Sheet

April 9, 2025

SMU Steel Demand Index momentum slows further

Written by David Schollaert

SMU’s Steel Demand Index growth eased again, according to early April indicators. The slowdown comes after the index reached a four-year high in late February.

Despite moderate declines over the past month, the index remains in expansion territory.

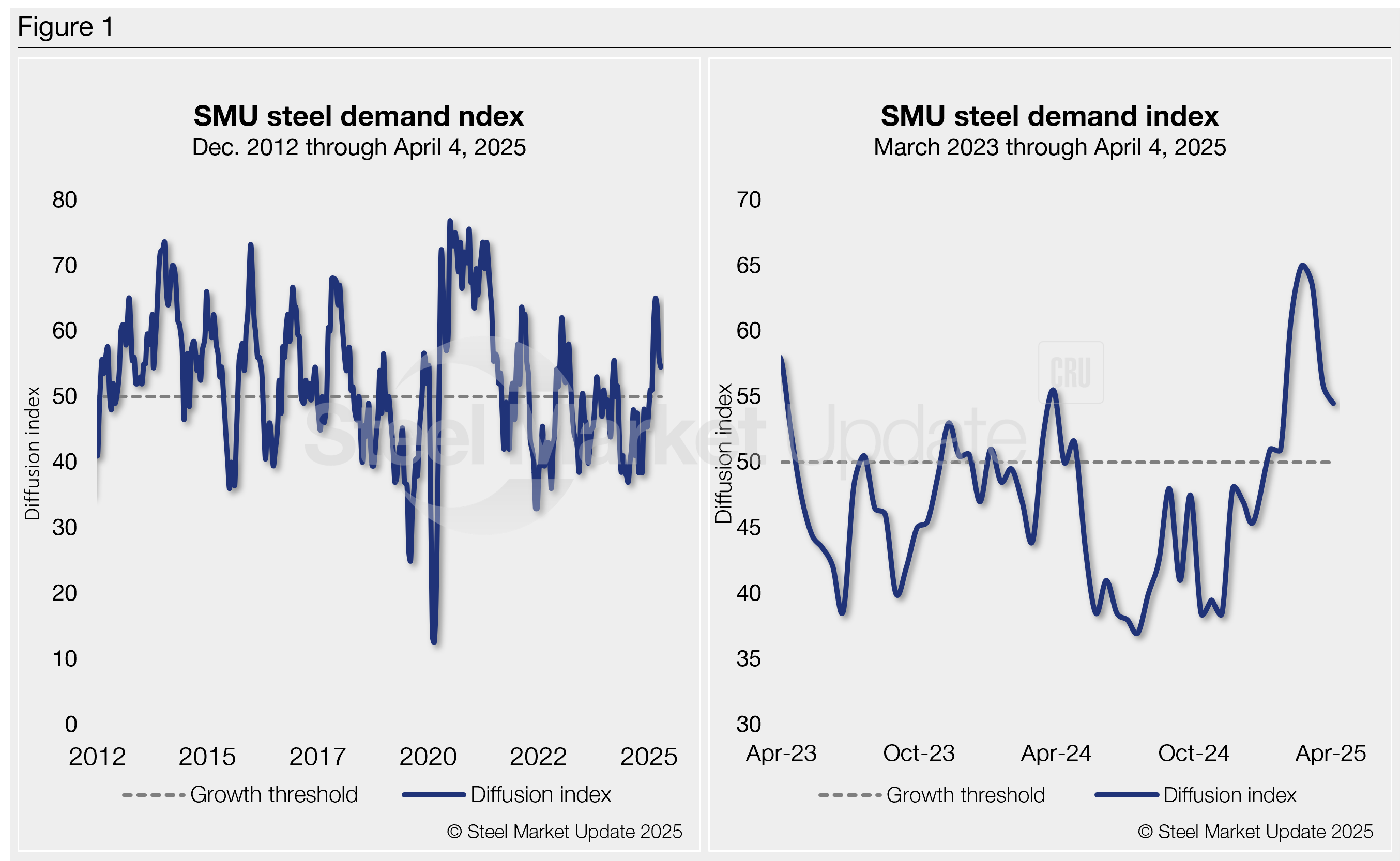

The Steel Demand Index, compiled from our twice-monthly survey data, now stands at 54.5, down from 65.0 in mid-to-late March, and off from a four-year high of 65.0 in late February.

Momentum turned at the start of the year. In February, mills began pushing higher prices, supported by tariffs. Once buyers covered near-term needs, concerns shifted to uncertainty around some of those same tariffs. Buying tailed off, demand has pulled back, and so have prices.

Methodology

Derived from the market surveys SMU conducts every two weeks, the index compares lead times and demand to create a diffusion index. This index has historically preceded lead times, which is notable given that lead times are often seen as a leading indicator of steel price moves. An index score above 50 indicates rising demand and a score below 50 suggests declining demand.

Figure 1 shows the nearly 13-year history of the index on the left and provides a closer look at the Steel Demand Index readings of the past two years on the right.

