Analysis

April 7, 2026

Final Thoughts

Written by Michael Cowden

More people expect hot-rolled (HR) coil prices to continue to climb. And most respondents to our last survey predict prices will hit or even breach the $1,100 per short ton (st) threshold.

Such predictions come even as many of those same people expressed concern about rising fuel and freight as well as the potential long-term impact of inflation stemming from the Iran War.

But as we note in our article on the latest SMU Price Ranges, such concerns to date haven’t changed the factors supporting high US sheet prices. Namely, low inventories, limited import competition, mill outages, and stable demand.

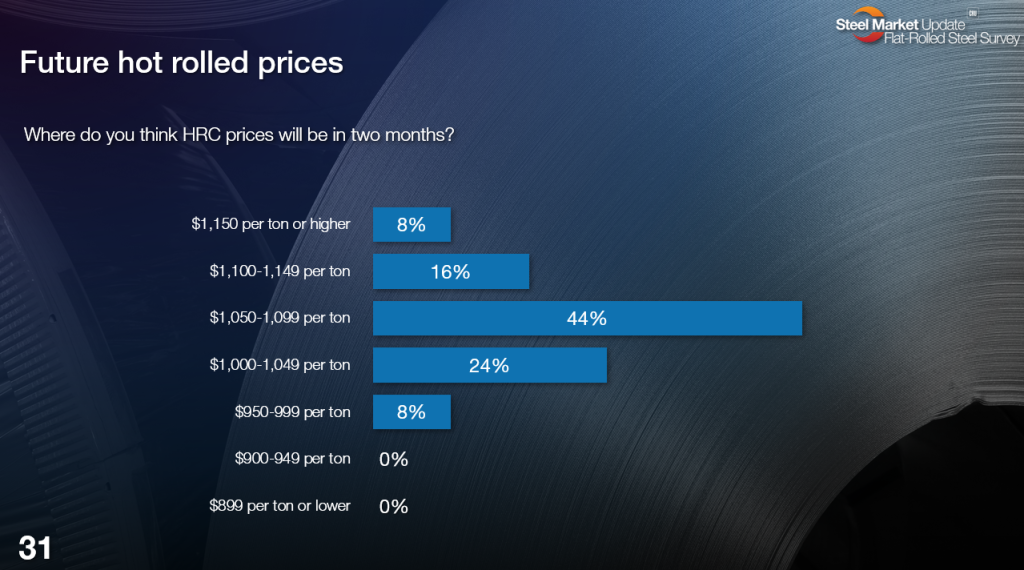

Where will HR prices be in two months?

So, let’s dive into that latest numbers. First, here is where survey respondents think prices will be in June:

(Editor’s note: You can click on the tables in this article to expand them. This represents a sampling of what you’ll find in our steel market surveys, which are available to our premium subscribers here. The numbers on the bottom left show where in the full deck you can find these charts. If you would like to upgrade from executive to premium to access such data, please contact us at smu@crugroup.com.)

The most common response (44%) is that HR prices will be in the range of $1,050-1,099/st, or slightly above where they stand now. That response implies mills, following practices introduced by Nucor, will continue to nudge prices higher by roughly $5-10/st per week.

A sizeable minority (24%) think prices will hold in the range of $1,000-1,049/st, or roughly where they are now. And the same percentage think prices will be above $1,100/st in early June. Only a few (8%) think HR price will sink back into the $900s/st.

Compare that to early March, when the most common response (31%) was that HR prices would be in the range of $950-999/st two months into the future. And only a small minority (7%) thought prices would cross $1,100/st.

Here is what some of them had to say, in their own words:

$1,150 or higher

“Demand is good.”

“Due to the war.”

$1,100-1,149

“There doesn’t appear to be anything keeping the mills from getting max pricing.”

“Energy pricing is going up and will keep prices elevated due to higher logistics costs.”

$1,050-1,099

“No sign of slowing down at the mills – and we’re still pushing out orders.”

“Still going up. I’m not sure how high they will go. But further from here.”

