Analysis

March 12, 2026

HR Futures: Stability shifts to repricing

Written by Gaby Ain

A month ago, the steel market was defined by stability. Prices had firmed and held, and the HRC futures curve appeared to be absorbing strength and follow-through rather than rejecting it. Since then, that stability has evolved into something more meaningful, repricing. Over the past few weeks, the front half of the HRC forward curve has lifted materially. The market is no longer simply acknowledging tighter conditions, it is reassessing how long those conditions may persist.

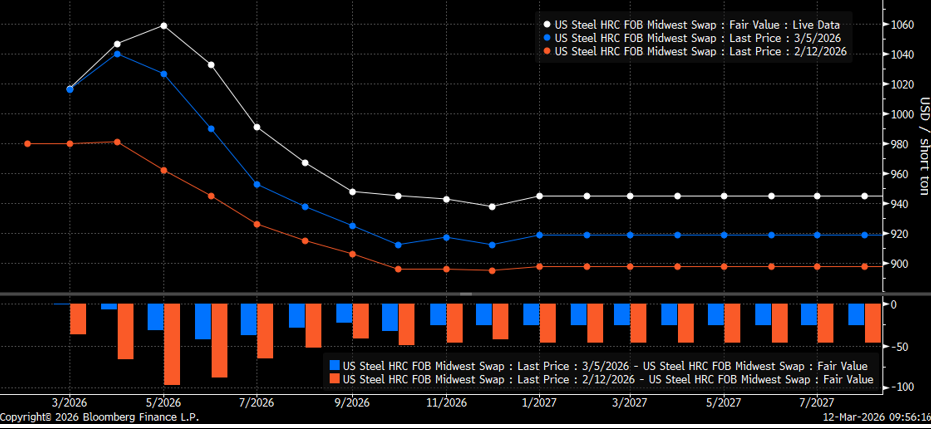

CME Midwest HRC futures curve (3/12 in white, 3/5 in blue, 2/12 in orange)

Looking at the evolution of the curve since my last column helps illustrate that shift. A month ago (orange), the market had largely stopped pricing a summer collapse, reached some stability but remained hesitant to fully embrace the rally, with future pricing still trading below the $1,000 level. As spot pricing began pushing through that psychological threshold, the tone of the curve started to change.

By a week ago (blue), strength in nearby months had begun lifting the belly of the curve. Today, (white), the front half of the strip has repriced even more decisively, with the peak of the curve shifting to May, aligning with the spring planned outage season, and spring contracts gaining roughly $40-100 over the past month. This suggests the market has moved from simply accepting tighter conditions to repricing the strength and duration of that tightness.

At the same time, the curve still reflects expectations of eventual normalization, maintaining a slope downward into the second half of the year. That structure suggests the market still anticipates the traditional balancing forces, such as imports responding to higher domestic prices, production normalization, and seasonal demand patterns eventually reasserting themselves.

However, even with expectation for some loosening later in the year, the stability of the back end remains particularly notable. Late-2026 and 2027 contracts continue to trade in a relatively tight band, lifting to now around $940. The market appears increasingly unwilling to price a return to the pre-2025 lows that characterized previous cycles. Structural forces like trade policy, cost structures, and supply discipline appear to be anchoring the long end at higher levels.

If that interpretation holds, the curve may be hinting at a broader shift in the structure of the steel cycle. Historically, steel pricing has oscillated dramatically, with swings between roughly $600 and $1,200. The current futures curve suggests a narrower regime, closer to $940-1060. Rather than boom-and-bust extremes, the market may be moving toward compressed cycles. In an environment shaped by trade barriers, consolidation, and reshoring, the industry may be entering a different type of pricing cycle.

CME HRC Money-Manager Positioning

Positioning data provides additional context. Net length among money managers remains among the largest seen in recent years, though it has eased slightly since my last column as both long and short exposure declined modestly. Even so, speculative positioning suggests the rally has become broadly accepted rather than actively contested. Consensus, however, does not eliminate risk. Crowded positioning can introduce volatility, as extended speculative exposure often becomes more sensitive to negative catalysts. Imports responding to higher domestic pricing, softening scrap market, production changes, tariff uncertainty, or broader macro developments could all shift sentiment quickly. In such environments, price movements can become driven as much by positioning adjustments as by changes in underlying fundamentals.

For now, the underlying physical market conditions remain supportive. HRC pricing surpassed the psychologically important $1,000 threshold. Mills continue to display pricing discipline, with Nucor’s consumer spot price (CSP) offer steadily grinding higher. Lead times remain extended, while demand is generally being described as steady rather than booming, uneven in places but not notably deteriorating. Import arrivals remain near the weakest environment since 2009 and with the spring outage season approaching, the physical market remains tight enough to support pricing.

Overall, the futures market has moved beyond simple stability. It has begun repricing how long tight conditions may persist. Whether that repricing proves justified will ultimately depend on how the supply side responds in the months ahead to higher prices.

Disclaimer

The content of this article is for informational purposes only. The views in this article do not represent financial services or advice. Any opinion expressed by Flack Global Metals or Flack Capital Markets should not be treated as a specific inducement to make a particular investment or follow a particular strategy, but only as an expression of his opinion. Views and forecasts expressed are as of date indicated, are subject to change without notice, may not come to be and do not represent a recommendation or offer of any particular security, strategy or investment. Strategies mentioned may not be suitable for you. You must make an independent decision regarding investments or strategies mentioned in this article. It is recommended you consider your own particular circumstances and seek the advice from a financial professional before taking action in financial markets.