Manufacturers/End Users

September 25, 2025

AIA: Architecture firms still under pressure

Written by Brett Linton

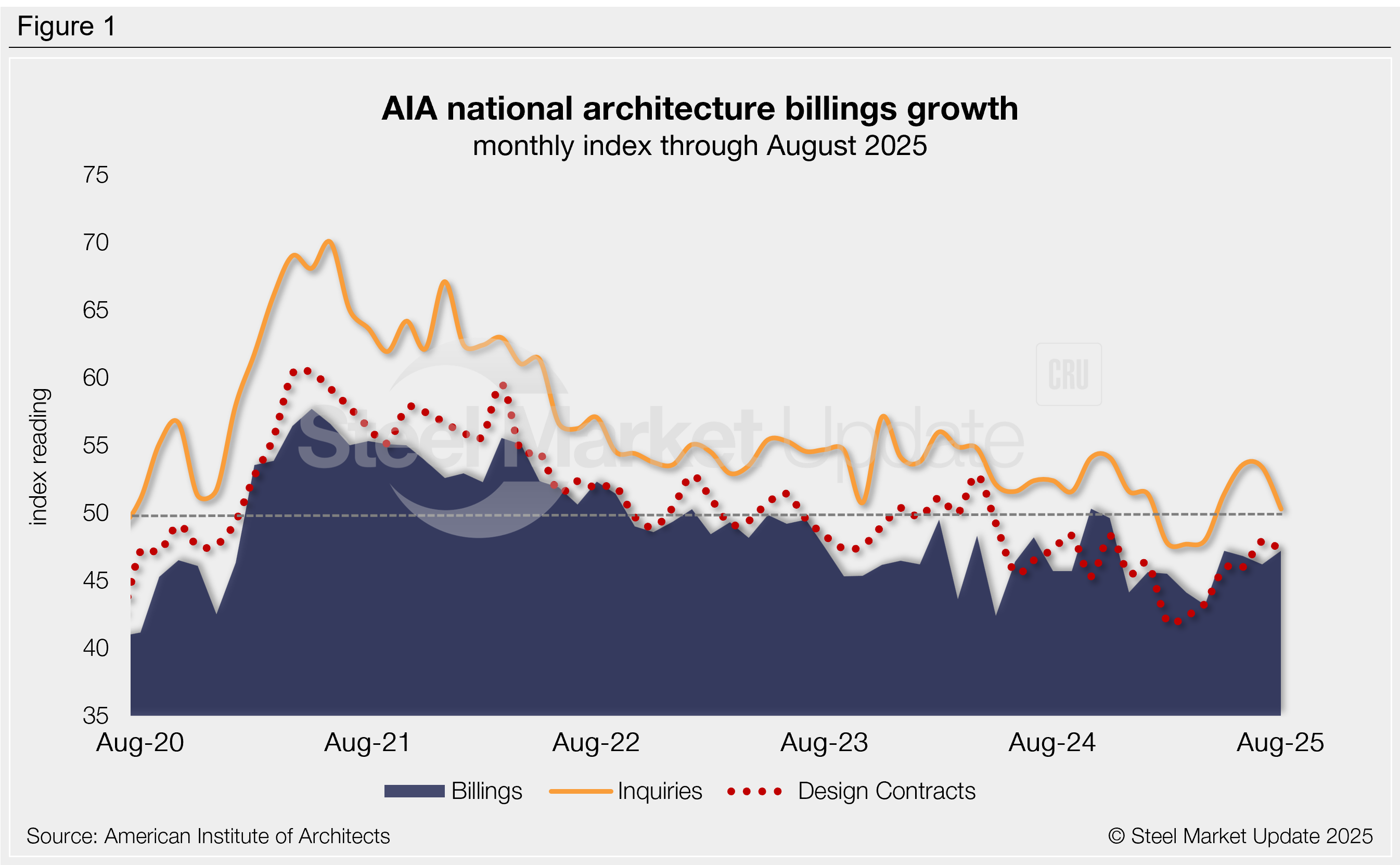

Architecture firms reported a modest improvement in billings through August, yet business conditions remained soft, according to the latest Architecture Billings Index (ABI) release from the American Institute of Architects (AIA) and Deltek.

The August ABI ticked up one point from July to 47.2, matching May for the strongest reading seen since November (Figure 1). The ABI has been in contraction for all but two months since October 2022, indicating consistently weakening business conditions since the post-pandemic rally.

“While business conditions remained soft at architecture firms nationally, there are signs that the downturn may be bottoming out,” said AIA chief economist Kermit Baker. He noted that new project inquiries have risen for four consecutive months, and billings at multifamily and commercial/industrial firms are showing signs of stability.

The ABI is a leading indicator of nonresidential construction activity, projecting business conditions approximately 9-12 months in the future (the typical lag between architecture billings and construction spending). Readings above 50 indicate an increase in architecture billings, while those below indicate a decline.

