Analysis

January 14, 2025

Final Thoughts

Written by Michael Cowden

It’s another week of big headlines and ho-hum pricing moves – which is to say the start of 2025 is looking a lot like the end of 2024.

Scrap has settled up $20 per gross ton (gt). Steel prices, however, were a soft sideways this week.

Chalk it up to uneven demand and abundant supply. And while we’re not aware of any major outages, some of you tell us that you’ve lost some shipping days here and there because of the cold snap.

A quiet start to the year for prices

“Things are quiet,” one Midwest service center source said. “We all bought big in Nov.-Dec. All those deliveries are being made now – and on time, which tells you that the mills are not all that busy.”

“This week isn’t bustling, so not much in the way of transactions to report. While there’s much in the news for tariffs … buyers are not showing much urgency,” another industry source said.

Nucor, for example, is officially at $750 per short ton (st) for hot-rolled (HR) coil – where it’s been since Nov. 12. Prevailing spot prices might be lower than that. But the lack of movement generally reflects spot market trends.

Another indication of a market off to a slow start: Some sources reported getting unsolicited offers from mills at competitive prices. Some even predicted that prices in the mid/low $600s for HR, roughly where contract prices are now, could bleed into the spot market unless demand improves or supplies are further restricted.

And yet market participants were generally optimistic about 2025 – predicting that Q2 should be better than Q1 and that Q3 should be better than Q2. In other words, if 2024 was a year of prices surprising to the downside, there is a hope that 2025 could see the opposite – prices surprising to the upside.