Some background

Last year was marked mostly by a slow-but-steady grind lower in demand. Spot buying struggled, and prices in the flat-rolled market waned. It turned the index into contraction for the better part of 2024. Trend shifts came only on the backs of some short-lived impetus from mill price hikes.

But the index revealed there wasn’t much underlying demand for steady growth. Large-volume buyers capitalized on discounted steel, but weak end-market demand prevailed.

The Trump bump

Optimism was noticeably up. The arrival of a new administration and the potential of a revamped Section 232 awakened demand in late 2024, especially in Q1’25. Mills were unified in their pricing stance, and buyers were keen to get in ahead of the increases. Contract and spot buys were pulled forward, mills nearly stopped negotiating, and lead times moved out.

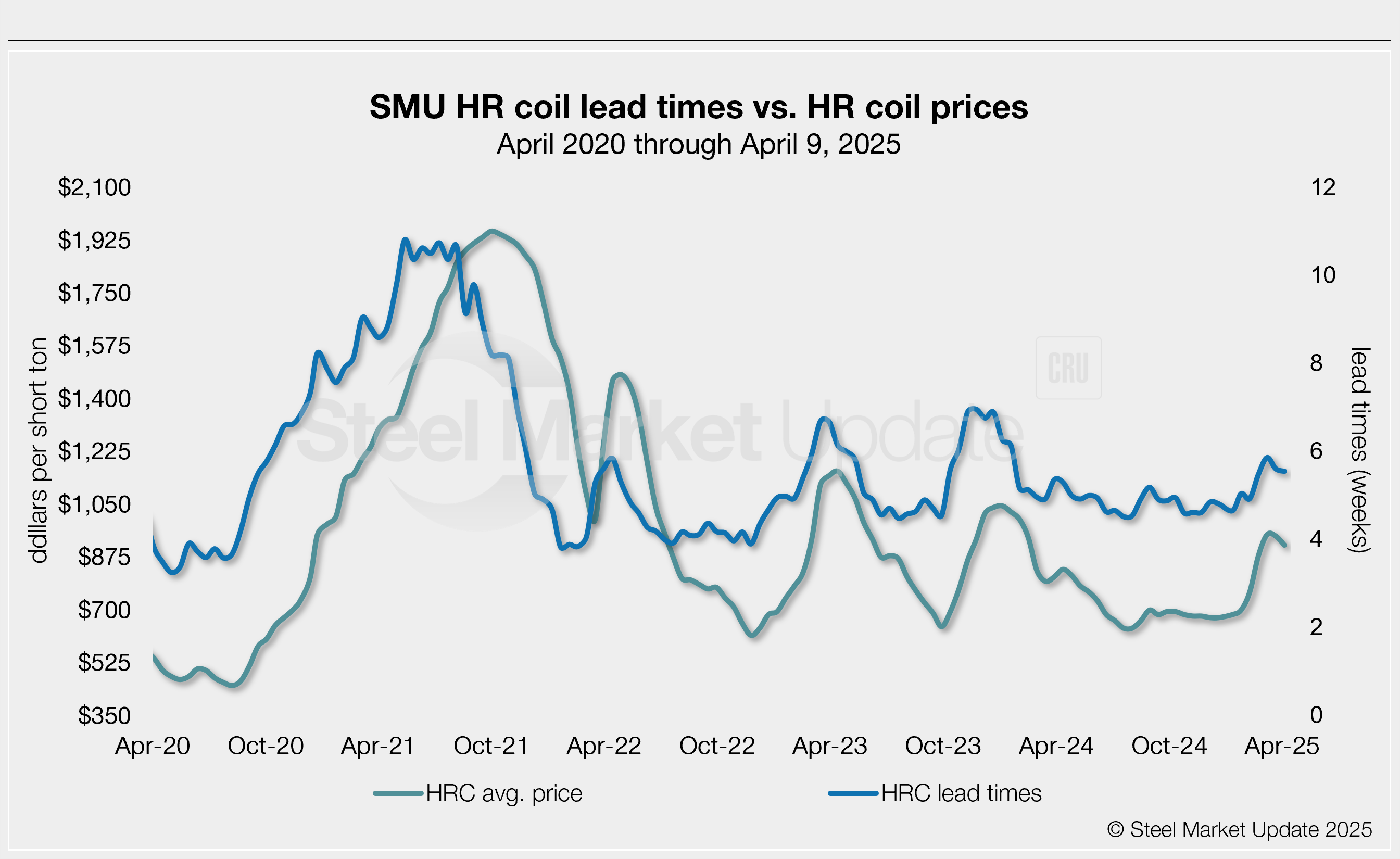

And hot-rolled (HR) coil prices responded, rising by nearly $300 per short ton (st) in just about nine weeks. And Lead times, which had been slipping and nearing 4.5 weeks, stretched out to nearly 6 weeks in early March.

But growing uncertainty on how it will all play out has shown a trend of declines.

HR coil prices have seen a similar trend, reaching $950 per short ton (st) in early March, but have since ticked down on average to $905/st, according to SMU’s latest check of the market on Tuesday, April 8.

Lead times are now back to 5.5 weeks on average in our latest assessment on April 2, down from 5.9 weeks on average just a month ago.