“Increased input cost may add a bit more to steel pricing.”

“Trickling upwards as the dominoes continue to fall.”

“I believe the top might be just under $1,200/st based on a tight-supply market – limited imports and strong demand.”

$1,000-1049

“With outages and inventories low, I do not see prices coming under pressure.”

“Very slow increases over the next several weeks.”

“We expect pricing to edge up to $1,100/ton but then start falling back as summer approaches. Maybe we see a low in the $800s by the back half of the year?”

“There is no argument for it to go up further.”

$950-999

“By the end of May, this market will be out of steam and hopefully slowly proceeding down the backside of the peak.”

“I don’t see the demand to justify current pricing. Something needs to give.”

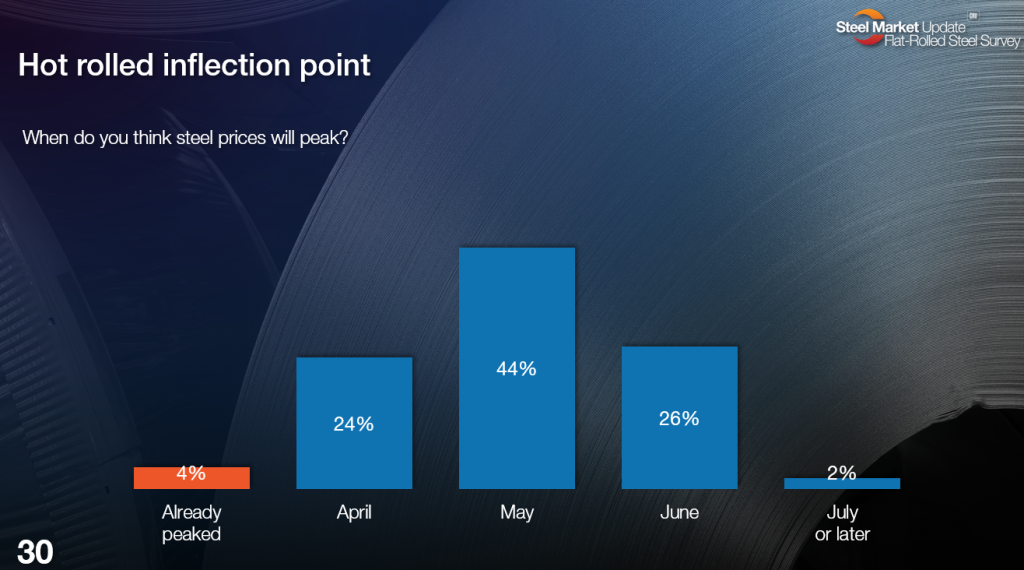

When will prices peak?

We see a similar pattern when we ask people when they think prices will peak. The most common response now (44%) is that prices will peak in May:

Compare that to last month, when the most common response (36%) was that prices would peak in April. In other words, survey respondents have been rolling predictions about when the market will peak from one month to the next as prices continue to inch higher.

Here is what some of them had to say, in their own words. (Fwiw, the folks who think prices won’t peak until July or later aren’t telling us why they think that.)

June

“Imports are coming in at these levels.”

“Supply in the spot market is still very tight.”

“Scrap will have corrected, planned outages are over, and summer doldrums are upon us.”

“Demand increases and supply tightness persists.”

“Due to tight steel supply.”

“Momentum.”

“Global uncertainty gives mills confidence.”

“Seasonal.”

May

“The Iran War will increase raw costs for mills.”

“The situation in Iran is affecting costs in general – could be a long way to go.”

“I don’t see the demand to justify current pricing. Something needs to give.”

“Momentum. Supply is tight. Foreign is scarce. Oil and associated manufacturing costs are up.”

“This rally, supply-driven as it may be, is still alive. Iran, spring outages, etc., will keep it going for a month or two more.”

“Downstream demand destruction will take a bit to catch up.”

“Still too much uncertainty in the near future.”

April

“Seems like we are close, but ultimately mills could push prices higher.”

