Analysis

January 22, 2026

AIA: Architecture sector struggles through 2025 despite solid backlogs

Written by David Schollaert

Architecture firms across the United States continued to face weak business conditions through the end of 2025, as economic conditions added to the uncertainty, according to the latest Architecture Billings Index (ABI) report from the American Institute of Architects (AIA) and Deltek.

“Despite the ongoing decline in billings at most architecture firms, there are a few signs of potential improvement on the horizon,” said AIA Chief Economist Kermit Baker. “The number of inquiries into future project work continues to grow, and Midwest firms saw billings increase for the fourth consecutive month in December.”

There were still some bright spots, though, in the December report. Firms still hold relatively solid backlogs, suggesting that previously secured work is keeping pipelines stable even as new opportunities slow.

Still, Baker said, “Overall conditions remain weak across all specializations. Multifamily residential firms faced the steepest declines, while institutional firms experienced a slightly slower pace of decline compared to earlier in the year.”

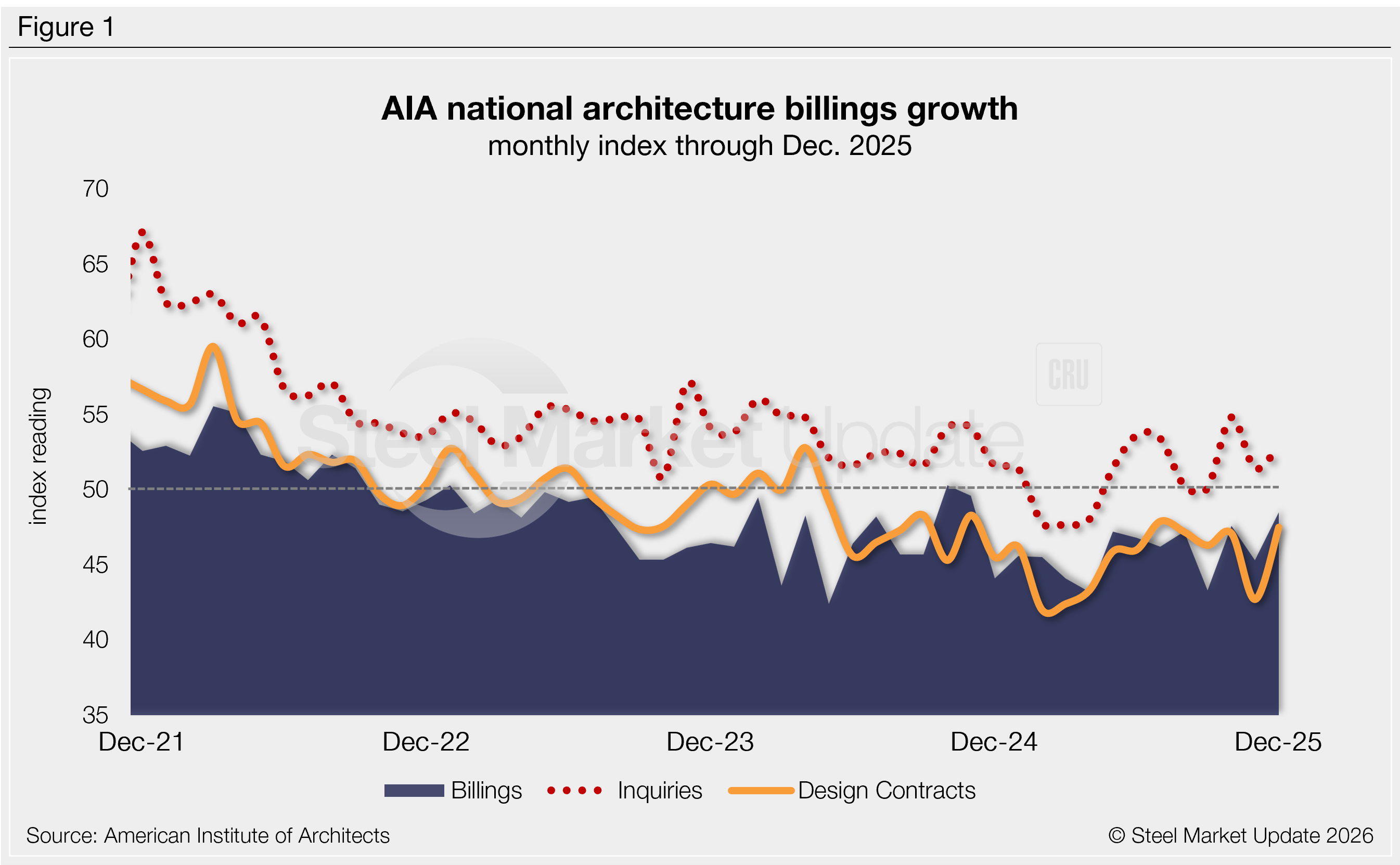

The December ABI ticked up 3.2 points from November to 48.5 (Figure 1). The ABI has been in contraction for all but two months since October 2022, indicating consistently weakening business conditions since the post-pandemic rally.

The ABI is a leading indicator of nonresidential construction activity, typically projecting business conditions approximately 9-12 months in the future (the usual lag between architecture billings and construction spending). Readings above 50 indicate increasing billings, while those below indicate reductions.

