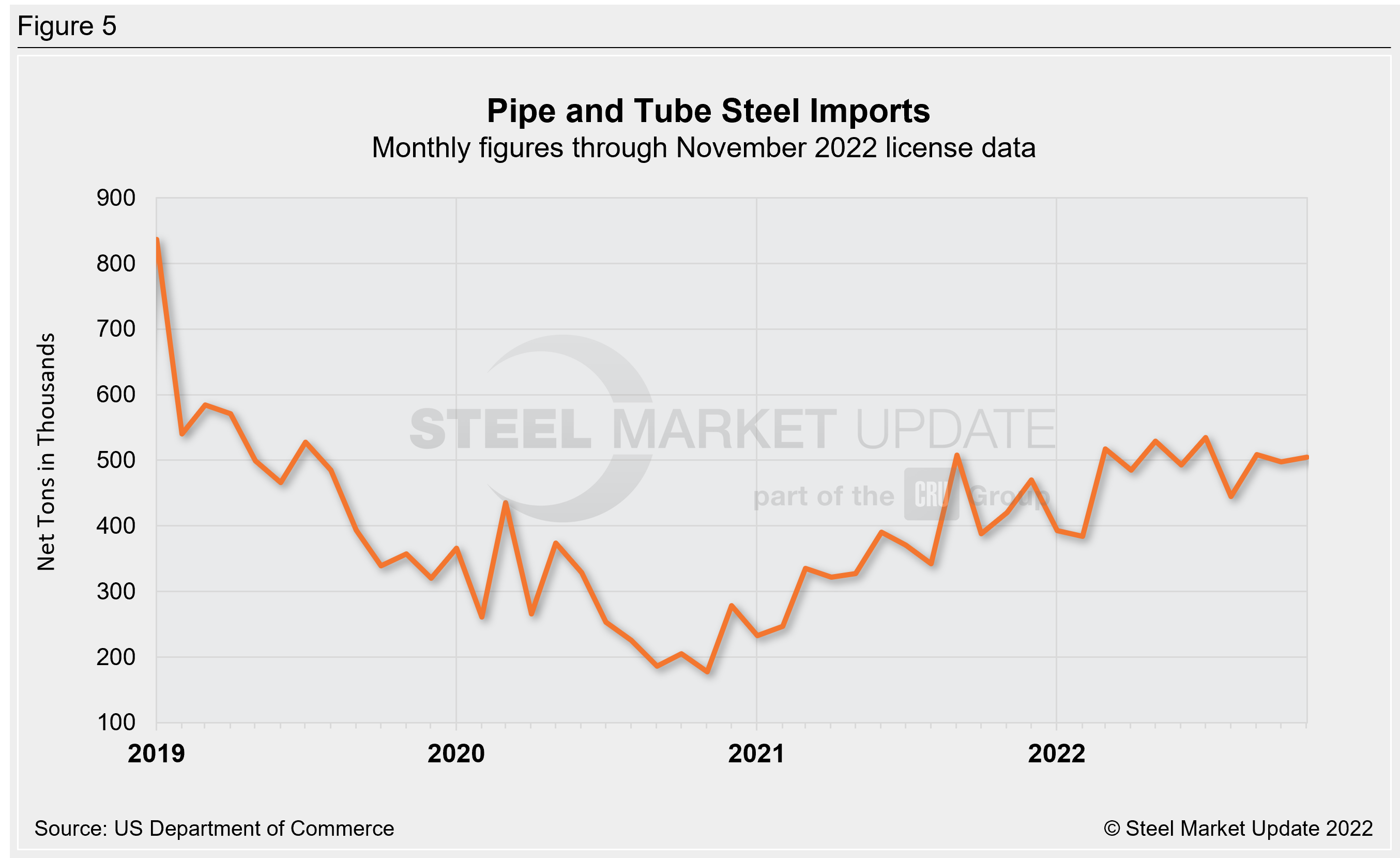

The charts below show monthly imports for two product groups: flat rolled and pipe and tube. Preliminary October flat-rolled imports totaled 909,000 tons, rebounding slightly from September’s 17-month low. November licenses are currently showing 713,000 tons of flat-rolled steel to have entered the country during the month. Pipe and tube imports were 498,000 tons in October, in line with levels seen since March of this year. November pipe and tube licenses are currently at 505,000 tons.

PSA: We have an interactive graphing tool available here on our website, where readers can explore historical import data. If you need assistance logging into or navigating the website, contact us at Info@SteelMarketUpdate.com.

By Brett Linton, Brett@SteelMarketUpdate.com