CRU

March 3, 2026

CRU: Energy, metals and fertilizers spike as war engulfs Middle East

Written by Ben Farey

This news item was first published by CRU. To learn about CRU’s global commodities research and analysis services, visit www.crugroup.com.

Crude-oil and natural-gas prices spiked, metals opened higher and some fertilizer benchmarks climbed after the US and Israel launched a “pre-emptive” strike on Iran, killing the supreme leader and plunging the region into chaos.

Traffic via the Strait of Hormuz carrying crude and liquefied natural gas (LNG) dropped 86% from February 28 to March 1, according to Lloyd’s List Intelligence. Three vessels were struck by projectiles since the conflict began over the weekend, the UK Maritime Trade Operations said. While there is currently no formal blockade of the strait, Iran has warned vessels to stay away. Shipowners are waiting for more information before navigating the narrow waterway – the route for 20% of the world’s oil and similar proportion of global LNG.

Iran extended its retaliation following the assassination of Ayatollah Ali Khamenei by striking Israel, Bahrain, Jordan, Dubai, Abu Dhabi, Qatar, Kuwait, Saudi Arabia and Cyprus as US President Donald Trump suggested the military operation may last as long as four weeks.

Brent crude rose as much as 13% to $82.37/barrel before paring some gains in early trade in London. Front-month natural-gas prices at the Dutch TTF hub climbed as much as 23% on March 2 to €39.305/MWh. Gold climbed 1.6% to $5,362/oz. The LME three‑month aluminum price rose as much as 3.3% on March 2, and was last seen trading at $3,240/t. This is $100/t higher than last Friday’s close amid expected disruption of Middle East supply.

The impact on the world economy, infrastructure, supply chains and trade flows will depend on the duration of the conflict and the length of disruption to oil and LNG flows from the region. Saudi Aramco’s oil facility at Ras Tanura was hit by a drone March 2, Reuters reported. Saudi Arabia’s energy ministry said there was no impact on the supply of petroleum products to local markets. No major crude-oil carriers have passed through Hormuz since February 28.

Israel shut down the Chevron-operated offshore Leviathan gas field over the weekend due to safety fears, reducing pipeline gas flows to Egypt’s nitrogen producers. The Karish gas field also halted output. In Egypt, Mopco reported a urea sale up $27/t for March loading although production was still said to be running in the country at the time of writing March 2. QatarEnergy Marketing delayed the announcement of its sulphur price for March, citing “recent geopolitical developments”. In China, the world’s biggest sulphur importer, domestic prices jumped RMB200/t.

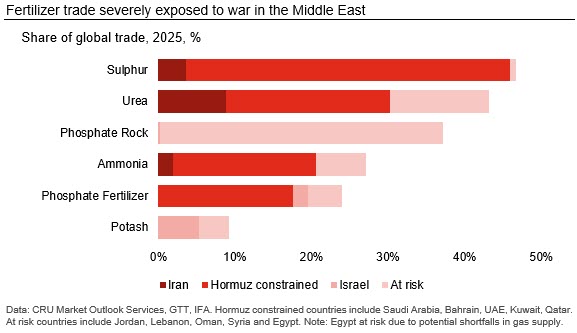

Fertilizers most at risk aside from energy

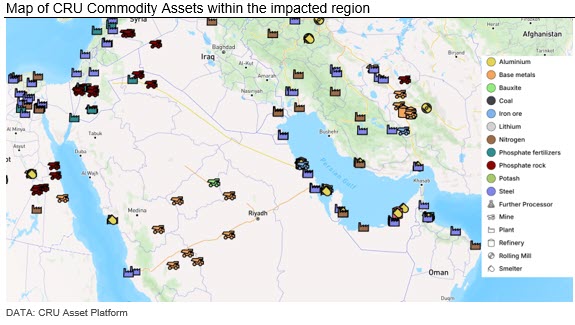

Fertilizers and fertilizer inputs are most exposed to the conflict – in particular sulphur trade, but also nitrogen and, to a lesser extent, phosphate shipments from Saudi Arabia, which must navigate Hormuz to reach their markets.

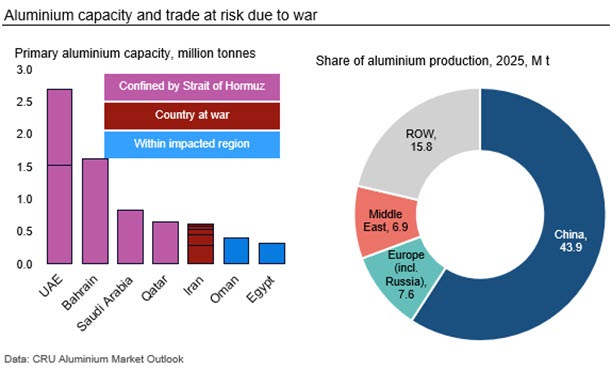

Aluminum supply at risk

For Gulf aluminum smelters (UAE, Bahrain, Qatar) the concern is not just how to export, but how they may import raw materials and 20-30 days of alumina is the maximum producers are likely to hold. EGA imports bauxite from Guinea. Maaden is more self-contained, but is impacted by the ability to export. The UAE has the option of circumventing the strait and exporting some metal from Fujairah directly on the Arabian Sea/Indian Ocean, although this export capacity is more limited and adds costs for land transportation. Iran has aluminum smelters, but information on their status is difficult to come by.

The strait is an essential waterway for all shipments to and from the Middle East, with the region representing over 20% of total primary output in the world outside of China.

In the short-term, aluminum supply will also be disrupted by the full closure of Mozal smelter in Mozambique, which seems unavoidable now. Meanwhile, Century announced the full restart of its Grundartangi smelter earlier than expected, but it will not be completed before the end of July.

Iran as a zinc producer

Iran is the only zinc producer in the Middle East. The conflict will likely put downward pressure on TCs because of the risk to output. This would put upwards pressure on the price. The country also exports high volumes of refined output, which if disrupted or viewed as likely to be disrupted, will put upwards pressure on the price. Still, information from Iran is difficult obtain. Zinc prices were down 1.8% on the LME at $3,309/t after some profit taking.

Impact on steel limited

The impact on the stainless value chain in terms of supply/demand is limited and largely restricted to higher energy prices that will impact production/freight costs and may trigger more demand at a later point (globally rather than from this particular region) due to stronger drilling activity and potentially investment.

Steel markets are likely to be influenced more by the second-order impacts of the war, such as higher energy prices.

Copper impact to be indirect

Copper impacts are also likely to be indirect. Iran produces small volumes of copper, with its exports typically destined for Asian markets. Copper remains near its all-time high at $13,343.50/t on the LME.

Tin prices near record

Tin prices gained more than 6% to $57,728/t on the LME as fears of supply disruption intensified.

Port disruption an evolving story

DP World said it paused operations at the port Jebel Ali in Dubai, among the busiest ports for container ships in the world. The port of Duqm in Oman was hit by drone strikes and closed on March 1. All ports in Bahrain were said to be closed, while those in Kuwait, Saudi Arabia, Egypt, Qatar and Jordan were open.