CRU

April 17, 2025

CRU: Iron ore falls to a 7-month low on escalating trade war

Written by Erik Hedborg

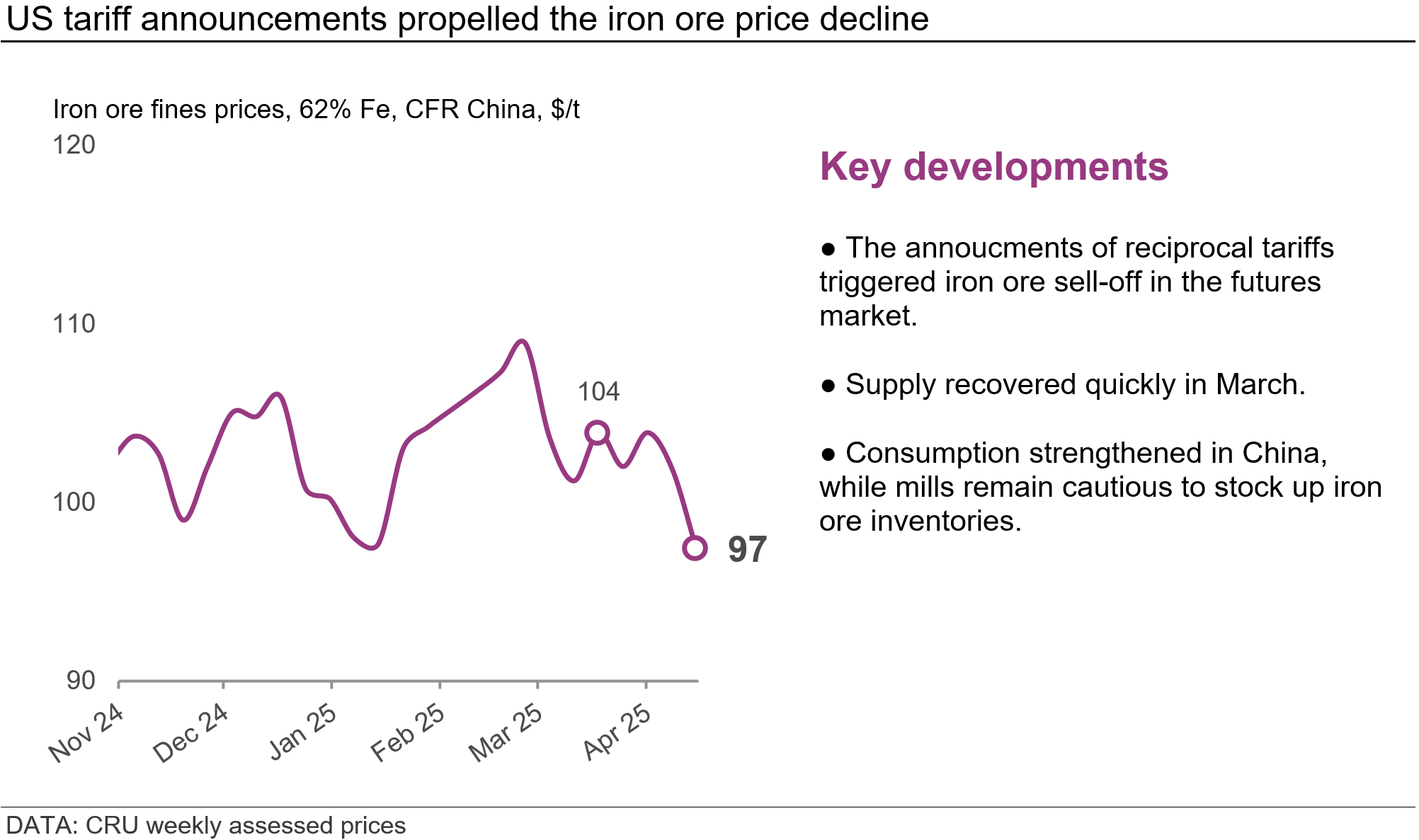

Iron ore prices were largely steady in March, hovering around $100–102 per dry metric ton (dmt) in a quiet market.

