Analysis

January 23, 2026

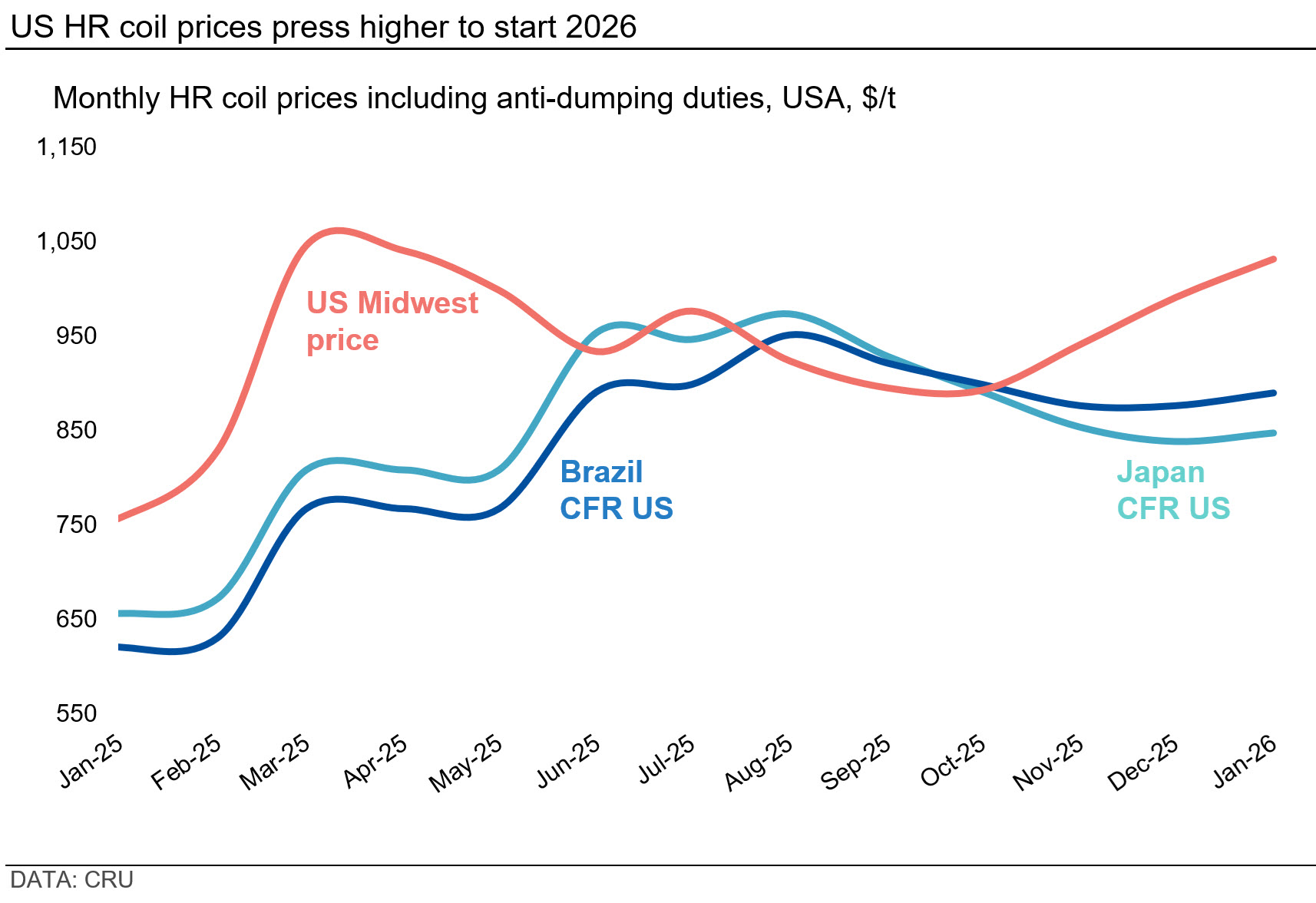

CRU: Fewer imports tighten US steel supply, supporting domestic prices

Written by Alexandra Anderson

This news item was first published by CRU. To learn about CRU’s global commodities research and analysis services, visit www.crugroup.com.

Lower finished steel imports continued to support US domestic prices this month. HR coil prices are up more than $40 per metric ton (mt) month-on-month (m/m) due to higher seasonal demand in January and tightening domestic supply.

The same trend was seen in the rebar market, as producers remained fully booked and rising scrap prices bolstered the market. However, market participants noted that rising US prices for finished steel may pave the way for higher imports as they become more cost-competitive.

Imports remain low, supporting US finished steel prices

All grades of US steel sheet prices trended higher to start the new year, although HR and HDG coil gains have slowed from December. Increased seasonal demand supported the market, as well as tighter supply domestically.

A drastic decline in imports due to S232 tariffs is largely the reason for this, in addition to the recent AD/CVD dumping rates imposed on multiple exporting countries (Australia, Brazil, Canada, Mexico, Netherlands, South Africa, Taiwan, Turkey, United Arab Emirates, and Vietnam).

Annualized, import arrivals in 2025 Q4 were 52% lower than in 2024 Q4, a difference of just over 4 million mt, well above the estimated capacity growth of 2.4 million mt in 2025. Early license data from January suggests arrivals from Canada and Mexico are set to fall further.

US long products prices also started 2026 on an upswing, with most products rising m/m amid tight supply and higher scrap costs. Data centers and infrastructure continued to drive steady demand, while limited imports kept domestic availability constrained.

As with steel sheet, rebar imports fell nearly 60% in H2 2025 compared to H2 2024 due to the S232 tariff increases. In late December, the US Department of Commerce issued its preliminary determination in the rebar anti-dumping case against Algeria, setting an anti-dumping rate of 127%, and will issue a final determination in March 2026. This investigation is running concurrently with the Department of Commerce and International Trade Commission anti-dumping and countervailing investigations against Algeria, Egypt, Bulgaria, and Vietnam.

According to the US Census Bureau, Vietnam, Egypt, Algeria, and Bulgaria accounted for more than 60% of rebar imports through October 2025.

Brazilian slab export prices increased m/m

Brazilian slab export prices increased by $10/mt m/m in January to $480/mt fob Brazil due to higher demand, as well as higher Asian slab prices.

In terms of trade, slab export volumes increased by 13% m/m in December, ending 2025 with a 24% year over year gain. The main export market remained North America, accounting for 78% of the total exports. Exports to Europe increased significantly, from 7% of the total volume in 2024 to 14% of the total in 2025.