CRU

March 6, 2026

CRU: Middle East conflict poses energy cost risk to ferrous value chain

Written by CRU Group

This news item was first published by CRU. To learn about CRU’s global commodities research and analysis services, visit www.crugroup.com.

The main impact on the ferrous value chain from the Middle East conflict will be the higher energy costs in a prolonged scenario. Spot oil and gas prices are already moving higher, and, over time, this will impact steelmaking costs across all regions.

Energy costs are surging because of the disruption risk to both production assets and shipping through the Strait of Hormuz. The latter is also forcing up freight costs, which will affect delivered import prices for the overall ferrous value chain across importing markets. Escalation risk of shipping disruption to the Red Sea will add to this.

Steel long products will be more impacted by higher oil and gas costs compared to flats given their exposure via electricity for EAF-based production (BF-BOF energy inputs are chemical, from coke). Re-rollers and island sites will be also more exposed than assets, with local energy generation, for example from BF off-gases.

Other impacts centre on disruption to trade flows in and out of the region.

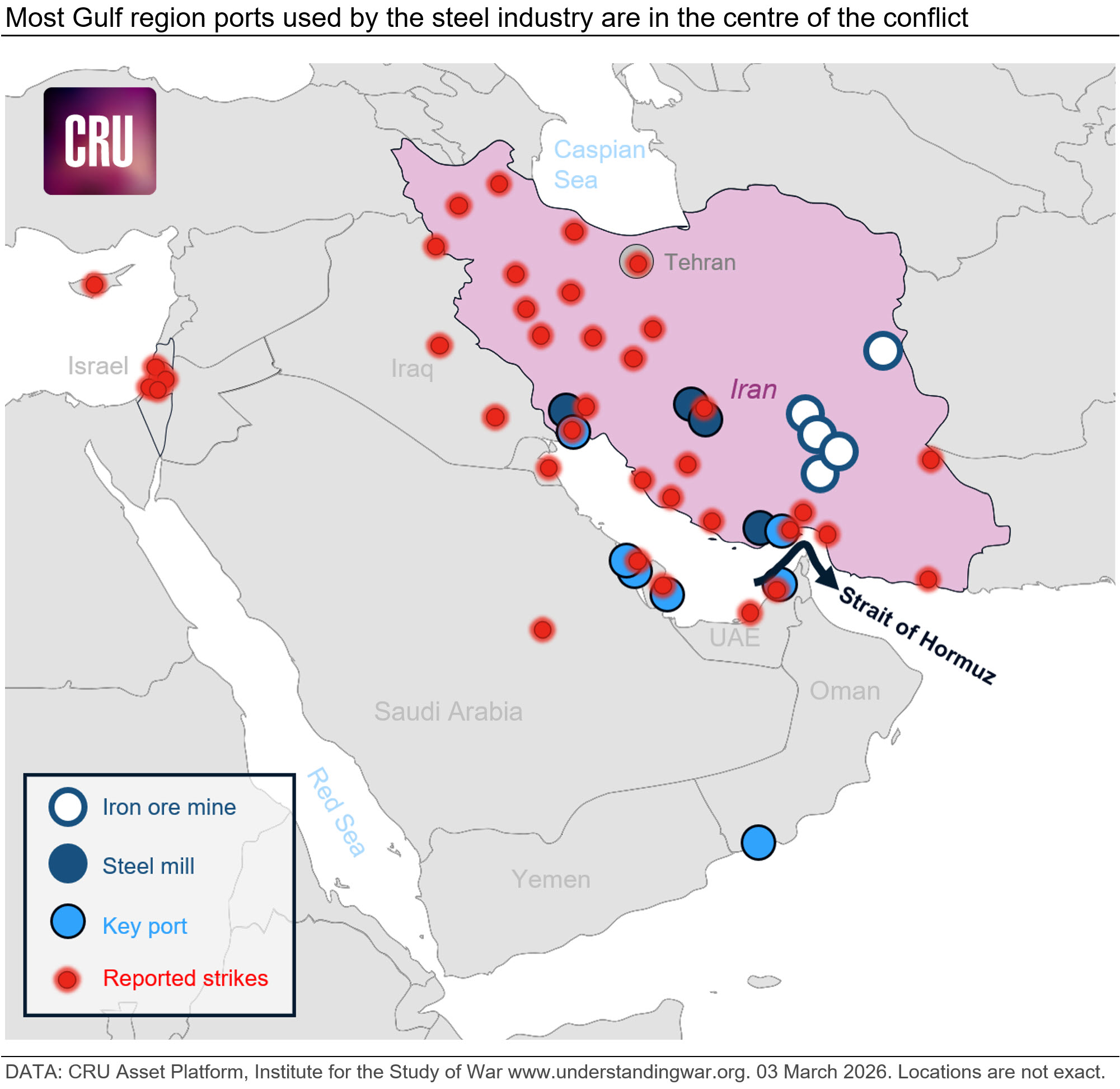

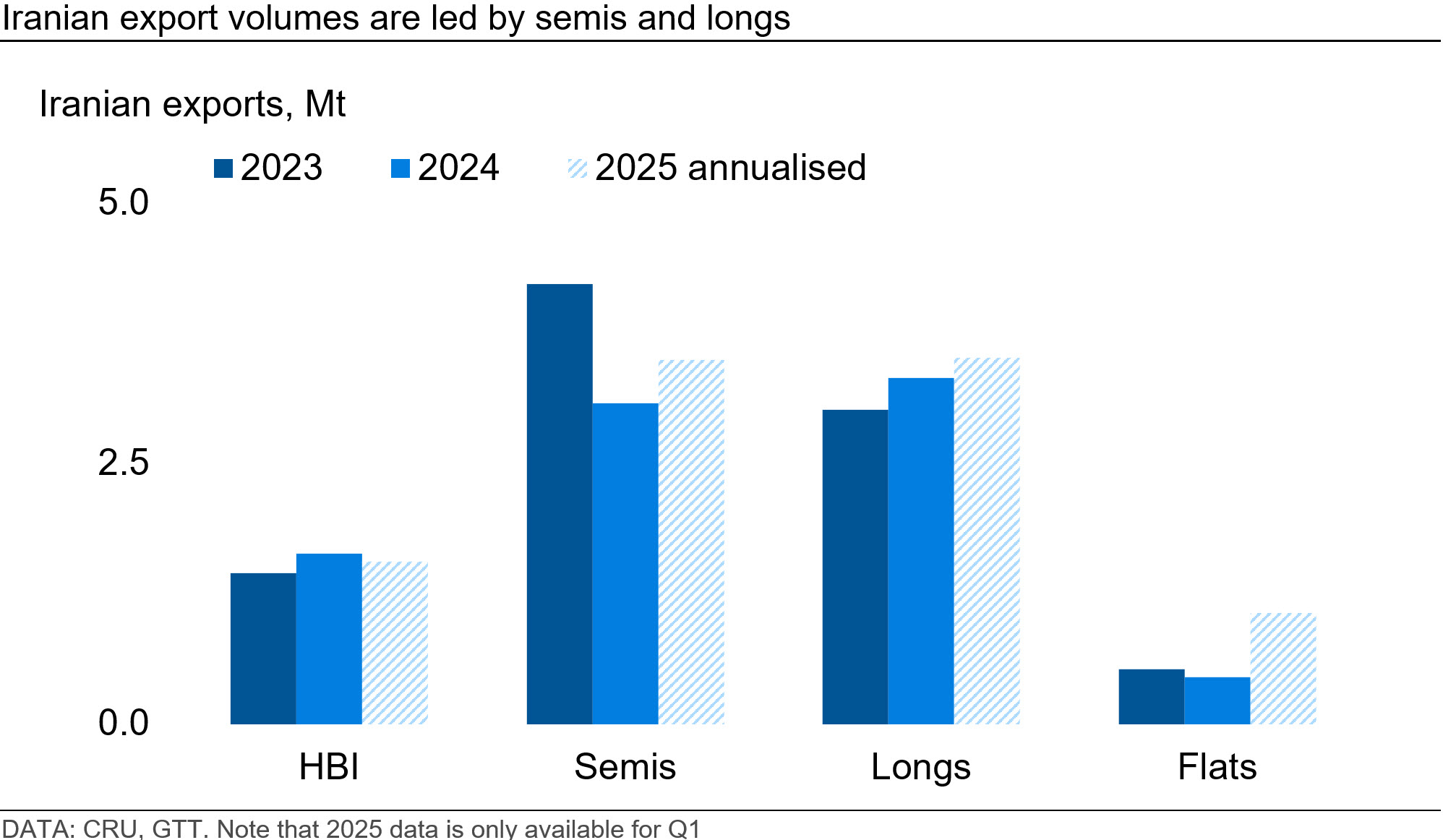

Iranian exports – largely semis and longs – are at risk

Iran is the largest crude steel producer in the Middle East and Africa. Production is predominantly gas-based DRI-EAF. Iran has built a large DRI industry that leverages domestic gas and iron ore reserves. It is the world’s largest DR-grade iron ore pellet producer and the second-largest DRI producer. Most output is consumed domestically and sanctions make exports challenging, although exports are facilitated by the country’s low production costs (for more information, please see CRU’s Asset Platform or request a demo here). In recent years, the country exported 6–8 million metric tons (mt) of steel per year, most of which was relatively low value-added products such as slab, billet, rebar and hot-rolled strip.

Current disruption in the Strait of Hormuz will cut Iran’s ability to serve export markets beyond, including China and India. Its biggest steel export market, Iraq, is over land and may remain accessible.

