Analysis

January 11, 2026

Final Thoughts: The 'Donroe Doctrine'

Written by Ethan Bernard

The first SMU Survey results of 2026 have arrived. And you thought the time for gifts was over. Well, our survey is year-round, and you never know what kind of precious data it will contain until you click on the file.

What’s in this week’s results, you ask? Well, the full results are available to all our Premium subscribers. (You can subscribe or upgrade here.) But we’re going to give everyone not only a peek at the data, but also some participant comments. A pretty visual slide, and market comments all along the value chain. Who could ask for more?

We’ll zoom in on the popularity of Trump’s tariffs, reshoring, demand, and HRC prices. Wondering about the weather and how it could affect scrap flows? I asked CRU’s proprietary AI if there were any odds out yet on if the legendary “Punxsutawney Phil’ will see his shadow on Groundhog Day 2026. But nothing yet. We’ll keep you posted.

For those other issues, check out below for slides and participant comments underneath.

One comment on tariffs really stood out, and I wonder if it might be a way to frame this entire presidential term.

“But how about the Donroe Doctrine?”

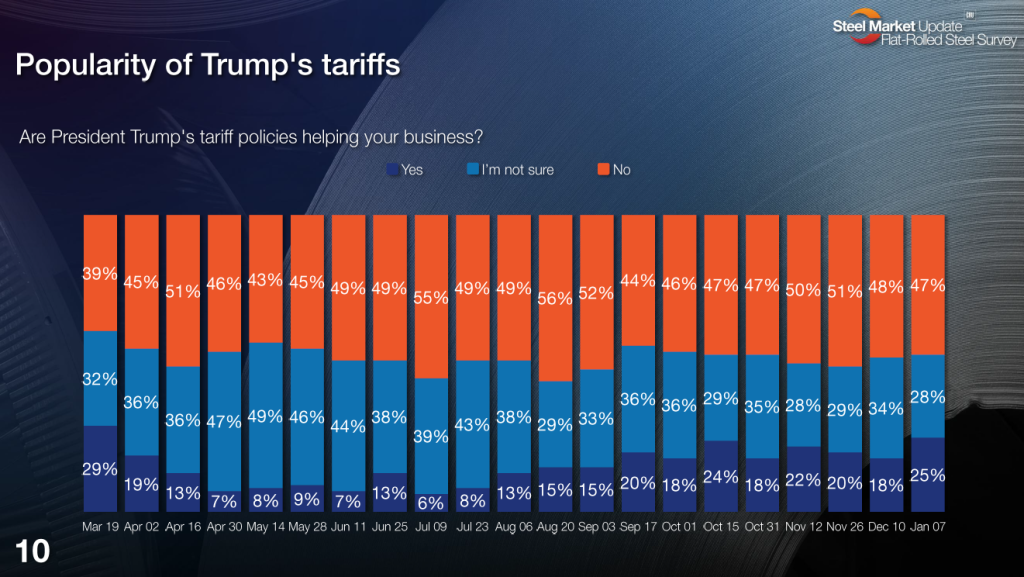

Are President Trump’s tariff policies helping your business?

“If anything, I get the sense that business has slowed in ’25 vs. previous years. It seems to me that manufacturing has slowed a bit vs. ’24.”

“Some good, some bad. But more good than bad. 232 derivative products leveled the playing field.”

“Seems like we’ve seen a pretty solid pricing floor for a while now. If nothing else, that’s helping.”

“Less today than a few months back. Supply chains seem to be getting figured out.”

“They are creating too many barriers and raising price artificially.”

“They are allowing mills to have inflated selling prices and negatively impacting demand.”

“Seeing much higher demand overall from domestic mills.”

“Steel pricing levels remains elevated, which help everyone. See the Canadian market for the alternative.”

“Inventory values have increased.”

