Canada

December 16, 2025

December energy market update

Written by Brett Linton

Editor’s note: Steel Market Update is pleased to share this Premium content with Executive members. For information on how to upgrade to a Premium-level subscription, contact Luis Corona at luis.corona@crugroup.com.

In this Premium analysis we examine North American oil and natural gas prices, drill rig activity, and crude oil stock levels through December. Trends in energy prices and rig counts serve as leading indicators for oil country tubular goods (OCTG) and line pipe demand.

The Energy Information Administration (EIA) recently released its Short-Term Energy Outlook (STEO) for December. The latest report continues to forecast declining crude oil prices through 2026 due to rising global inventories. Natural gas prices are being pushed up by colder winter weather, though rising production and milder weather are expected to help moderate prices after the winter season. US electricity generation is forecast to grow due to increasing data center demand. View the full December STEO report here for detailed insights on energy prices, production, inventories, and more.

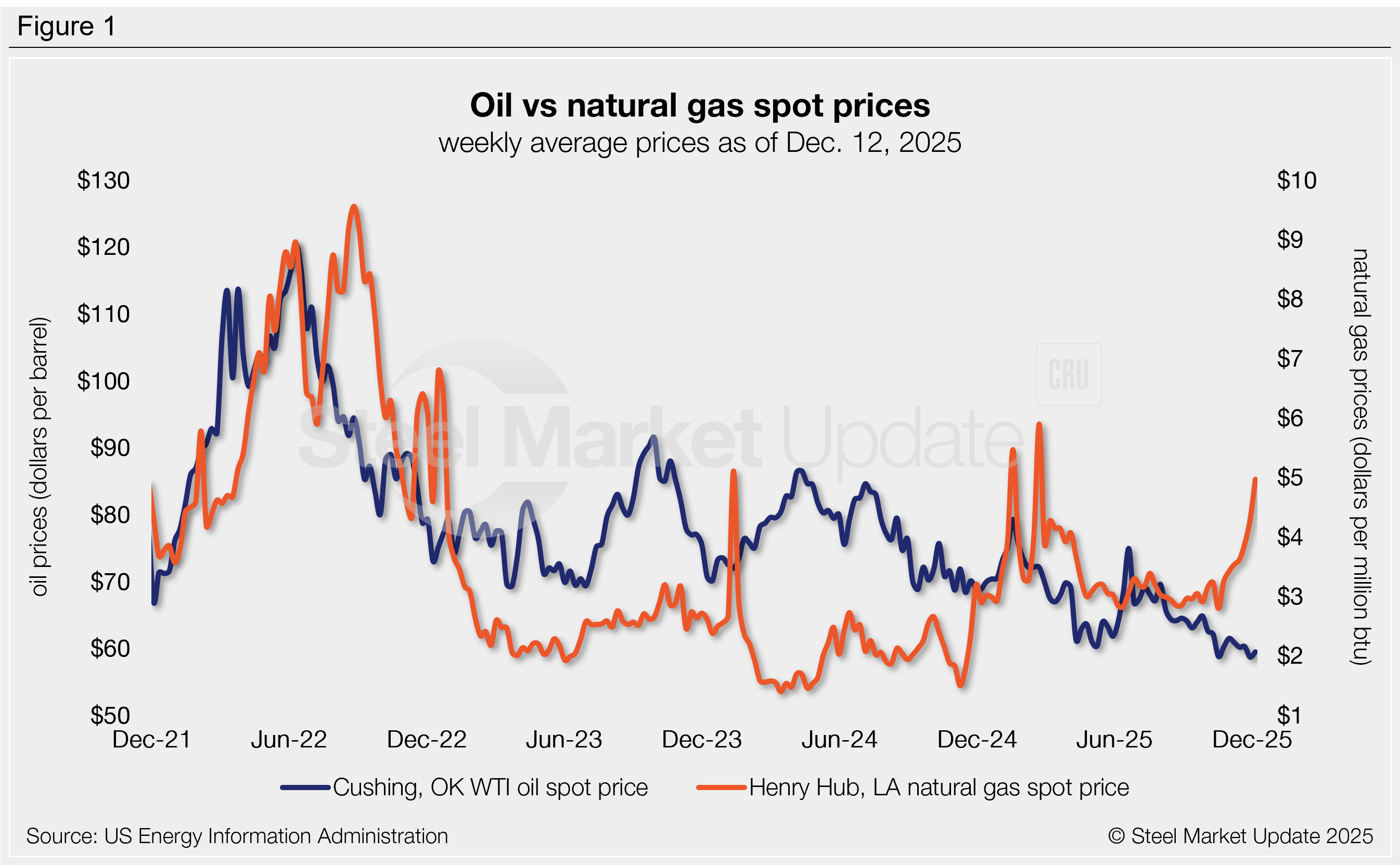

Oil spot prices

The weekly West Texas Intermediate oil spot market price has trended lower since June and has remained outside of its usual $70-90/b range for most of the year. In late November it reached $58.69 per barrel, the lowest weekly rate seen since early 2021. As of Dec. 5, it has inched up to $59.48/b (Figure 1).