“I feel there is more supply than what we will have for flat-rolled steel demand. We are seeing varying mill lead times, and I feel all will begin trending to the shorter ones – which will drive prices lower.”

“I really have no clue anymore. Everything has changed.”

Already peaked

“I don’t see the demand to justify current pricing. Something needs to give.”

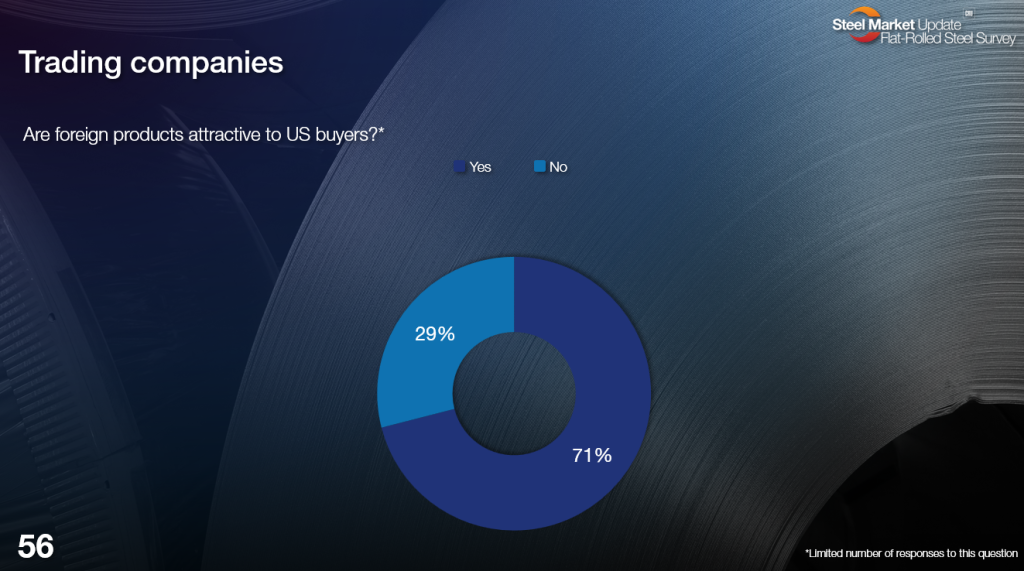

Imports on the way. But how many tons?

We’re relatively sure that more imports will find their way to the US markets based results like the one below.

Most traders tell us that foreign steel is attractive to US buyers. That’s a sharp change from last year, when US prices were lower and 50% Section 232 tariffs were enough to effectively wall off much of the US market.

But the question isn’t so much whether we’ll see more imports. It’s more a question of if the volumes will be enough to give more pricing power back to steel buyers.

The US was set to import 1.58 million metric tons (mt) of steel in March, according to license data from the US Commerce Department. That’s up modestly from 1.53 million mt in February and marks the highest monthly total since 1.70 million mt last August.

March’s total, however, is still well below the monthly average of 2.06 million mt we’ve seen over the last five years. Could we inch closer to that 2 million mt per month total as we get into Q3? And what foreign products might be seeing the most interest from US buyers?

Here is what some survey respondents had to say:

“If we can get offers, I believe we can be attractive due to limited domestic supply and high prices.”

“Coated and especially galvalume and pre-painted are attractive. HRC and CRC is as well. Bare galvanized not as much due to plentiful domestic supply. But as domestic prices keep increasing, that might change.”

“Hot holled to an extent and cold rolled.”

“Specialty steel strip.”

“Very light gauge.”

That doesn’t answer the volume question. But it gives you a hint that a wide spectrum of products could see more import interest in the months ahead – even if that does little to alleviate a tight spot market now.

Scouting the market so you don’t have to

Want to catch up with SMU in person? Then sign up to attend our VIP Industry Briefing on April 23 at the Swissotel in Chicago.

I’ll be presenting along with CRU Research Principal Josh Spoores and a few other special guest speakers.

We’ll be holding the event ahead of the Scout America Metals Industry Dinner just next door at the Hyatt Regency. There is no cost to attend. You can register here.