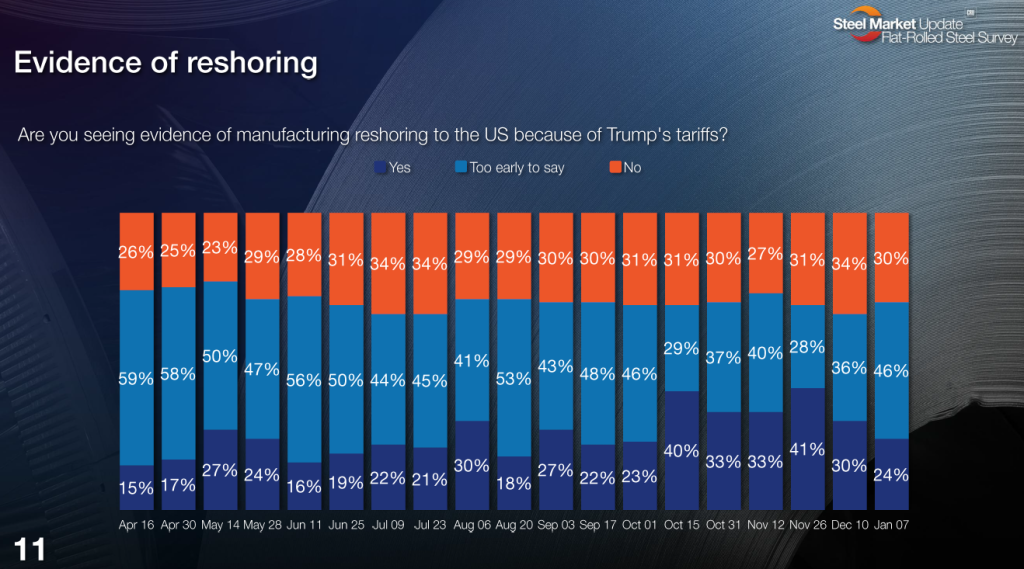

Are you seeing evidence of manufacturing reshoring to the US because of Trump’s tariffs?

“Little or no growth in the customers I’m calling on.”

“Anecdotal/specific industries (e.g., tube).”

“In most every industry.”

“Chatter remains, and I am sure there are some small examples that we are benefiting from. But it will happen organically.”

“A lot of announcements. Some smaller volumes have made their way back to the States.”

“Some might happen. But many are just waiting for the next administration.”

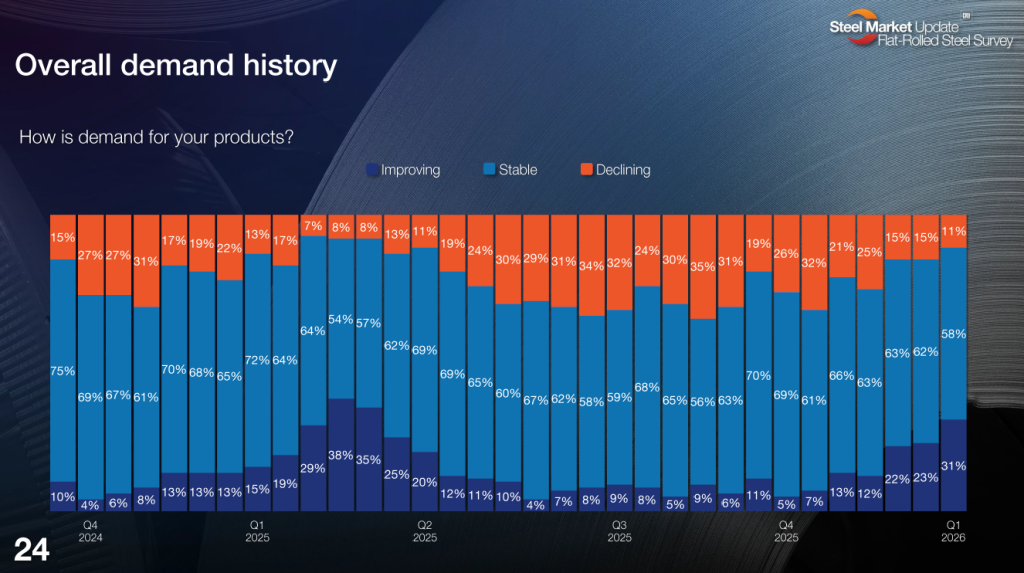

How is demand for your products?

“December was really slow, but January has had a strong start.”

“Demand is weak. But it’s hard to know as it’s been a slow holiday break and many customers are only returning this week.”

“Winter season has a huge impact on our products.”

“We will be producing fewer units in 2026 than we did in 2025.”

“Now that we are through the holidays, order books are solid.”

“Demand hasn’t changed much in last 8-9 months, just the same group of companies all fighting for the same orders.”