Participant comments this month included:

- “Proposal activity has increased but contract signatures are weak. Still far too much uncertainty for investors to pull the trigger on larger projects.” – Western firm with commercial/industrial specialization

- “RFPs and RFQs have substantially decreased in amount. Project sizes are generally smaller in nature. Firms that would not have historically pursued small-scale work are pursuing those projects now.” – Midwestern firm with institutional specialization

- “Our firm has seen a significant increase in multifamily projects, starting with a great emphasis on getting projects shovel-ready to start construction.” – Southern firm with residential specialization

- “Slow but appear to be increasing opportunities in fall 2025 into 2026.” – Northeast firm with institutional specialization

Subindex trends

The new project inquiries index slipped to a four-month low of 50.3 in August, though it continues to indicate growth. The design contracts index remained in contraction for the 15th straight month at 47.2, though it is holding above the lows seen earlier this year.

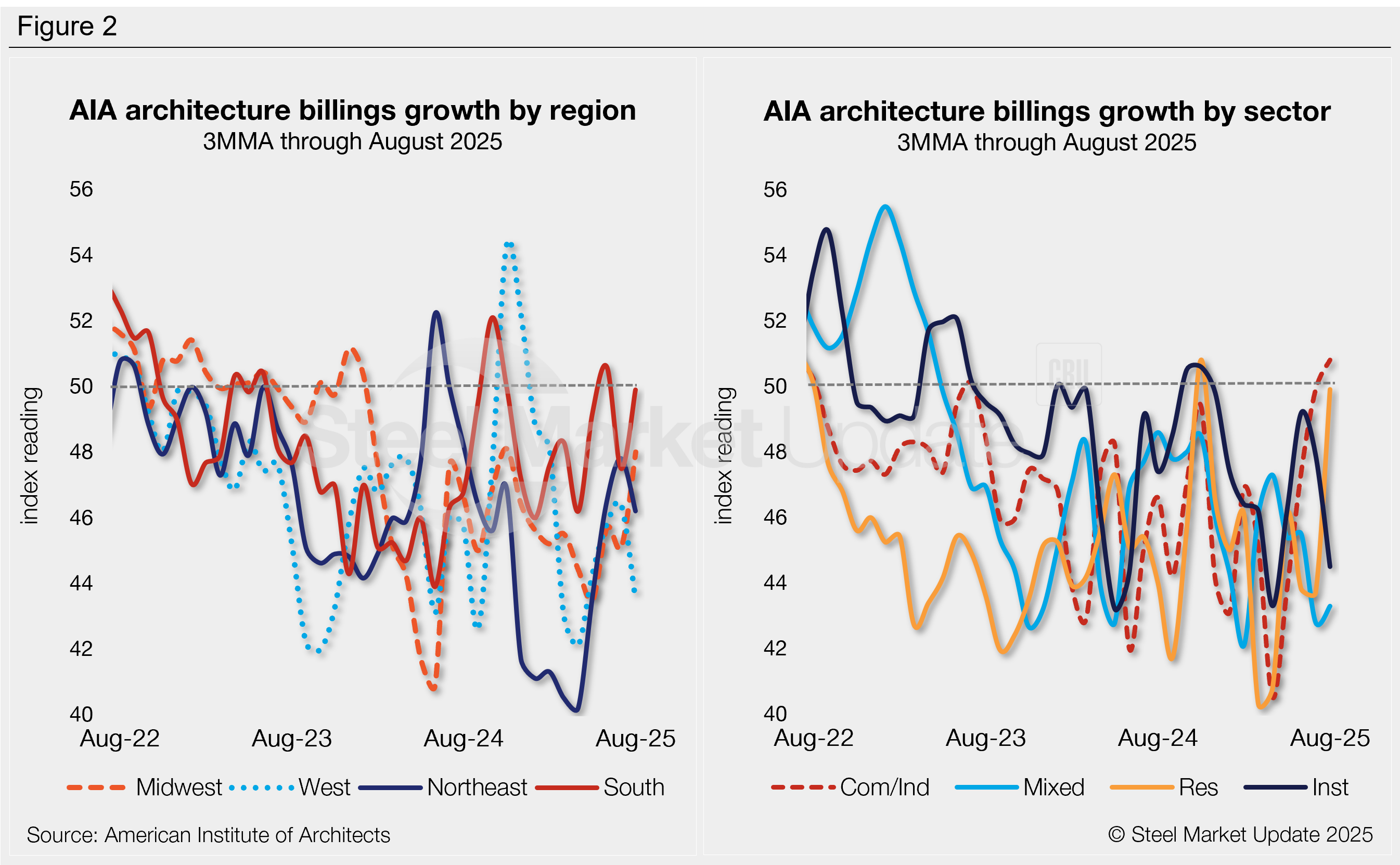

Two of the four regional indices (Southern and Midwest) ticked higher from July to August, though all stayed below the 50 threshold (Figure 2, left). The Southern region nearly returned to growth territory, rising to 49.9.

Three of the sub-sector indices recovered from July (all but institutional). Residential saw the sharpest gain, jumping more than six points to a nine-month high. Commercial/industrial was the only sector to record an actual increase in billings, rising to 50.8 (Figure 2, right). Recall that in March the residential, commercial/industrial, and institutional sectors were at some of the lowest levels witnessed across the past five years.

An interactive history of the August Architecture Billings Index is available here on our website.