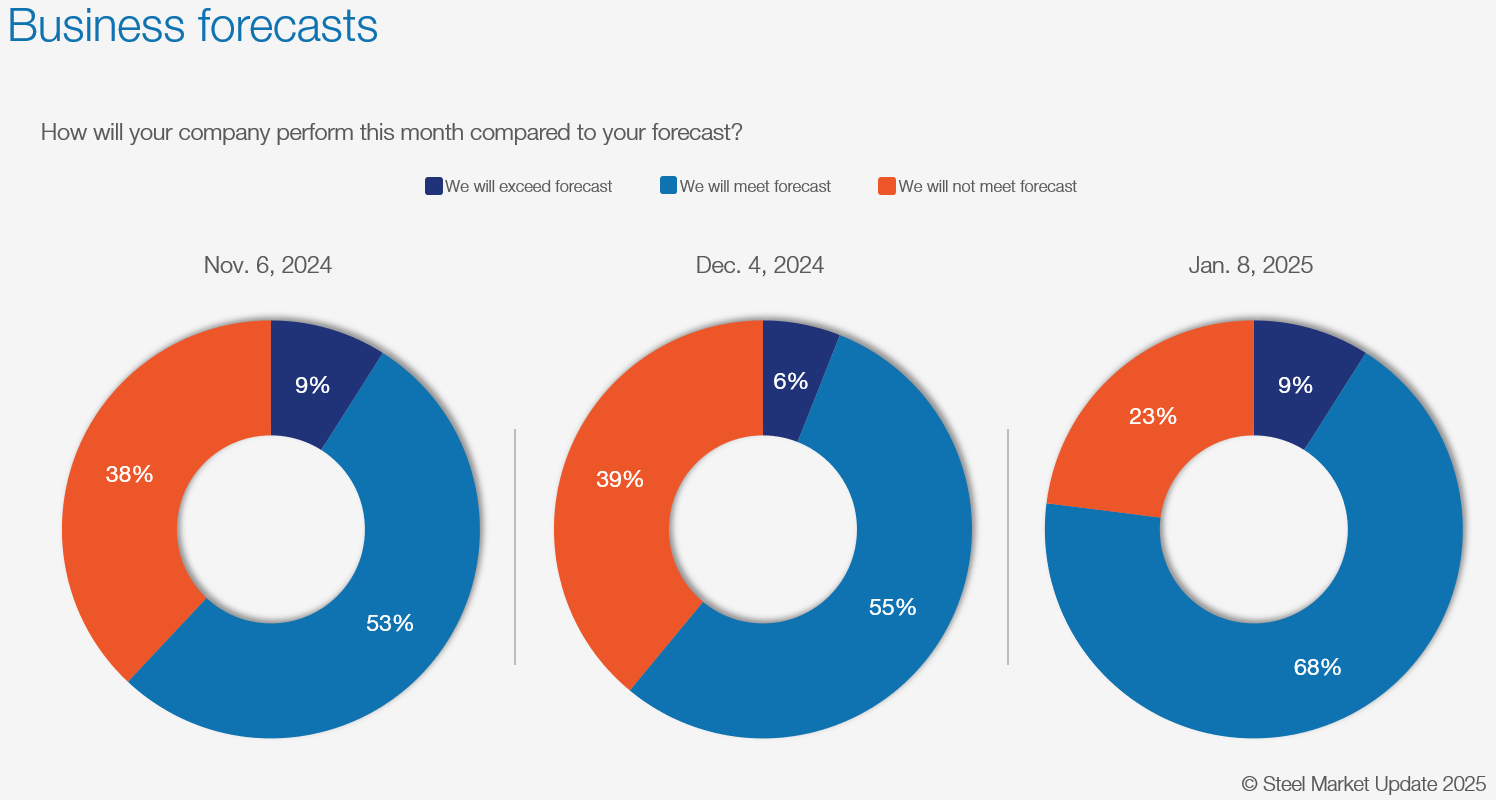

In fact, despite the slow start to the year, most respondents to our last survey said they would meet or exceed forecast. Only 23% said they would miss it – which is a big improvement from prior months, when nearly 40% said they would miss forecast.

The Cliffs-Nippon-USS circus continues

As far as headlines go, Cleveland-Cliffs Chairman, President, and CEO Lourenco Goncalves stole the show this week, for better or worse.

He did it with a press conference at the company’s Butler Works in Western Pennsylvania. The event was promoted to media outlets as a celebration of the the company’s acquisition of AK Steel five years ago. The invite also mentioned that Butler makes electrical steel.

I thought the presser might be focused on trade issues. Maybe Goncalves would call for more protections from the incoming administration – particularly for electrical steels. That’s not quite how it went down.

SMU reporter Stephanie Ritenbaugh has the highlights (and lowlights) here. The main point: Cliffs remains adamant that it wants to buy U.S. Steel.

You could be forgiven if you got distracted from that point. I know what’s considered acceptable public discourse has changed over the last year. Still, it’s a bit of a stretch to suggest that Japan is “worse” than “evil” China. And that nothing has changed since 1945. As if all that weren’t enough, Goncalves threatened to come for Nippon Steel CEO Eji Hashimoto’s dog.

With Goncalves speaking about “America first” (and pets) in front of a row of US flags, consensus seems to be that his words were intended for the incoming Trump administration. What’s the goal there – to get a US president to intervene (again) in the USS-Nippon process? And could Trump change deadlines as abruptly as Biden has? We’ll see soon enough.

Fire up the rumor machine

Goncalves’ remarks also came amid reports, among credible media outlets, that Cliffs and Nucor might work together to acquire U.S. Steel.

Maybe. There is some logic to that.

Cliffs would get its wall of integrated mills along the Great Lakes. Nucor would finally get Big River Steel (BRS) – the startup that it tried to block more than a decade ago and that is now a massive EAF complex. BRS also happens to be nestled along the Mississippi River, right next door to other Nucor mills in northeast Arkansas. So there are clear synergies for both companies.

That said, credible media outlets also reported, back in 2023, that Esmark was in the running to buy U.S. Steel. That didn’t age well. So, again, we’ll see what happens this time around.

Trade and tariffs

By the way, we’re less than a week away from Inauguration Day. And there is still little consensus on what new tariff regime we might be facing. Was the threat of tariffs enough? Or is the real thing still necessary?

Also, there are questions over whether projects funded by the IRA and other Biden-era initiatives will remain on the books or face cuts. That’s something I’m curious to find out about too.

And if you’re tired of speculation and looking for answers on trade issues, Laura Miller has a good update on the coated trade case here. Long story short, the prelims are likely to be moved to April 3 – as has been rumored for some time now. The market consensus: Expect shipments to continue to arrive through March but to fall sharply thereafter.

Tampa Steel Conference

One thing that’s not off to a slow start is the Tampa Steel Conference! As temperatures have dropped, registrations have picked up.

Nearly 450 people have registered to attend, which puts us on track to meet or exceed last year’s record. You can see the list of companies attending here.

There will be a lot to talk about, especially as Trump 2.0 trade policies come more into focus. And, of course, there will be networking opportunities too. Do you prefer golf or a harbor tour? You can find out more and register here.