AISI: Domestic steel output ticks back up

US steel mills have ramped up raw production since April, with weekly output steadily increasing in nearly every week since.

US steel mills have ramped up raw production since April, with weekly output steadily increasing in nearly every week since.

The resistance Brazilian pig iron sellers had shown to accepting lower prices has proved short-lived, sources told SMU.

Nucor maintained its weekly list price for hot-rolled (HR) coil this week, following two consecutive increases.

Not many people in the North American steel market had direct US involvement in another Middle East conflict on their bingo card. Prices weren't expected to shoot higher unless something unexpected happened. That unexpected something has now happened. And there is talk of oil at $100 per barrel. What does that mean for steel?

We’ll have a lot to talk about because construction is at the intersection of so many of today’s hot-button issues. The main question: Will construction thrive or dive in the rest of ’25? (Nothing wrong with a rhyme, even in serious times.)

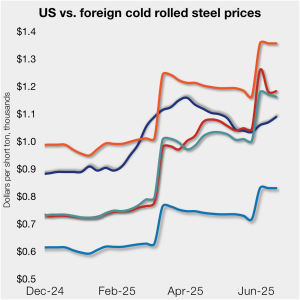

US cold-rolled (CR) coil prices continued to tick higher this week, while offshore markets were mixed.

Your highlights on the week in trade developments, price increases, scrap news, and more.

Oil and gas drilling activity declined in the US again this week the US, while Canadian counts improved, according to Baker Hughes.

The forceful headwinds bearing down on steel markets across the globe have created demand challenges and sent prices southward. The US, however, challenged the global trend.

According to our latest analysis, prices for four of the seven steelmaking raw materials we track declined from May to June. Collectively, these materials declined 3% month over month (m/m) and are down 9% compared to three months ago.

The moves include reciprocal procurement restrictions, import quotas, and the formation of stakeholder task forces for aluminum industries.

Now that the USS/Nippon deal has been completed, what's next?

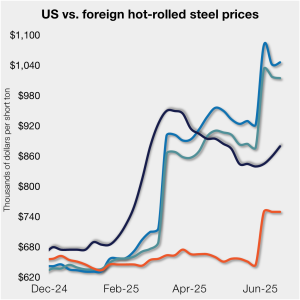

Several steel market sources say they were blindsided when mills increased spot prices for hot-rolled coils this week.

US hot-rolled coil prices crept up again this week but still trail imports from Europe.

Earlier this week, SMU polled steel buyers on an array of topics, ranging from market prices, demand, and inventories to imports and evolving market events.

Getting back to the price increases I mentioned at the top of this article, to what extent are they aimed at raising prices and to what extent are they aimed at stopping the bleeding that was happening in the second half of May, before President Trump announced the 50% tariff?

Steel prices inched higher again this week across most of the sheet and plate products tracked by SMU.

After climbing to a seven-month high in March, heating and cooling equipment shipments edged lower in April, according to the latest data released by the Air-Conditioning, Heating, and Refrigeration Institute (AHRI). Shipments of water heaters, air conditioner/heat pumps, and warm-air furnaces all declined month over month (m/m) but remain strong relative to the past three years.

The Trump administration has expanded the list of derivative steel products covered by the now 50% Section 232 tariff.

Domestic mills continue to produce record volumes of steel, according to AISI's latest figures.

Cleveland-Cliffs plans to increase prices for hot-rolled (HR) coil to $950 per short ton (st) with the opening of its July spot order book. The Cleveland-based steelmaker said the price hike was effective immediately in a letter to customers dated Monday.

Nucor raised its published weekly spot price for hot-rolled (HR) coil by $10 per short ton (st) on Monday.

Flat rolled = 57.1 shipping days of supply Plate = 55.7 shipping days of supply Flat rolled US service centers reined in flat roll supply in May, coinciding with declining shipments. At the end of May, service centers carried 57.1 shipping days of supply, according to adjusted SMU data. That’s down slightly from 57.6 shipping […]

We just wrapped another Steel 101 Workshop, where you take what you learned in the classroom into the steel mill.

Steel market participants learned that negotiations between the US and Mexico include discussions about Section 232 tariffs on steel and aluminum despite President Trump’s June 3 proclamation increasing the tariffs from 25% to 50% for all steel and aluminum imports—except for those from the UK.

US cold-rolled (CR) coil prices edged up again this week, and most offshore markets moved in the opposite direction. But the diverging price moves stateside vs. abroad did little to impact pricing trends. The bigger impact was from Section 232, which were doubled to 50% as of June 3. The higher tariffs have resulted in […]

Hashing out duty costs

If you’re feeling a sudden jerk and a case of tariff whiplash coming on, you’re not alone.

More developments with USS-Nippon. A look at whether imports will be needed. The latest prices. And more.

SMU’s latest steel buyers market survey results are now available on our website to all premium members. After logging in at steelmarketupdate.com, visit the pricing and analysis tab and look under the “survey results” section for “latest survey results.” Past survey results are also available under that selection. If you need help accessing the survey results, or if […]