Analysis

July 12, 2024

HVAC equipment shipments rebound 6% in May

Written by Brett Linton

Shipments of heating and cooling equipment bounced back in May, according to the latest data released from the Air-Conditioning, Heating, and Refrigeration Institute (AHRI).

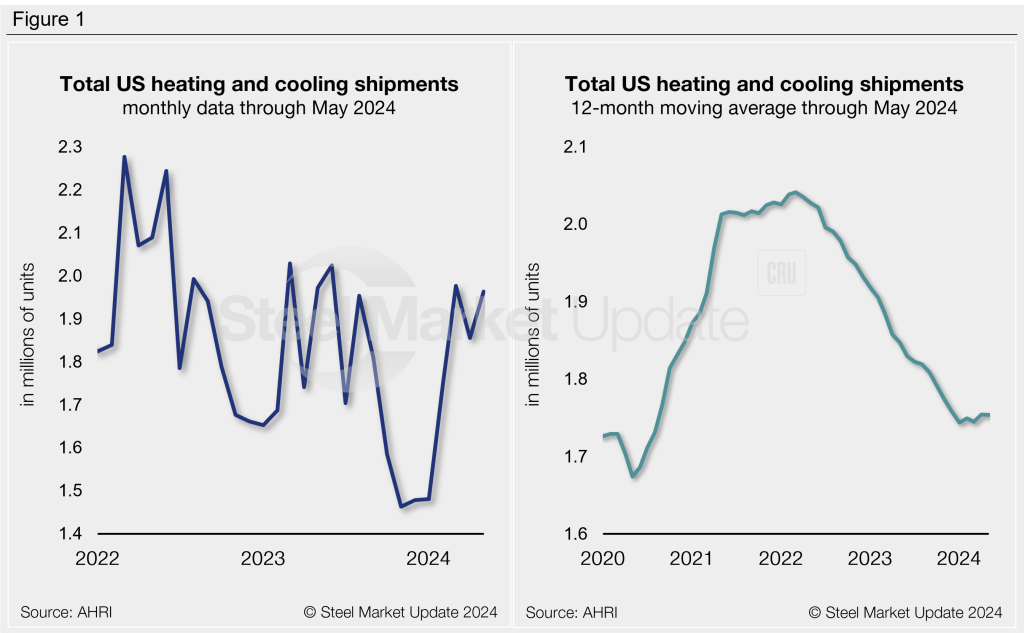

May shipments increased 6% month on month (m/m) to 1.96 million units. This is less than 1% below the same month last year. May represents the second-highest monthly shipment rate recorded in the last 11 months, just below March’s peak of 1.98 million units.

On an annualized 12-month moving average (12MMA) basis, shipments have been trending lower since their post-Covid surge, flattening out in late 2023. The latest 12MMA for total shipments is 1.75 million units through May. This is 5% lower than the same period last year and 14% lower than the 12MMA seen two years prior.

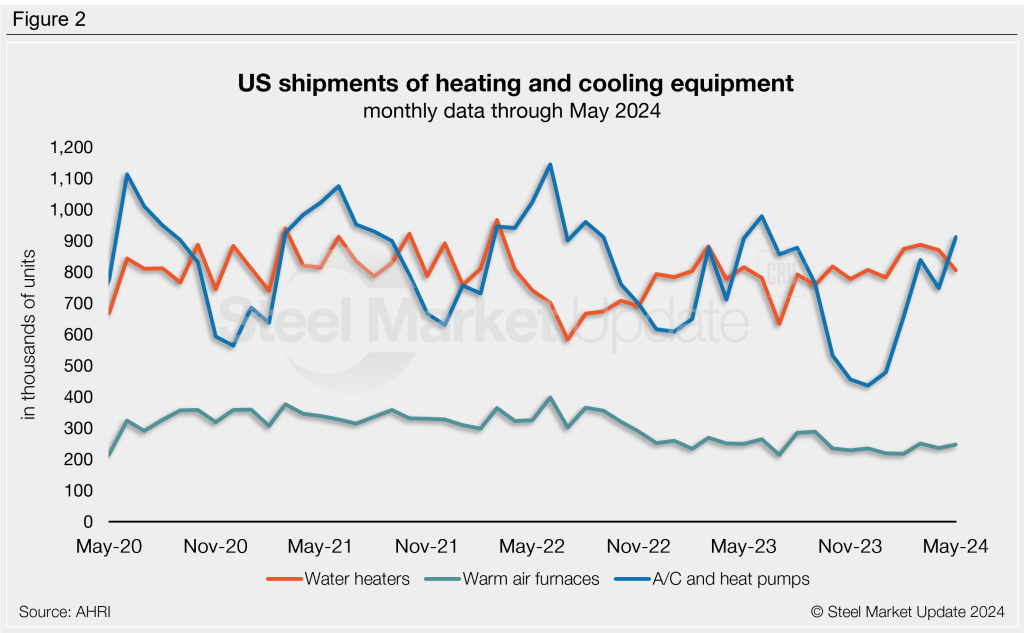

May shipments of residential and commercial storage water heaters eased 7% m/m, now down to a four-month low of 805,000 units. Recall that in March we saw water heater shipments reach a two-year high of 887,000 units. May shipments are 1% less than levels seen one year ago. Combined water-heater shipments have averaged 799,000 units per month across the past year.

Warm air furnace shipments rose 4% m/m to a combined 247,000 units. This is 1% less than levels this time last year. Furnace shipments have averaged 243,000 units per month across the past year.

Shipments of central air conditioners and air-source heat pumps jumped 22% m/m to a total of 912,000 units. Note that air conditioner/heat pump shipments are very seasonal, with slowdowns experienced throughout the winter months as evidence iin Figure 2. Total air conditioner and heat pump shipments are less than 1% higher than the same month one year prior. Shipments have averaged 711,000 units per month across the past year.

The full press release of this data is available here on the AHRI website.

An interactive history of heating and cooling equipment shipment data is available here on our website. If you need assistance logging in to or navigating the website, please contact us at info@steelmarketupdate.com.