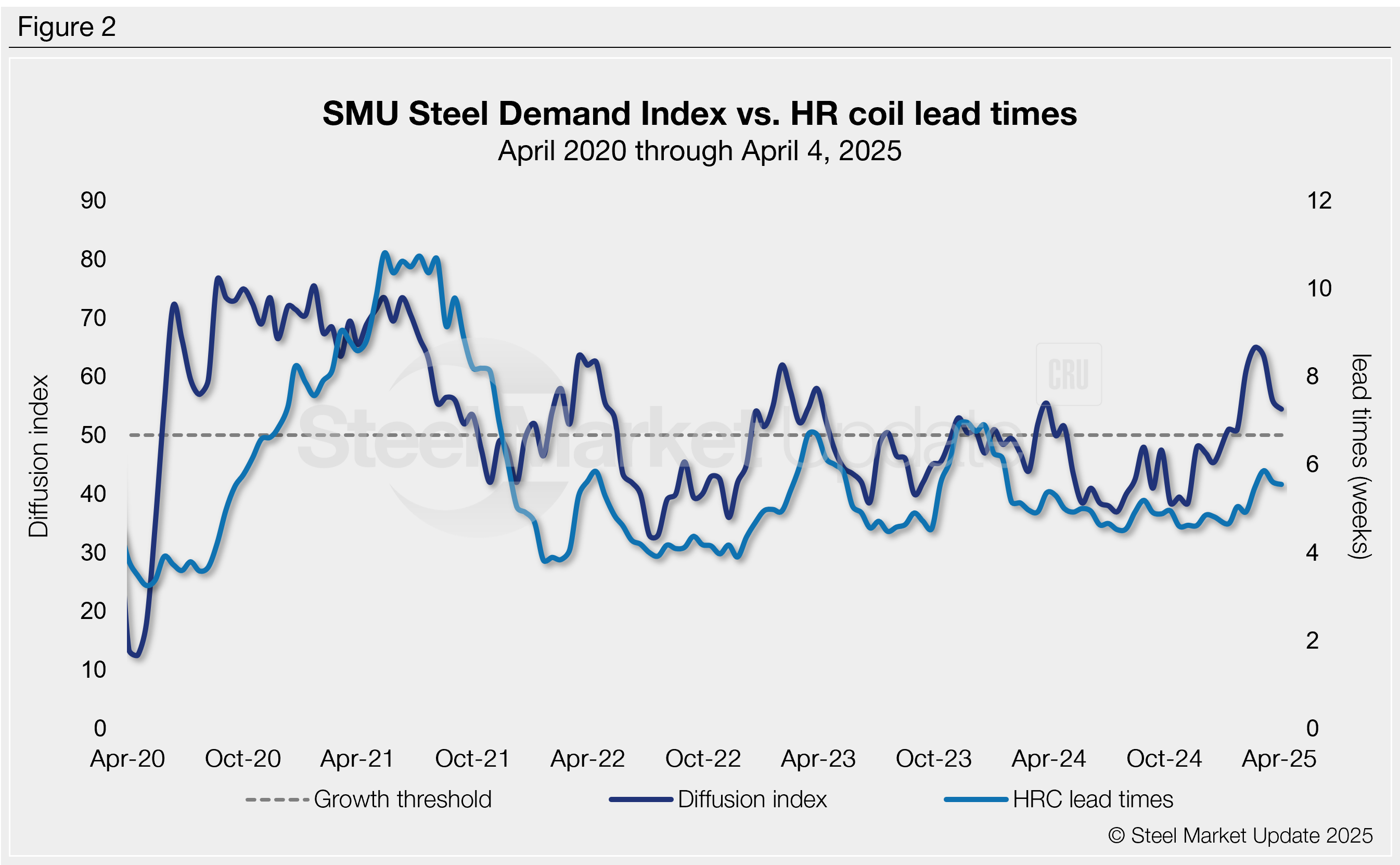

For nearly a decade, SMU’s steel demand diffusion index has preceded moves in mill lead times (Figure 2), and SMU’s lead times have also been a leading indicator of flat-rolled steel prices, particularly for HRC (Figure 3).

What to watch for

While demand in some sectors remains steady and is still showing growth, the recent tariff-driven buying surge has turned.

Uncertainty slowed things down, and now the market seems a bit paralyzed since “Liberation Day.” Buying has slowed, though underlying demand for plate seems to be running a bit better for now, according to market sources.

But aside from the unknown of the latest political landscape shift, could some of the perceived curtailment in buying be a result of lead times now stretching into the slow summer months?

Recent survey data suggest very few believe the market will have legs come summer.

Time will tell if the uncertainty around tariffs has led to the apparent shift in buying, or if it’s driven largely by balanced inventories as we move closer toward traditionally slower summer months.

Maybe it’s a blend of both. Nevertheless, we’ll know soon enough.

Editor’s note

Demand, lead times, and prices are based on the average data from manufacturers and steel service centers participating in SMU’s market trends analysis surveys. Our demand and lead times do not predict prices but are leading indicators of overall market dynamics and potential pricing dynamics. Look to your mill rep for actual lead times and prices.