In parallel, any disruptions to natural gas or electricity supply in Iran would result in reduced DRI and steel output.

Raw materials markets will see a limited impact

Iran’s iron ore exports are also at risk. In 2025, Iran exported 6–7 million mt of iron ore, predominantly to China, either directly or via Oman. The direct impact on the broader iron ore demand-supply balance may be limited.

The Middle East consumes only 3 million mt per year of met coke, ~40% of which is imported. The region’s steel production is geared towards the DRI-EAF route, with Iran being the only country to house BF and coke capacity. It consumes ~2.8 million mt per year of coke to produce 3.5 million mt per year hot metal, importing ~33% of its coke requirement. Iran’s coking coal is sourced domestically, while its met coke imports are mostly from China. This implies limited impact on met coal and coke markets from demand destruction.

Freight risk escalation is a broader threat

On freight, a further risk is escalation to the Red Sea/Suez Canal, which would force widespread rerouting to impact cargoes otherwise unrelated to the Gulf region (often via the Cape of Good Hope), increasing voyage distances and schedule unreliability across container and dry bulk routes. In October 2023, Houthi attacks in the Red Sea forced trade flows to reroute to the Cape of Good Hope around Southern Africa. This increased shipping costs and lead times, thus raising delivered import prices across multiple markets. The same would happen if such attacks resumed now.

Inbound shipping also a risk

Shipping disruption threatens not only Iranian exports but also imports into other countries in the Gulf region. Saudi Arabia and the United Arab Emirates, for instance, import significant volumes of steel products – over 17 million mt between them in 2025, about half of which was from China.

The Middle East is also a key market for DR-grade iron ore pellet and pellet feed, with growing DRI production and domestic pelletising capacity. Infrastructure damage and freight disruptions are likely to weigh on the pellet and high-grade ore market, complicating price negotiations for Q2 sales.