Prices

August 22, 2023

SMU Price Ranges: Sheet Prices Mixed, Downtrend Moderating?

Written by David Schollaert & Michael Cowden

Sheet prices were mixed this week after trending lower for most of July and earlier in August.

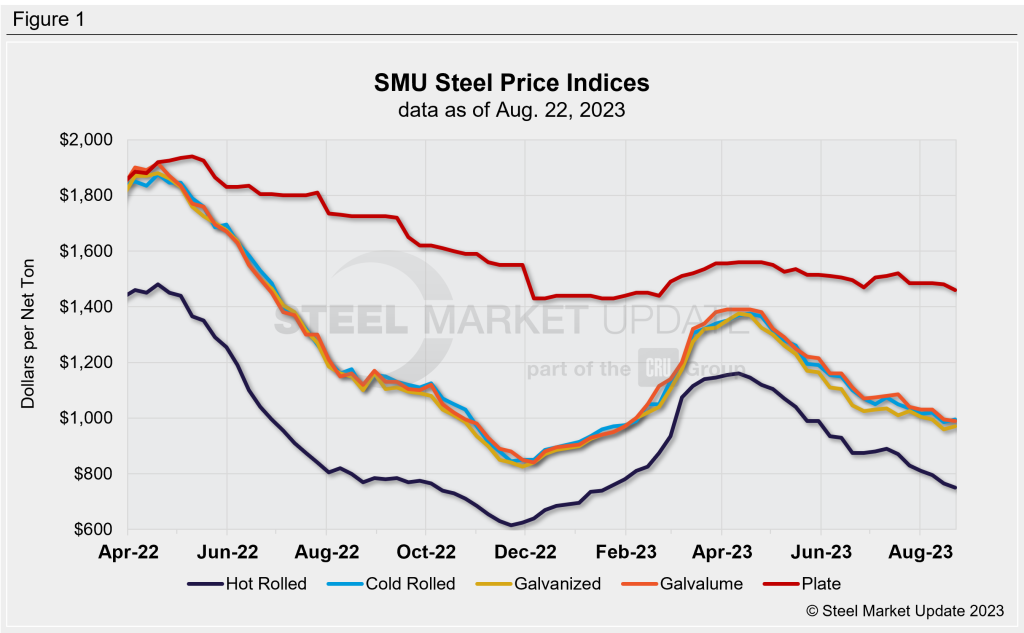

SMU’s average hold-rolled coil (HRC) price slipped to $750 per ton ($37.50 per ton), down $15 per ton from a week ago.

Galvalume prices slipped by $5 per ton. But cold-rolled and galvanized base price, in contrast, rose $10 per ton.

Market sentiment was mixed, with some sources voicing concerns about second-half demand – and uncertainty about United Auto Workers (UAW) negotiations.

Others, however, said seasonality should result in demand picking up as people return to the market in earnest after Labor Day.

SMU has kept all its sheet momentum indicators pointed lower until a clear trend emerges. Our plate momentum indicator remains at neutral.

Hot-Rolled Coil

The SMU price range is $700–800 per net ton ($35.00–40.00 per cwt), with an average of $750 per ton ($37.50 per cwt) FOB mill, east of the Rockies. The bottom end of our range decreased $30 per ton vs. one week ago, while the top end of our range was unchanged week-on-week (WoW). Our overall average is $15 per ton lower compared to the prior week. Our price momentum indicator for hot-rolled coil is still pointing lower, meaning SMU expects prices will decline more over the next 30 days.

Hot-Rolled Lead Times: 3–6 week

Cold-Rolled Coil

The SMU price range is $950–1,040 per net ton ($47.50–52.00 per cwt), with an average of $995 per ton ($49.75 per cwt) FOB mill, east of the Rockies. The lower end of our range was up $30 per ton WoW, while the top end was down $10 per ton compared to a week ago. Our overall average is up $10 per ton WoW. Our price momentum indicator on cold-rolled coil is still pointing lower, meaning SMU expects prices will decline more over the next 30 days.

Cold-Rolled Lead Times: 5–8 weeks

Galvanized Coil

The SMU price range is $920–1,020 per net ton ($46.00–51.00 per cwt), with an average of $970 per ton ($48.50 per cwt) FOB mill, east of the Rockies. The lower end of our range was sideways vs. last week, while the top end of our range was up $20 per ton compared to one week ago. Our overall average is $10 per ton higher vs. the prior week. Our price momentum indicator on galvanized steel is pointing lower, meaning SMU expects prices will decline more over the next 30 days.

Galvanized .060” G90 Benchmark: SMU price range is $1,017–1,117 per ton with an average of $1,067 per ton FOB mill, east of the Rockies.

Galvanized Lead Times: 4-9 weeks

Galvalume Coil

The SMU price range is $950–1,030 per net ton ($47.50–49.50 per cwt), with an average of $990 per ton ($49.50 per cwt) FOB mill, east of the Rockies. The lower end of our range was unchanged vs. last week, while the top end of the range was $10 per ton lower WoW. Our overall average was down $5 per ton compared to one week ago. Our price momentum indicator on Galvalume steel is still pointing lower, meaning SMU expects prices will decline more over the next 30 days.

Galvalume .0142” AZ50, Grade 80 Benchmark: SMU price range is $1,244–1,324 per ton with an average of $1,284 per ton FOB mill, east of the Rockies.

Galvalume Lead Times: 6–8 weeks

Plate

The SMU price range is $1,350–1,570 per net ton ($67.50–78.50 per cwt), with an average of $1,460 per ton ($73.00 per cwt) FOB mill. The lower end of our range was down $40 per ton compared to the week prior, while the top end of our range was unchanged vs. last week. Our overall average is down $20 per ton WoW. Our price momentum indicator on steel plate remains at neutral, meaning we are unsure of what direction prices will go over the next 30 days.

Plate Lead Times: 3–8 weeks

SMU Note: Below is a graphic showing our hot rolled, cold rolled, galvanized, Galvalume, and plate price history. This data is available here on our website with our interactive pricing tool. If you need help navigating the website or need to know your login information, contact us at info@steelmarketupdate.com.

David Schollaert

Read more from David Schollaert