Nucor ups HR spot price to $1,025/ton

Nucor raised its consumer spot price (CSP) for hot-rolled (HR) coil to $1,025 per short ton (st), up $10/st from last week.

Nucor raised its consumer spot price (CSP) for hot-rolled (HR) coil to $1,025 per short ton (st), up $10/st from last week.

Plate market sources say the week has been quiet, but that overall, business remains consistent.

As spot prices for hot- and cold-rolled coils edge higher, mill capacity utilization rates hover below 80%, raising concern among some market participants.

Most steel buyers report that domestic mills are unwilling to negotiate price on new sheet and plate spot orders.

Prices for both sheet and plate products climbed higher this week, with some rising to multi-year highs, according to SMU's latest market canvass.

Nucor raised its consumer spot price for hot-rolled coil to $1,015 per short ton, up $5/st from last week.

This week sources said spot prices on hot-rolled coils increased modestly.

A month ago, the steel market was defined by stability. Prices had firmed and held, and the HRC futures curve appeared to be absorbing strength and follow-through rather than rejecting it. Since then, that stability has evolved into something more meaningful, repricing.

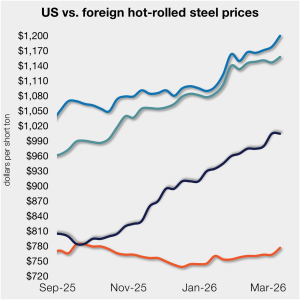

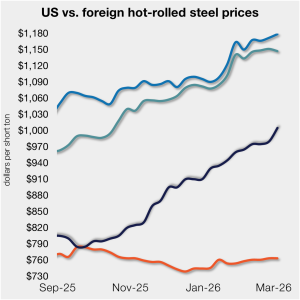

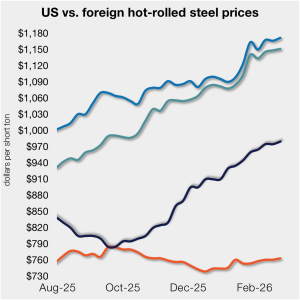

The price gap between US hot-rolled coil (HR) and landed offshore product widened this week, as stateside tags were little changed.

Domestic plate market participants expressed confidence in the overall improvement of market conditions this week.

Earlier this week, SMU polled steel buyers on an array of topics, ranging from market prices, demand, and inventories to tariffs, imports, and evolving market events.

Nucor Plate Group notified customers it is increasing prices on all rolled products by $40 per short ton (st) and $60/st on all heat treat products.

SMU's sheet and plate prices were flat or higher this week in a US market that remains characterized by extended lead times and limited spot availability.

The US scrap market softened in March as most grades traded sideways, with prices seen falling next month, sources told SMU.

Nucor’s consumer spot price (CSP) for hot-rolled coil increased to $1,010 per short ton (st), up $5/st from last week.

Prices are moving up and lead times moving. And most people expect them to continue to do so for a little while longer, according to our latest survey results. But there is one big wildcard: the Iran war.

Participants in the US hot- and cold-rolled sheet market cautiously called the week a win as prices inched north and demand picked up.

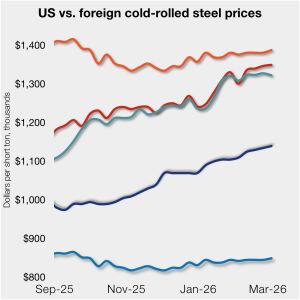

Cold-rolled (CR) coil prices ticked up in the US this week, matching a similar trend seen in most offshore markets as well.

Oregon Steel Mills and SSAB Americas announced higher plate prices to close out the week.

The main impact on the ferrous value chain from the Middle East conflict will be the higher energy costs in a prolonged scenario.

The price gap between US hot-rolled coil (HR) and landed offshore product tightened this week, as stateside tags continue to rise.

Most steel buyers responding to our market survey this week said domestic mills remain unwilling to negotiate lower prices for new spot orders.

Let’s say the going price for HR is around $1,000/st. Want to place a 1,000-ton spot order at that price? Good luck. It probably won’t be easy.

SMU's sheet and plate prices increased this week to new multi-month highs.

Crude-oil and natural-gas prices spiked, metals opened higher and some fertilizer benchmarks climbed after the US and Israel launched a “pre-emptive” strike on Iran, killing the supreme leader and plunging the region into chaos.

Nucor’s consumer spot price (CSP) for hot-rolled coil increased to $1,005 per short ton (st), up $15/st from last week.

Sources in the domestic hot- and cold-rolled coil market said they are beginning to feel prices creeping up this week.

The price gap between US hot-rolled coil (HR/HRC) and landed offshore product remained largely flat again this week, as price movements stateside and abroad mirrored each other.

SMU polled steel buyers on an array of topics, ranging from market prices, demand, and inventories to tariffs, imports, and evolving market events.

US hot-rolled coil prices are set to rise year on year in 2026, but the market will face heightened volatility as import flows recover and new domestic capacity comes online, CRU Research Principal Josh Spoores said at this year's Tampa Steel Conference.