Market Data

December 18, 2025

AIA: Architecture firms face prolonged billing declines as 2026 looms

Written by David Schollaert

Architecture firms across the United States continued to grapple with weak billings in November, as economic conditions added to the uncertainty, according to the latest Architecture Billings Index (ABI) report from the American Institute of Architects (AIA) and Deltek.

“Weakness in business conditions at architecture firms continues to be widespread, with declining billings across all major specializations and in every region except the Midwest,” said AIA Chief Economist Kermit Baker.

There were some bright spots, though, in the November report. Inquiries for new projects and design at firms in the Midwest ticked higher — a region that traditionally has the lion’s share of manufacturing activity.

The region, Baker said, “appears to have hit its bottom for this cycle and is expected to continue to improve.”

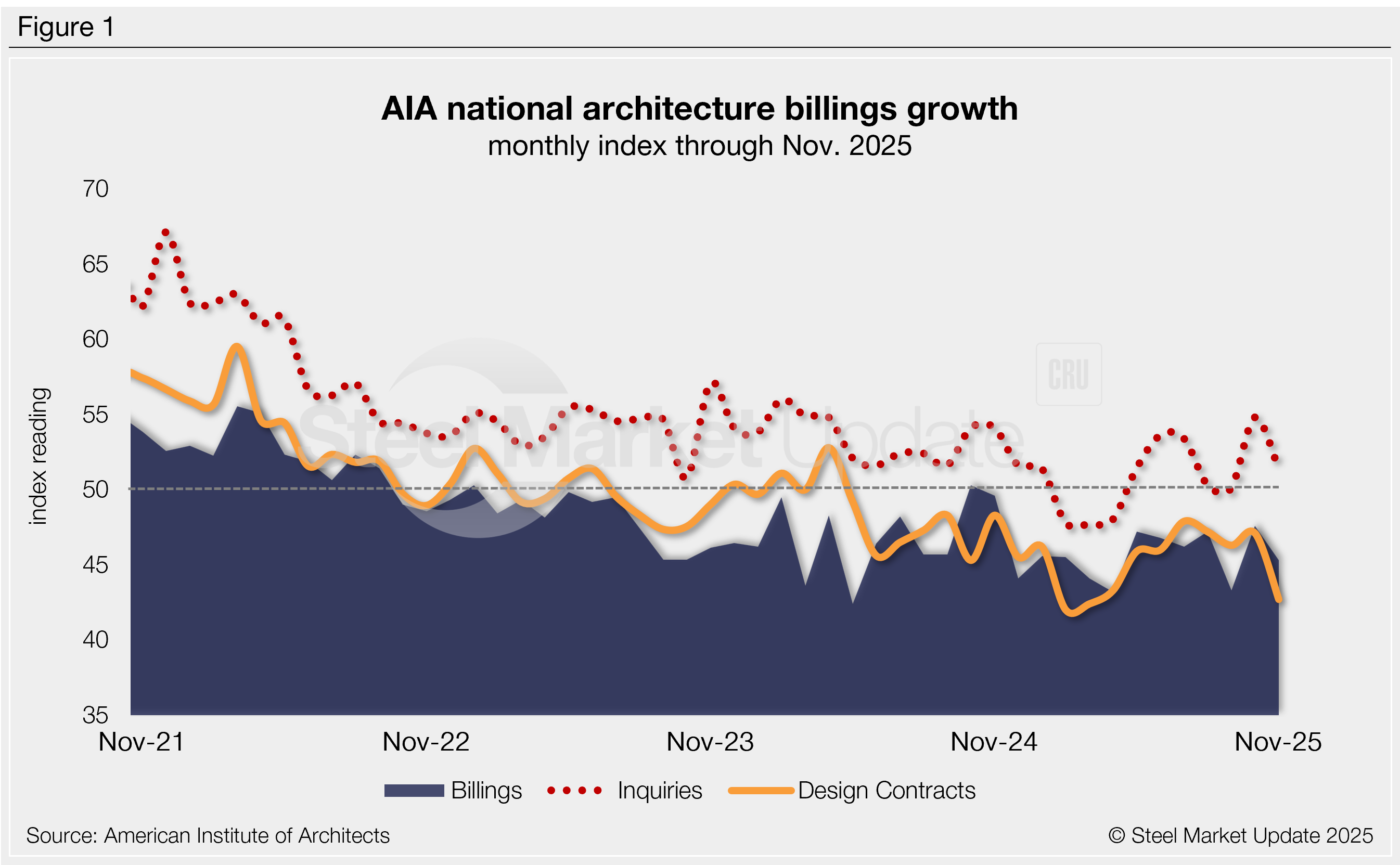

The November ABI ticked down 2.3 points from October to 45.3, and one of the lowest readings of the year (Figure 1). The ABI has been in contraction for all but two months since October 2022, indicating consistently weakening business conditions since the post-pandemic rally.

The ABI is a leading indicator of nonresidential construction activity, typically projecting business conditions approximately 9-12 months in the future (the usual lag between architecture billings and construction spending). Readings above 50 indicate increasing billings, while those below indicate reductions.

