Analysis

December 17, 2024

HVAC equipment shipments healthy through October

Written by Brett Linton

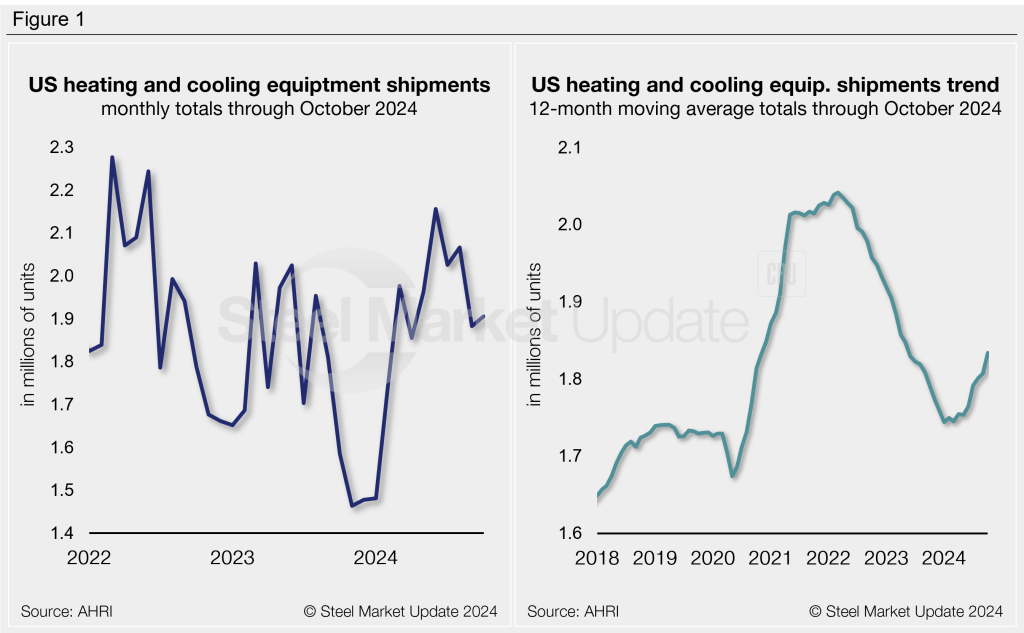

Shipments of heating and cooling equipment were stable from September to October, according to the latest data released from the Air-Conditioning, Heating, and Refrigeration Institute (AHRI).

October shipments ticked up 1% month on month (m/m) to 1.91 million units (Figure 1, left). Recall that shipments recently reached two of the highest levels observed in the past two years in June and August, at 2.16 and 2.07 million units, respectively. October shipments are 20% higher than the same month last year (which was a three-and-a-half year low at the time).

Trends

To smooth out seasonal fluctuations and better showcase trends, monthly shipment data can be adjusted to a 12-month moving average (12MMA) basis. On this annualized basis, shipments have trended higher across 2024. The 12MMA through October has risen to a 17-month high of 1.83 million units (Figure 1, right). This trend reversal comes after the significant decline occurring from mid-2022 to the end of 2023, which followed the post-Covid surge.

Shipments by product

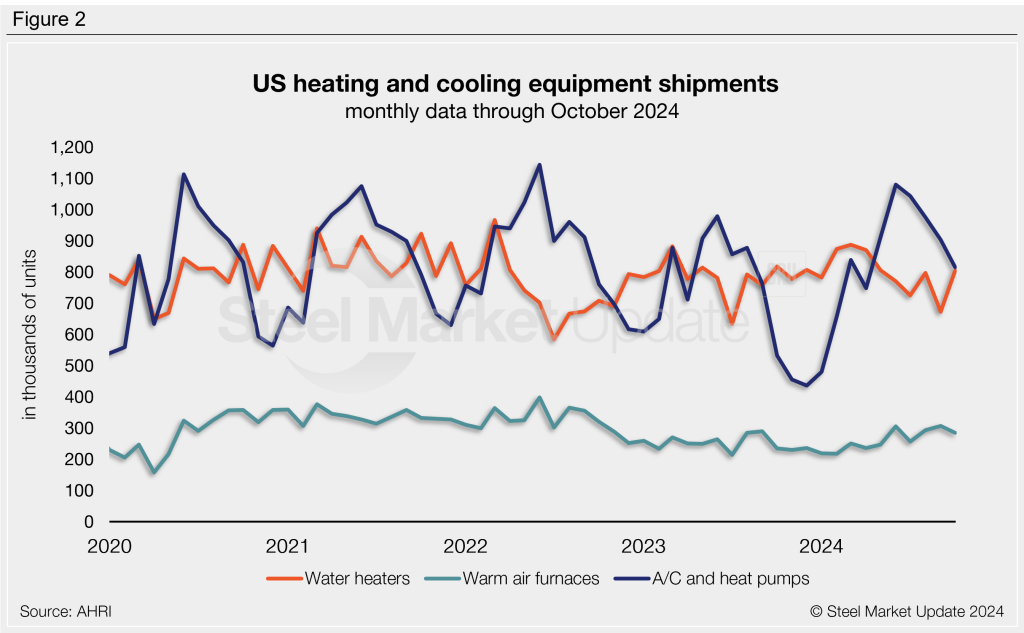

- Water heaters: Shipments rebounded in October to a five-month high of 805,000 units, up 20% m/m from September’s 14-month. Recall the two-year high of 887,000 units recorded back in March. October shipments were 2% less than levels seen one year ago.

- Warm air furnaces: Following September’s 23-month high, furnace shipments slipped 7% in October to 285,000 units. Shipments were 21% higher in October than levels recorded the same month last year.

- Air conditioners and heat pumps: Shipments fell in October for the fourth consecutive month, easing 10% m/m to 815,000 units. While down, total shipments were 53% greater than the same month one year prior. Note that air conditioner/heat pump shipments are very seasonal, with slowdowns experienced throughout the winter months as evident in Figure 2.

The full press release of this data is available here on the AHRI website.

You can also dig deeper into SMU’s interactive history of heating and cooling equipment shipment data.