Analysis

September 12, 2025

Drill rig activity ticks higher in US and Canada

Written by Brett Linton

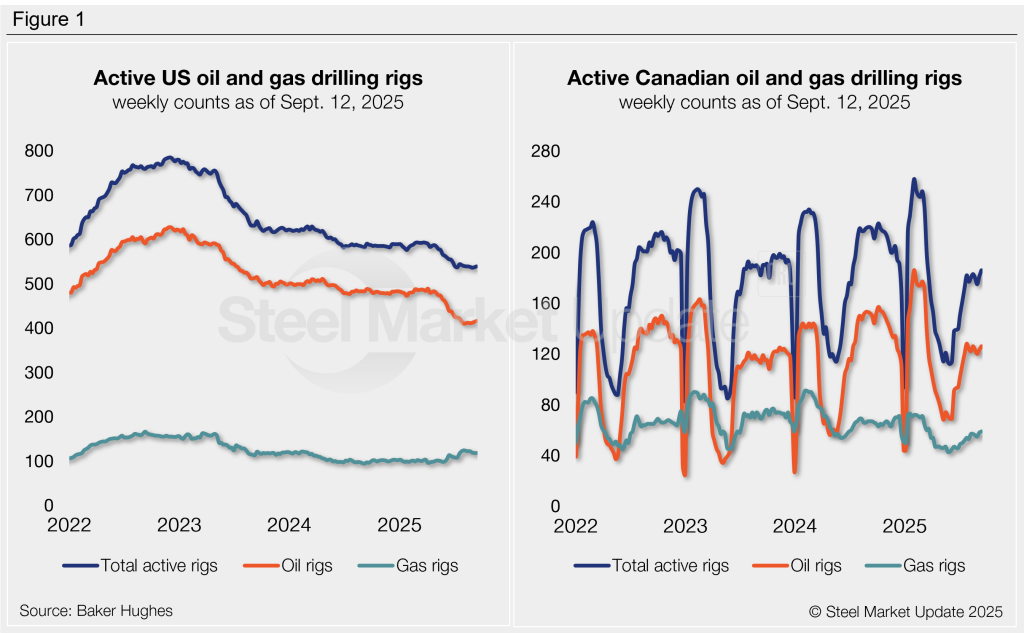

Active rig counts increased in both the US and Canada last week, according to figures released by Baker Hughes. Although rising, US counts continue to hover just above historic lows. Canadian figures remain comparatively healthy, rising to a six-month high this week.

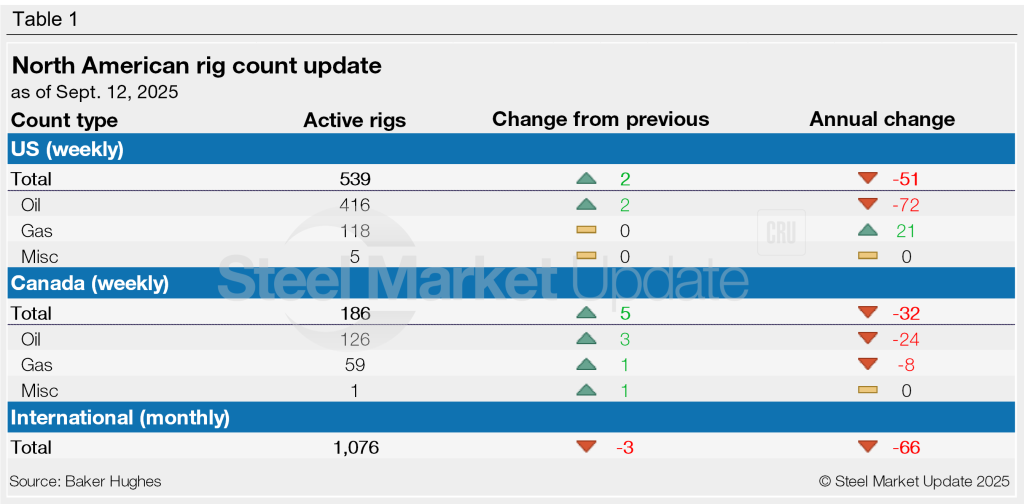

Total US rig counts climbed by two week over week (w/w) to 539. This is only three rigs above the near-four-year low seen two weeks prior. There are 51 fewer US rigs in operation this week compared to this time last year.

Canadian activity increased for the third consecutive week, rising by five rigs w/w to 186. Despite recent increases, Canadian counts are down 32 rigs compared to those seen one year prior.

The monthly international rig count declined by three rigs in August to 1,076, 66 fewer than levels seen one year ago.

The Baker Hughes rig count is significant for the steel industry because it is a leading indicator of oil country tubular goods (OCTG) demand, a key end market for steel sheet.

For a history of the US and Canadian rig counts, visit the rig count page on our website.