However, prices declined sharply in early-April, as President Donald Trump’s tariffs announcement triggered significant selloff of steel and iron ore futures. While prices slightly edged back up over the past week, our monthly assessment fell to $97/dmt as a result.

US tariff situation evolved rapidly

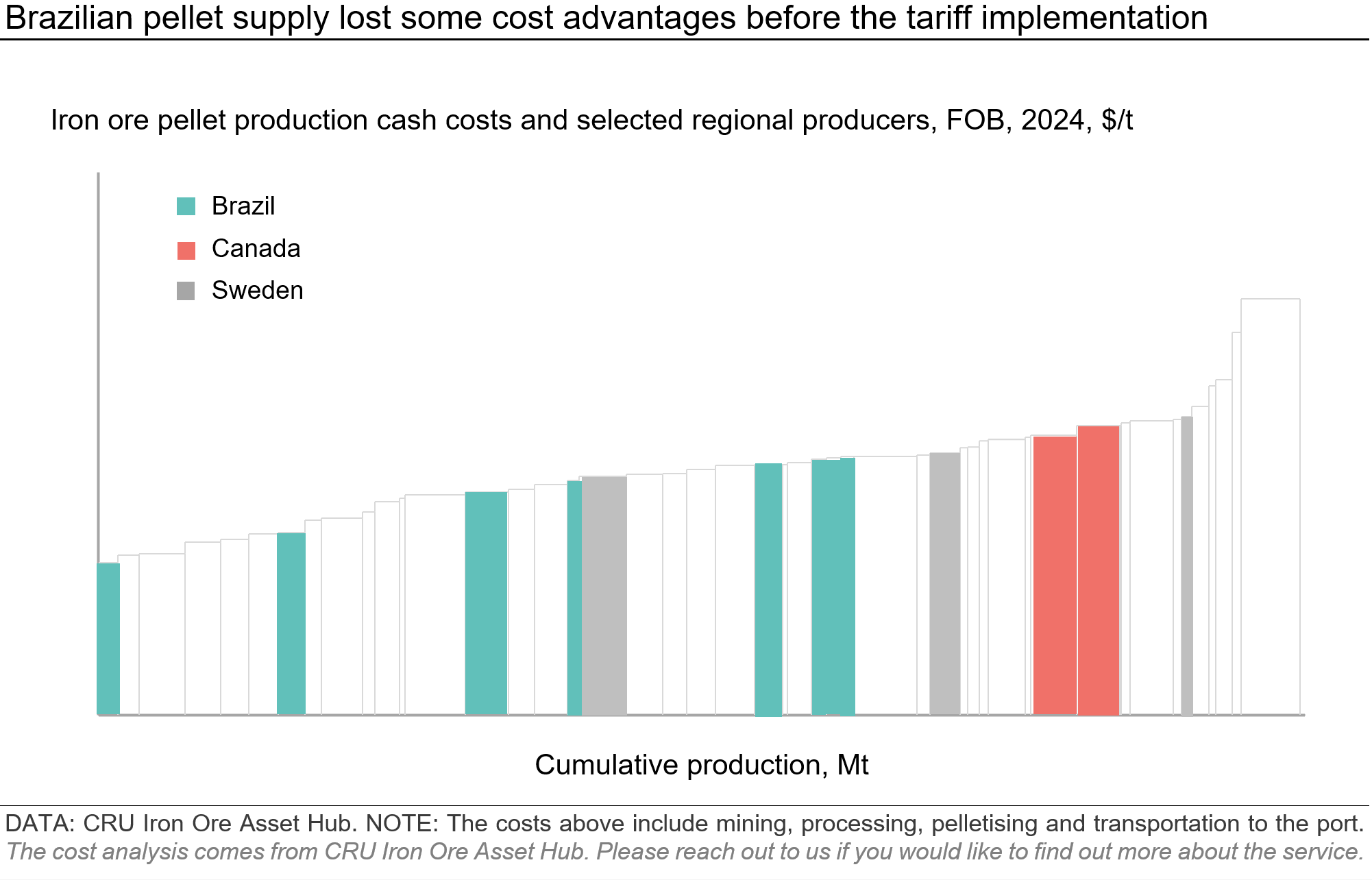

As discussed in a prior Insight, the US is a net importer of iron ore, mainly DR pellet. In 2024, ~57% of pellet imports came from Brazil, ~40% from Canada, and ~3% from Sweden.

With the announcement of retaliatory tariffs, CRU learned that for iron ore imports into the US, Brazil and Sweden will face a 10% import tariff, while Canadian pellet will no longer be taxed as it is USMCA-compliant.

Looking at major pellet exporters to the US, Brazilian producers have been on the lower side of the cost curve. With higher freight costs and the 10% duty, some higher-cost Brazilian supply may become less competitive comparing to Canadian supply.

However, CRU believes quality consideration is at the top of the list for US pellet buyers, and Brazilian pellet from Vale and Samarco will still be favored even with the import duty.