The December STEO forecasts oil spot prices to average $55/b in the first quarter and remain around that price throughout the year.

Gas spot prices

Natural gas spot prices have surged in the last two months, rising to a near 10-month high of $4.97/mmBtu (million metric British thermal units) as of Dec. 12. This time last year prices had also rapidly climbed higher, jumping from under $2.00/mmBtu in October and November to around $3.00/mmBtu in December.

EIA expects natural gas prices to increase further through the end of the year, forecasting average winter rates of $4.30/mmBtu (up $0.40 from their previous estimate). 2026 prices are expected to average roughly $4.00/mmBtu.

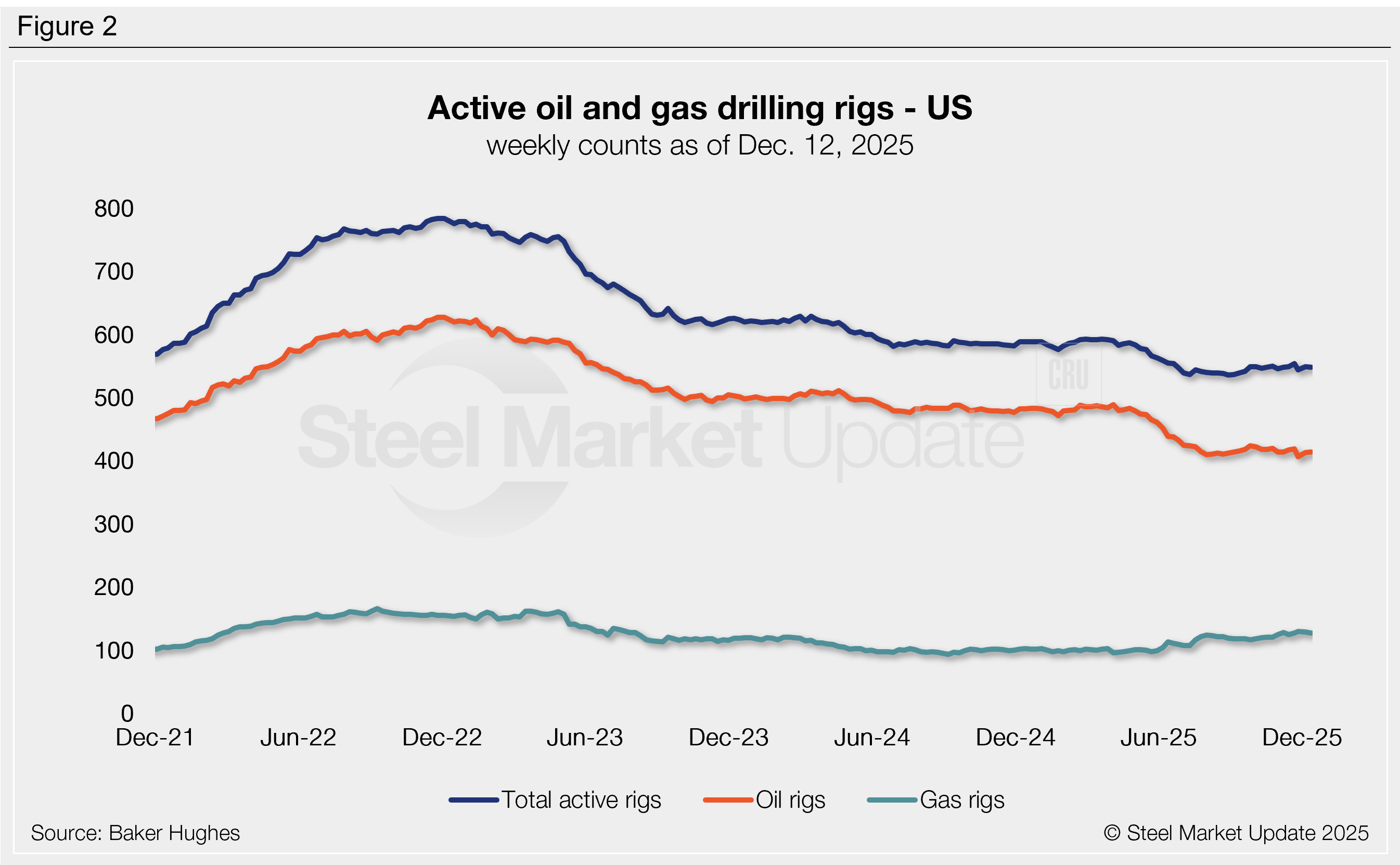

Rig counts

