SMU Price Ranges: Sheet and plate prices flat or up (again) – for how long?

Sheet and plate prices were flat or modestly higher this week, continuing a trend we’ve seen since the beginning of Q4. The big question: How much longer can the trend hold?

Sheet and plate prices were flat or modestly higher this week, continuing a trend we’ve seen since the beginning of Q4. The big question: How much longer can the trend hold?

Nucor has increased its consumer spot price (CSP) for hot-rolled (HR) coil to $1,035 per short ton (st), a $10/st bump from last week.

The pace of sheet and plate price increases slowed this week, with most products holding at some of the highest levels seen in over a year.

Mexico’s Ministry of Economy issued a preliminary ruling in its anti-dumping case on hot-rolled steel from China and Vietnam. The government found evidence of price discrimination and imposed provisional duties on a wide range of hot-rolled flat products, including coils, sheet, strip, and plate.

Nucor raised its consumer spot price (CSP) for hot-rolled (HR) coil to $1,025 per short ton (st), up $10/st from last week.

Most steel buyers report that domestic mills are unwilling to negotiate price on new sheet and plate spot orders.

Chinese steel export prices and Turkish longs export prices increased this week due to higher energy and raw material costs. In India, HR coil exports remained paused amid the Middle East crisis.

The spread between domestic hot-rolled coil and prime scrap prices widened in March, marking a six-month trend.

SMU's sheet and plate prices were flat or higher this week in a US market that remains characterized by extended lead times and limited spot availability.

Nucor’s consumer spot price (CSP) for hot-rolled coil increased to $1,010 per short ton (st), up $5/st from last week.

Following extensions in February, steel mill lead times held steady or extended further for both sheet and plate products this week, according to buyers responding to our latest market survey.

Most steel buyers responding to our market survey this week said domestic mills remain unwilling to negotiate lower prices for new spot orders.

Sheet prices continue to grind higher on tight supply and 'okay' demand. Plate finally saw some movement after weeks of stability as price increases begin to stick.

Nucor’s consumer spot price (CSP) for hot-rolled coil increased to $990 per short ton (st), up $10/st from last week.

Participants in the domestic sheet market say they experienced lighter inquiries and fewer orders than in previous weeks, rendering domestic mill price increases for spot-market hot- and cold-rolled coils irrelevant.

The spread between domestic hot-rolled coil and prime scrap prices widened slightly in February. It has been trending in that direction since October.

The galvanized steel market is navigating price increases and longer lead times with a surer footing than in prior months.

Hot rolled and galvanized lead times are about half a week longer than they were three months ago, while production times for cold rolled, Galvalume, and plate products are one to two weeks longer.

Since late 2025, mills have begun to hold a firmer stance on prices, tightening their grip at the start of this year and holding on since

Three of SMU’s price indices increased this week, while two remained steady, all holding at multi-month highs.

A narrow range has emerged, suggesting the market’s repricing of downside risk is starting to stick.

Hot-rolled coil hovering near $970 per ton could push toward $1,000, but Timna Tanners cautioned at the Tampa Steel Conference that anything “much above that” becomes difficult to sustain. Still, she argued that mills’ slow, disciplined price increases are working in their favor.

SMU’s sheet price indices inched up to new multi-month highs this week, while plate prices held steady.

Nucor’s consumer spot price (CSP) for hot-rolled coil increased to $975 per short ton (st), up $5/st from last week.

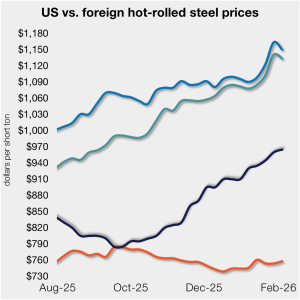

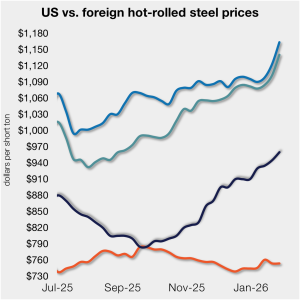

The price gap between US hot-rolled coil and landed offshore product narrowed this week, as price movements stateside and abroad diverged.

One third of the steel buyers responding to our market survey this week reported that domestic mills are negotiable on new spot order pricing. Mills began to hold a firmer stance on prices towards the end of last year, tightening their grip in early January and holding it since.

Steel mill lead times marginally declined on sheet products this week but edged higher on plate, according to responses from SMU’s latest market survey. Overall, lead times remain one to two weeks longer than levels seen three months ago.

Flat-rolled steel prices inched upward again this week as mixed demand appeared to be offset by limited supplies.

Nucor’s consumer spot price (CSP) for hot-rolled coil increased to $970 per short ton, up $5/st from last week.

The price gap between US hot-rolled coil and landed offshore product inched higher, even as prices stateside and abroad mostly moved in tandem vs. last week.