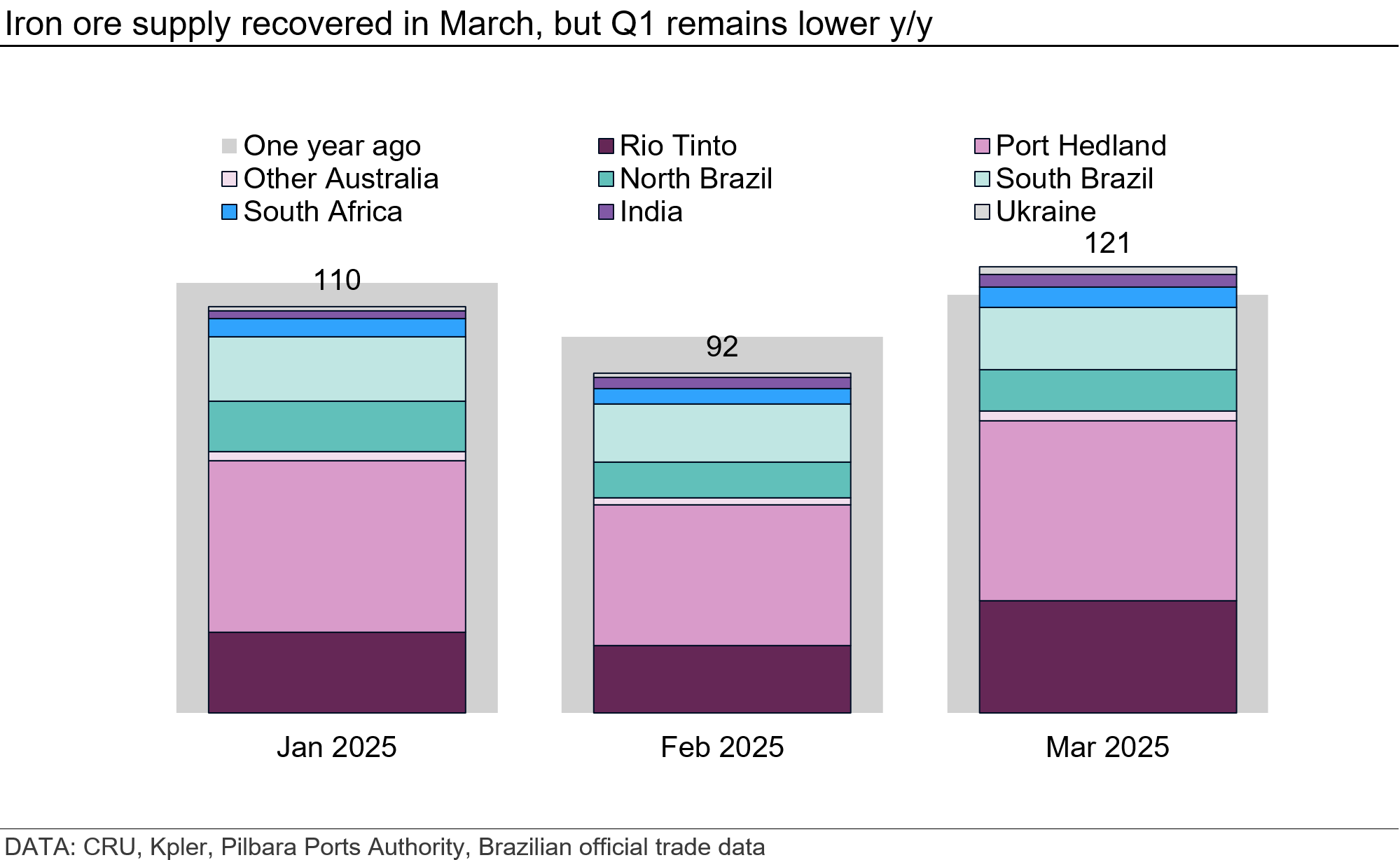

Supply received a strong push in March

Australian shipments recovered and excelled quickly since late-February and stayed at a robust level throughout March.

Producers looked to increase supply to catch up with the schedule as severe cyclone disruptions in January and February led shipments to fall behind. Port Hedland shipments totalled 50.7 million metric tons (mt) in March, the strongest March month on record.

Rio Tinto also ramped up to a record-high March level of 30.3 million mt. Despite the end of quarter efforts of 4.4 million mt year-over-year (y/y) increase in Australian March shipments, Q1 shipments were still 2.2 million mt lower y/y. Shipments slowed at the beginning of April, and it appears that Roy Hill deferred its maintenance.

For Brazil, March exports rose to 28.4 million mt as rainfall began to subside and miners sold more of their stocks during the quarter. For Vale, we saw increased outflow from the north, especially from S11D. Pellet exports also increased as Samarco offloaded more of its pellet inventory in March. Shipment data suggests that this momentum continues into April, especially as freight will be under more pressure going forward.

Canadian exports to the US dropped significantly in March due to the initial imposition of a 25% blanket tariff that was later pushed back. Total exports rose on increased shipments to France, Belgium, Japan, and South Korea. While the latest development suggests there is no tariff on Canadian iron ore, erratic changes to US tariff policies remain a business risk for Canadian pellet producers selling to the US.

Chinese consumption somewhat surprised to the upside

Over the past month, Chinese iron ore consumption is estimated to rise by ~4.6 million mt, or ~3.9%, month over month (m/m) with higher hot metal production. This is an impressive number that exceeded our previous expectation. This is mainly because of strong manufacturing steel demand and steel export constraints having yet to fully take effect. Iron ore port inventories have fallen at a slower pace following the substantial decline in the previous month due to cyclone-led supply disruptions in Australia and are now at 143–144 million mt.

Steelmakers remain cautious about whether robust steel demand is sustainable. On one hand, direct steel exports are under greater pressure, as fresh safeguard measures have taken effect in countries such as Vietnam and South Korea, while the Chinese government tightened taxation regulations that would crack down upon illegal steel exports.

On the other hand, indirect steel exports through manufacturing goods are at risk of higher tariffs in the US market. Moreover, even though steel margins were positive, they were not high enough to motivate mills to buy and hold additional iron ore inventories aside from the volumes that are just sufficient to maintain their BF operations. The surveyed iron ore mill inventories have been higher than last two years over the past few weeks but remain below that prior to 2023.

This article was first published by CRU. To learn about CRU’s global commodities research and analysis services, visit www.crugroup.com.