Plate

April 7, 2026

SMU Price Ranges: Sheet and plate continue to inch higher on tight spot market and despite Iran War concerns

Written by David Schollaert & Michael Cowden

Sheet and plate prices continued to hold steady or tick upward once again this week. The factors behind the gains are familiar ones: limited spot tonnage, stable demand, limited import competition, and outages (planned or otherwise) at domestic mills.

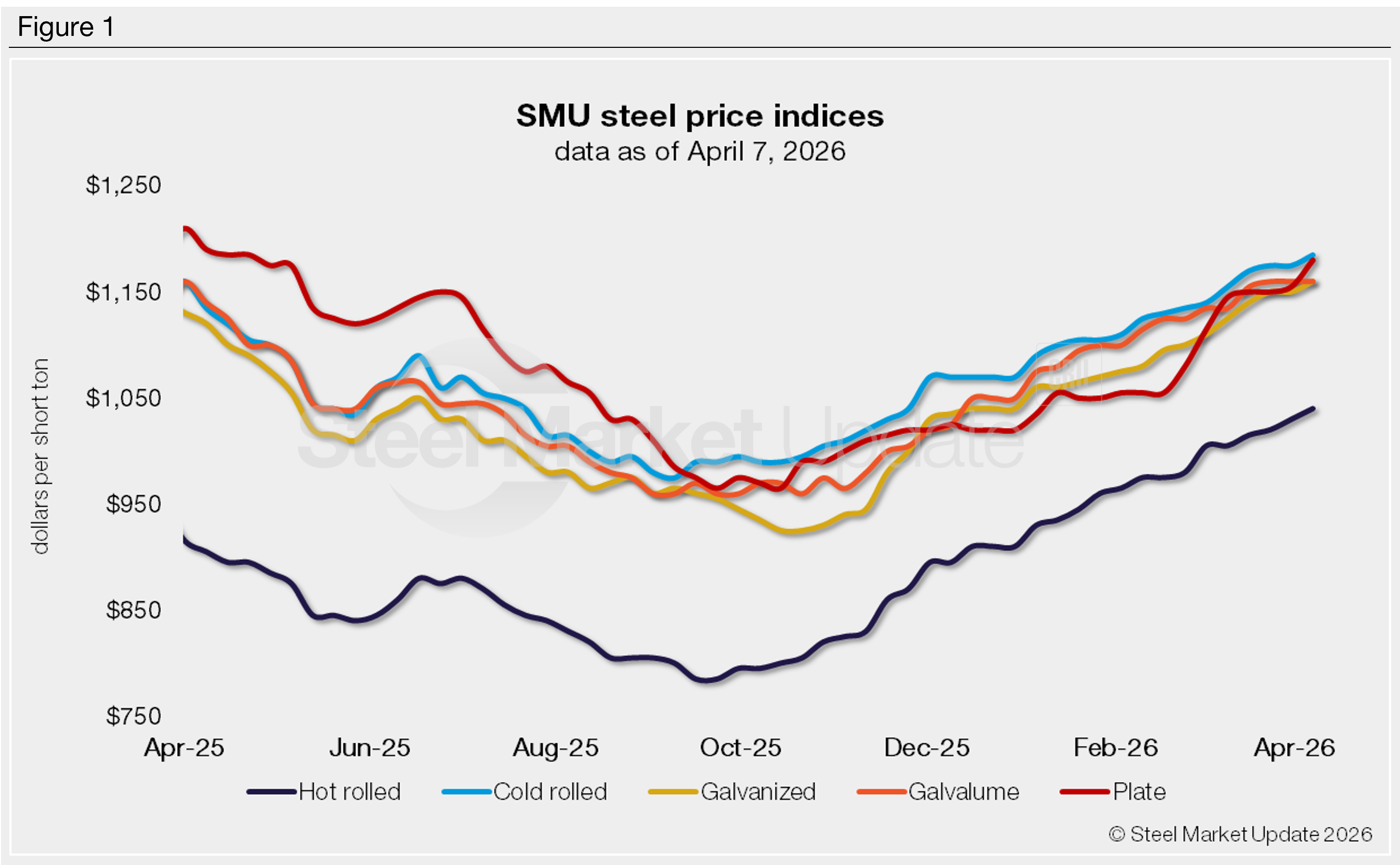

SMU’s price assessment for hot-rolled coil now stands at $1,040 per short ton (st), up $10/st from last week and up $130/st since the start of the year. The gains (at least in sheet) have been slow and steady, a stark contrast with the price spikes that have characterized pricing cycles in past years.

What people are saying

There remain questions about whether imports could play a bigger role in the market in late spring/early summer. But in the meantime, market participants tell us that while they can secure tonnage under contract terms, it’s become increasingly difficult to find mills with spot availability. And some warn inventories could move lower (perhaps dangerously low), assuming demand remains on track.

The result: The consensus on where and when the market might peak continues to reset higher. (We explore that topic in more detail in our latest Final Thoughts.)

The primary change in the market (as we noted in a prior Final Thoughts) might be higher fuel and freight costs and surcharges. Nucor rolled a new fuel surcharge for plate this week. We understand other flat-rolled mills began implementing similar practices as far back as early/mid-March, shortly after the outbreak of the Iran War.

We’re also told that Galvalume extras could reset higher on the heels of higher aluminum costs, which stem from a combination of Section 232 tariffs and production disruptions at major smelters in the Middle East. (Aluminum Market Update details those outages.)

Momentum remains at ‘higher’

While some market participants expressed concerns about the potential long-term impact of war-related inflation, few said they had seen any immediate change in the supply-demand balance in the domestic steel market.

SMU as a result has kept its momentum indicators for all sheet and plate products pointed higher. In other words, we expect prices to continue to increase in the short term.

Refer to Table 1 (click to enlarge) for our latest price indices and trends.

Hot-rolled coil: $1,020–1,060/st, averaging $1,040/st

The lower end of our range is up $20/st week over week (w/w), while the top end is unchanged. Our overall average is up $10/st w/w.

Hot-rolled lead times range from 4–9 weeks, averaging 6.5 weeks, according to our April 2 market survey. We will publish updated lead times on Thursday.

Cold-rolled coil: $1,150–1,220/st, averaging $1,185/st

The lower end of our range is unchanged week over week (w/w), while the top end is $20/st higher. Our overall average is up $10/st w/w.

Cold-rolled lead times range from 6–11 weeks, averaging 8.2 weeks through our latest survey.

Galvanized coil: $1,100–1,200/st, averaging $1,150/st

The lower end of our range is unchanged week over week (w/w), while the top end is $20/st higher. Our overall average is up $10/st w/w.

Galvanized .060×48” G90 benchmark: SMU price range is $1,210–1,290/st, averaging $1,250/st FOB mill, east of the Rockies.

Galvanized lead times range from 6–10 weeks, averaging 7.9 weeks through our latest survey.

Galvalume coil: $1,120–1,200/st, averaging $1,160/st

Our range was unchanged w/w.

Galvalume .0142×42” AZ50, grade 80 benchmark: SMU’s price range is $1,549–1,629/st, averaging $1,589/st FOB mill, east of the Rockies.

Galvalume lead times range from 6–10 weeks, averaging 8.4 weeks through our latest survey.

Plate: $1,130–1,180/st, averaging $1,155/st

The lower end of our range is up unchanged w/w, while the top end is up $50/st. Our overall average is up $25/st w/w.

Plate lead times range from 6–8 weeks, averaging 7.1 weeks through our latest survey.

David Schollaert

Read more from David Schollaert