US drilling activity continues to hover just above historic lows, having remained at reduced levels for over a year. The latest count eased by one last week to 548, only 12 rigs higher than the near-four-year low set back in August (Figure 2). This total consisted of 414 oil rigs, 127 gas rigs, and seven miscellaneous rigs. Compared to the same week of 2024, there were 41 fewer rigs in operation this week.

EIA expects US drilling to remain relatively stable, keeping inventories high and oil prices under pressure through 2026.

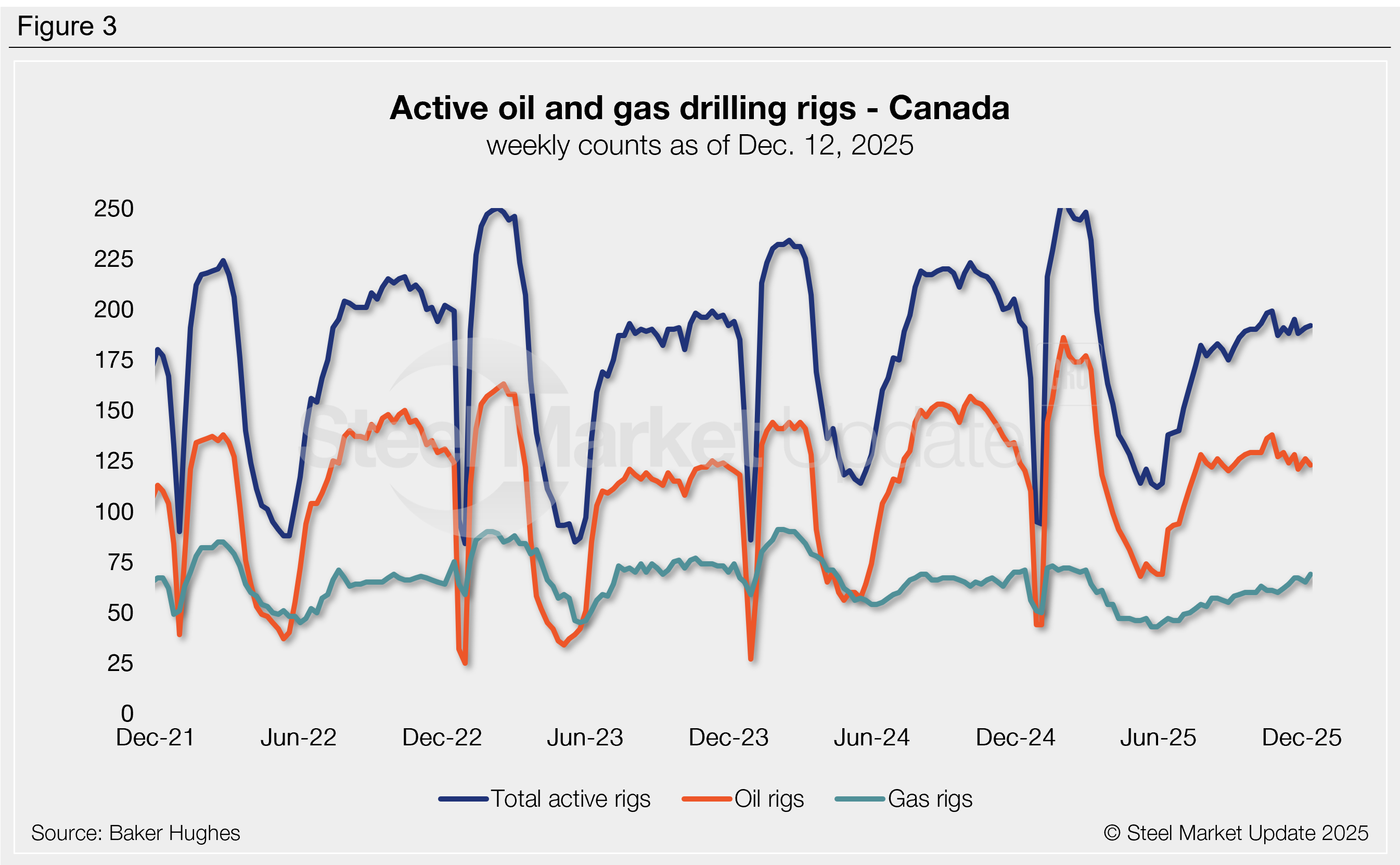

Canadian counts remain comparatively healthy, rising by one rig last week to 192, nearly identical to year-ago levels (Figure 3). This count consisted of 123 oil rigs and 69 gas rigs. Canadian activity should begin to slow in the coming weeks, a seasonal dip that typically occurs around the holidays.

