Analysis

November 25, 2025

SMU Survey: Mills firmer on sheet prices, more negotiable on plate

Written by Ethan Bernard

Mills are less willing to talk price on spot orders on all the sheet products SMU tracks, but plate has veered the other way, according to SMU’s market survey this week.

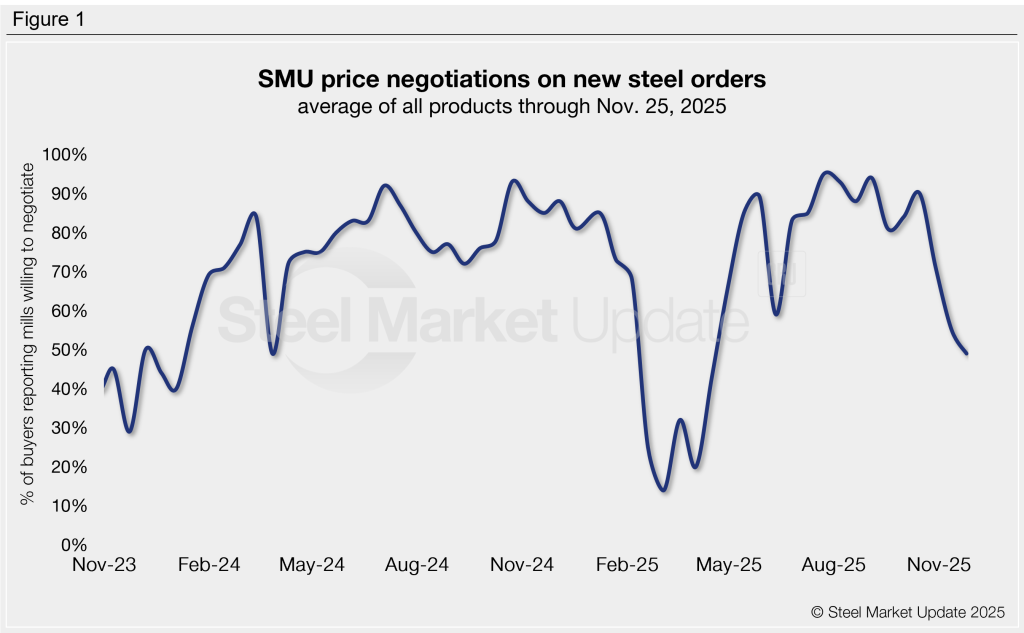

SMU polls hundreds of service center and manufacturer buyers every other week to see if domestic mills are negotiable on new spot order prices. This week, 49% of respondents said mills were negotiable on price, down from 55% two weeks earlier. We have to go back to mid-April when the rate stood at 43% to find a reading under 50% (Figure 1).

Negotiation rates ease on sheet, up on plate

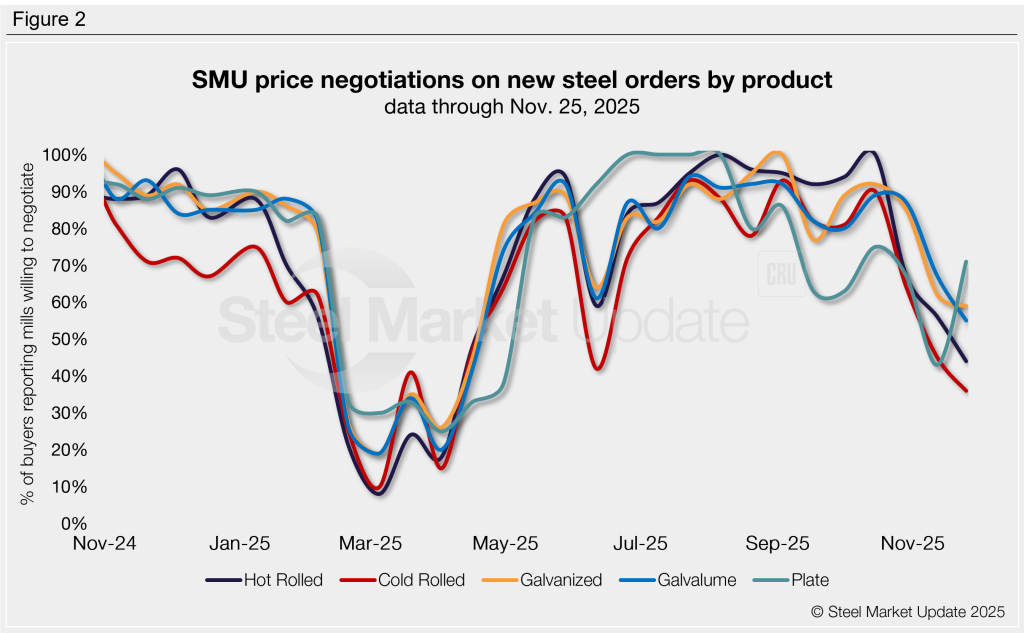

Of the five products we track, all sheet products saw lower negotiation rates this week vs. the previous survey, while plate bucked the trend. (Figure 2). Current rates are:

- Hot rolled: 44% of buyers said mills are willing to talk price, down 12 percentage points.

- Cold rolled: 36%, off nine points.

- Galvanized: 59%, down three points.

- Galvalume: 55%, down 12 points.

- Plate: 71%, up 28 points and the highest reading since early September.

Buyer remarks:

“US mills no, Canadian mills yes (on CR).”

“There is still December capacity and floor stock of galvanized coil with some mills, but pricing has been firm.”

“Right now there is little negotiation on HRC.”

“Trying to stick to closing their books on hot roll products. Can talk some mills in getting close to their contract pricing for spot—especially if it is additional tons to current contract.”

“Galvanized still seems to be the one product that is able to be negotiated right now.”

Note: SMU surveys active steel buyers every other week to gauge their steel suppliers’ willingness to negotiate new order prices. The results reflect current steel demand and changing spot pricing trends. Premium members can view an interactive history of our steel mill negotiations data on our website.