Participant comments:

- “It is very strong for select clients, like aviation and sports.”— A 520-person firm in the Midwest, institutional specialization

- “Demand for future housing has skyrocketed due to so few projects in the design/permitting pipeline. While the financing markets have moved in a positive direction, everything is still very tentative and unpredictable.”— A 54-person firm in the West, multifamily residential specialization

- “We’re seeing some prospects emerge, but many are in wait-and-see mode.”— Four-person firm in the South, commercial/industrial specialization

- “Conditions are slower than 2024, even though 2025 was a good year for us. Our clients are more cautious, and that means fewer RFPs for non-critical projects. Most of our current projects are related to much-needed infrastructure upgrades (mechanical systems, electrical switchgear, etc.).”— A 12-person firm in the Northeast, institutional specialization

Subindex trends

The new project inquiries index improved 1.5 points to 52.9, but is still behind a 19-month high seen in October, marking a seventh consecutive month of growth. The design contracts index improved, though it remained in contraction — now for a 20th straight month — at 47.5, up from 42.7 in November.

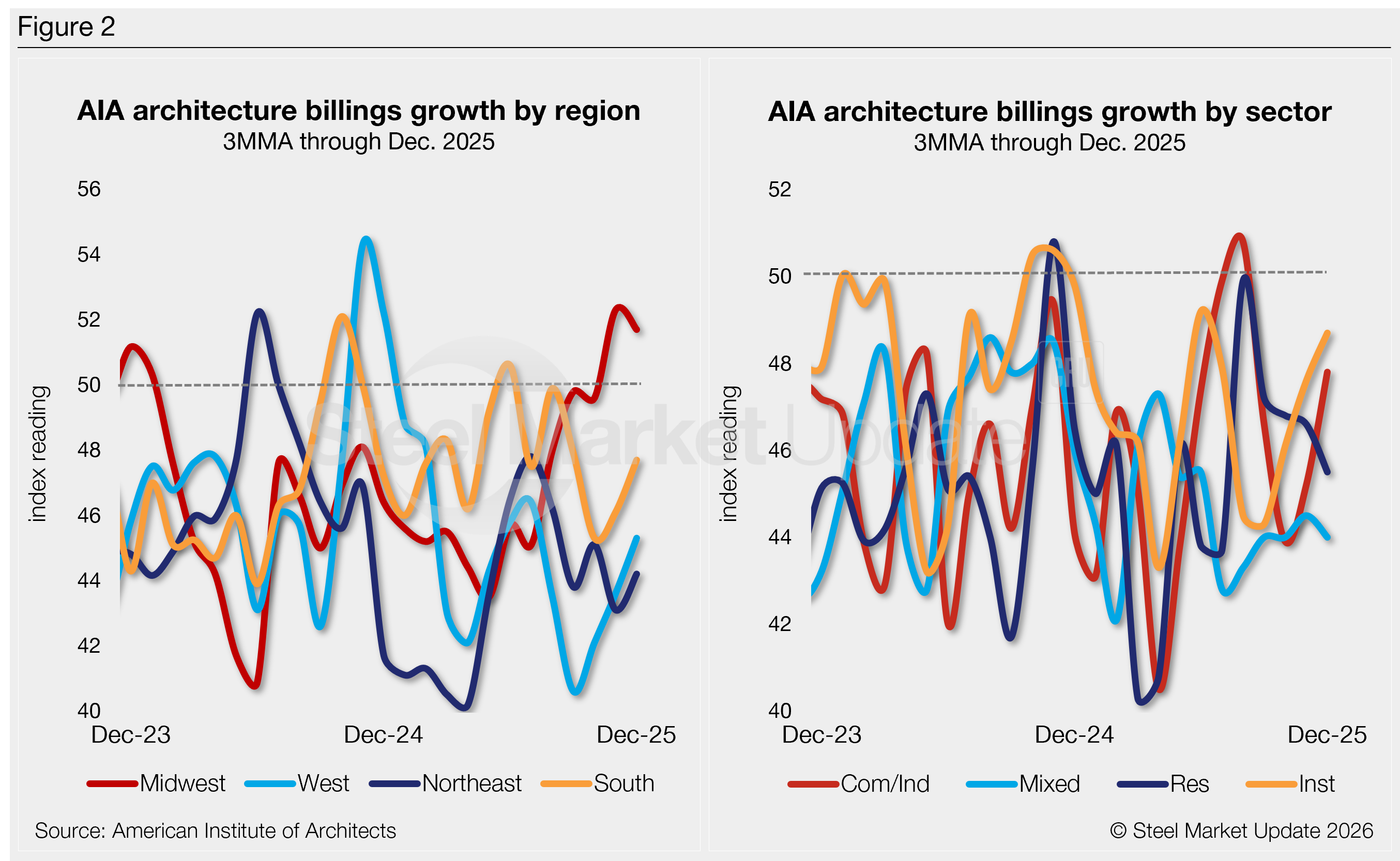

Three out of four regional indices (Northeast, South, and West) ticked higher from November to December. And while the Midwest remained in expansion, the other three stayed below the 50 threshold (Figure 2, left).

Two of the sub-sector indices were also up from November (institutional and commercial/industrial), but all continue to indicate a reduction in billings. Residential was down 1.1 points to 45.5 (Figure 2, right), while institutional was up 1.1 points to 48.7.

Looking ahead to 2026, AIA found that firm leaders cite profitability as their top concern. In an annual survey, 56% identified increasing profitability as a major issue, alongside finding new clients and negotiating fair fees.