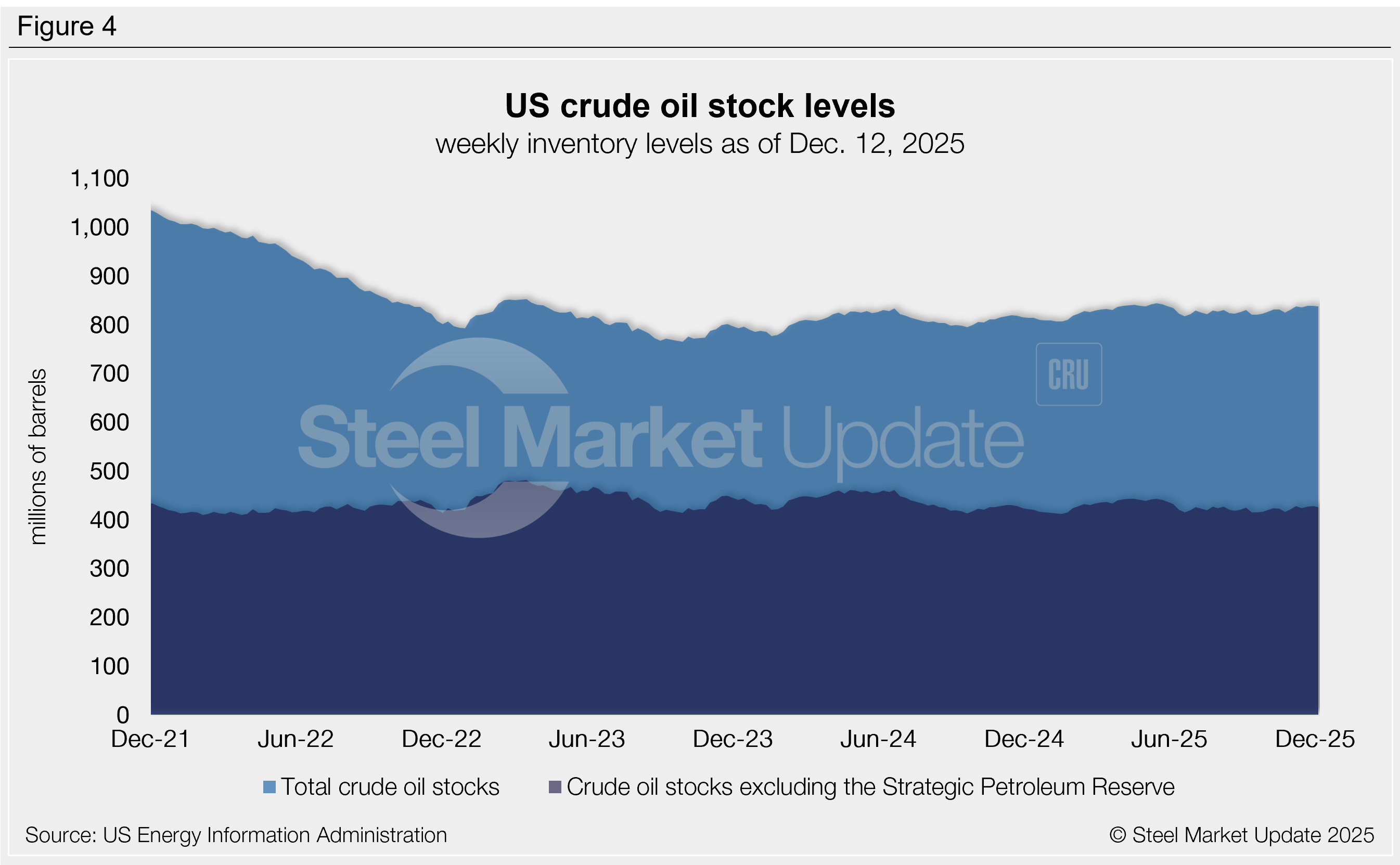

Crude stock levels

US crude oil stock levels continue to hold relatively stable, as they have done since the start of the year. As of Dec. 12, stocks totaled 838 million barrels, one of the higher rates seen in the last six months. Compare this to the two-year high of 844 million barrels set back in May. Stocks are 3% higher than they were this time last year (Figure 4).