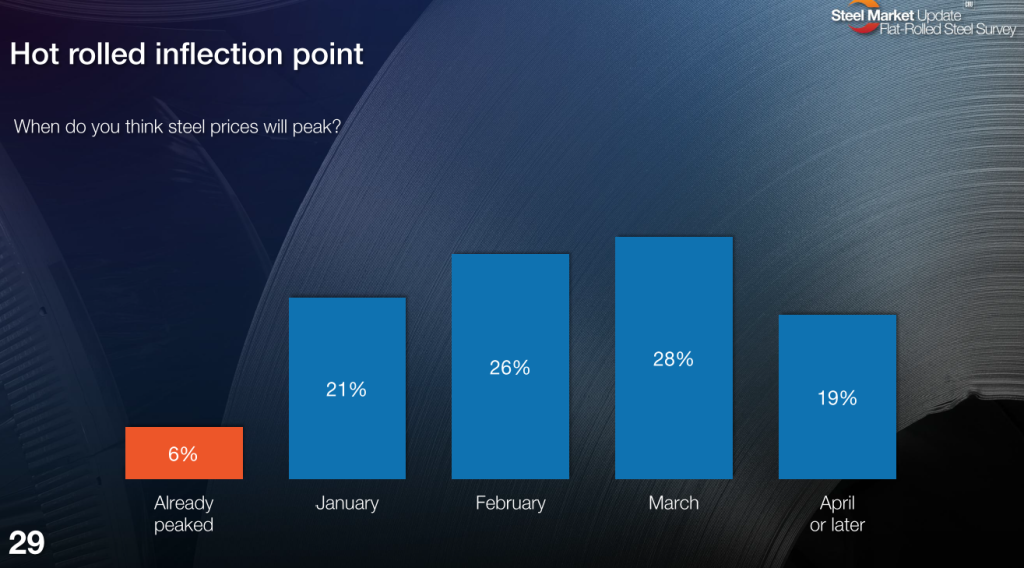

When do you think steel prices will peak?

“We are predicting a strong Q1.”

“Outages and shutdown have constrained supply.”

“Supply is short, so demand will be high.”

“I feel within the next 3-5 weeks pricing will peak unless something changes to spur real demand (not just some refilling of stock after depleting for year-end).”

“Prices should stay firm well into Q2.”

“Too many moving parts to stop raising prices now.”

“Demand is going to peak in January and inventory is still in a good position.”

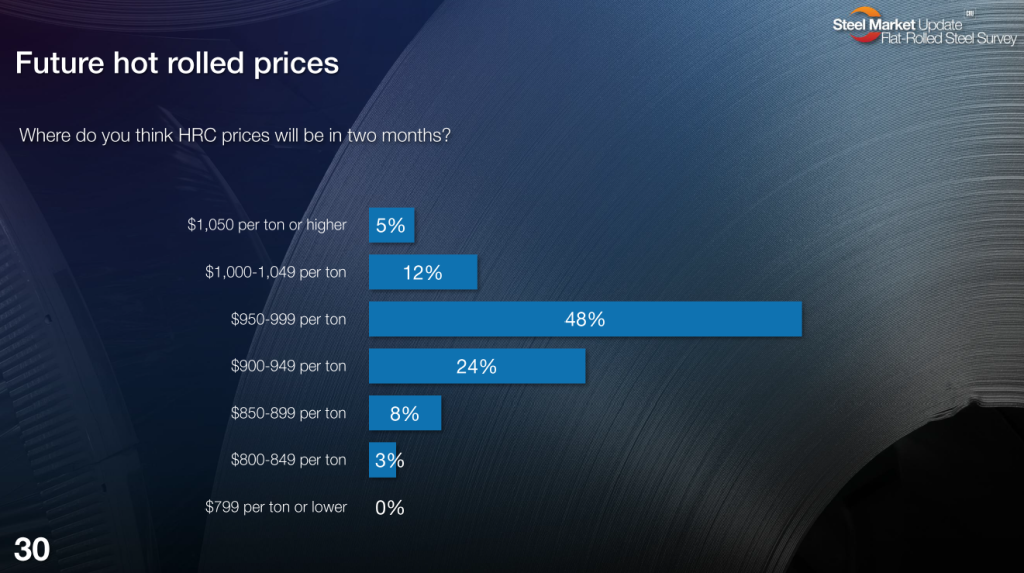

Where do you think HRC prices will be in two months?

“It seems to me that some foreign steel is now competitively priced with domestic steel, so I don’t see domestic steel prices going up much further.”

“Demand is still not great.”

“There is more room to increase. But once it gets over the psychologically important level of $1,000/ton, it might get pushback.”

“We don’t think we’ll quite get to $1,000/ton. And by late Q1, we’ll be falling back down.”

“I feel we will see some increases in the coming weeks followed by declines that get us to about where we are currently at.”

“Supply tightening while demand improving.”

“I believe this current pricing cycle peaks around the February scrap trade, and is coming back down by early March.”

“Strong order books, extended lead times, and low inventories.”

“Topping out below $980 per ton.”

Do you want to share your thoughts? Contact david@steelmarketupdate.com to be included in our market questionnaires.