Participant comments:

- “Healthcare, our primary market, is typically busy at this time of year as clients look to us for budget numbers for planned work. So proposal activity is strong, but not all turns into real work.” — Western firm with institutional specialization

- “Uncertain about 2026 conditions. Architects and contractors appear steady, but pipelines are not as full.” — Southern firm with commercial/industrial specialization

- “Things still feel a bit slow, although we’ve been pretty good most of the year. We are slightly worried about Q1, but if we get our normal signs in January/February, we’re going to be fine.” — Midwestern firm with multifamily residential specialization

- “Conditions are mixed. Clients are still adjusting to the ever-increasing costs of construction.” — Northeastern firm with commercial/industrial specialization

Subindex trends

The new project inquiries index declined 3.4 points to 51.4 after reaching a 19-month high in October, but still marked a sixth consecutive month of growth. The design contracts index fell further in contraction — now for a 19th straight month — at 42.7, the lowest reading since March.

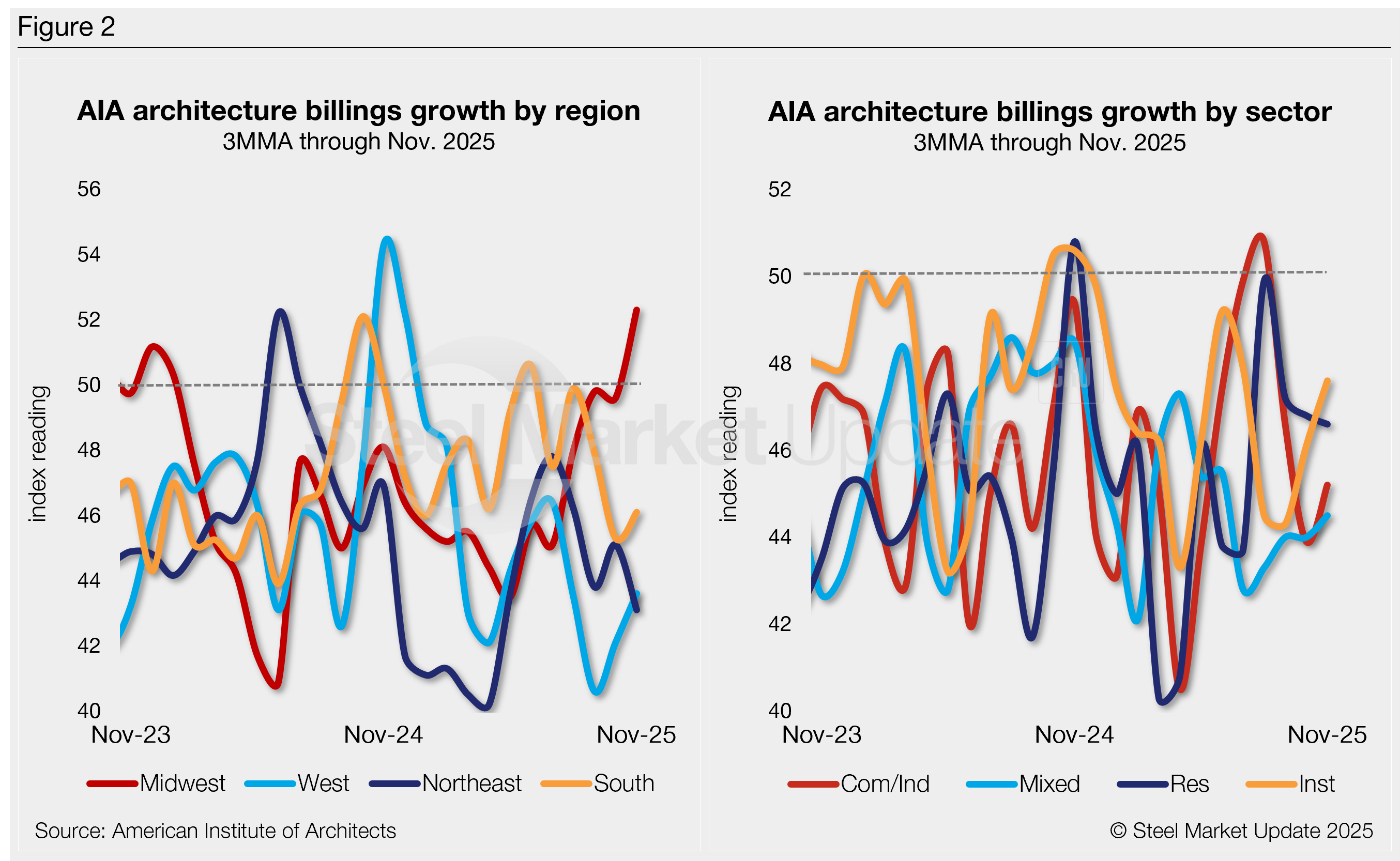

Three out of four regional indices (Midwest, South, and West) ticked higher from October to November. And while the Midwest moved into expansion for the first time since January 2024, the other three stayed below the 50 threshold (Figure 2, left).

Three of the sub-sector indices were also up from October (all but residential), but continue to indicate a reduction in billings. Residential was down 0.2 points to 46.6 (Figure 2, right), while institutional was up 1.5 points to 47.6.

Looking ahead to 2026, AIA found that firm leaders cite profitability as their top concern. In an annual survey, 56% identified increasing profitability as a major issue, alongside finding new clients and negotiating fair fees.