December scrap settle seen down $10-20/gt

The scrap market in the US finally settled on Monday with one of the nation’s largest steelmakers issuing its price bids.

The scrap market in the US finally settled on Monday with one of the nation’s largest steelmakers issuing its price bids.

Nucor’s weekly spot price for hot-rolled (HR) coil will remain at $750 per short ton (st) for a fifth week.

As my colleague Ethan Bernard noted in our most recent Final Thoughts, I don’t think many of us thought uncertainty would be mounting four weeks out from 2025. If anything, the general theme post-Steel Summit and into Q4 was that election night would be the turning point. And whatever had been keeping the steel market from building would finally get the jump-start it needed.

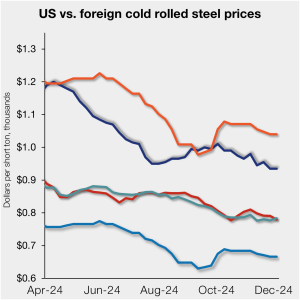

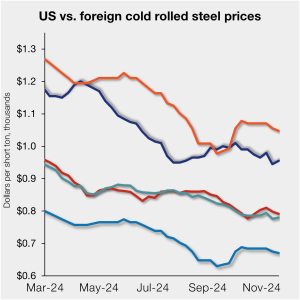

The price spread between US-produced cold-rolled (CR) coil and offshore products on a landed basis was flat in the week ended Dec. 6.

A newly adjusted anti-dumping duty on imports of oil country tubular goods (OCTG) from Argentina is too low, according to U.S. Steel. This past week, the Department of Commerce released the preliminary results of annual AD duty order reviews on OCTG from both Argentina and Mexico. It is reviewing imports during the one-year period that […]

The US scrap market has begun forming for December shipment and prices seem to be sagging so far.

The US drill rig count increased by seven this week, while the Canadian count dropped by 11, according to the latest data from Baker Hughes.

SMU’s latest steel buyers market survey results are now available on our website to all premium members. After logging in at steelmarketupdate.com, visit the pricing and analysis tab and look under the “survey results” section for “latest survey results.” Past survey results are also available under that selection. If you need help accessing the survey results, or if […]

Domestic steel shipments were down month over month and on-year in October.

The ferrous scrap market hasn’t settled yet for December, but sources say mills are looking to push scrap prices down.

SMU's price indices saw minor fluctuations on sheet products this week, while our plate and Galvalume indices held steady.

US plate prices are at their lowest level in nearly four years and mills continue to do what they can to limit the bleeding. Domestic prices are now just a fraction of their all-time high of $1,940 per short ton (st) reached in May 2022, and trending lower.

On Monday, Nucor published new extras effective Jan, 4, 2025.

The slowdown in North American zinc demand in recent months has played out across all sectors, and CRU now expects it to contract by 3.7% y/y.

The ferrous scrap markets both here and abroad are displaying a definite lack of enthusiasm as we head into the holiday season.

Steel Market Update’s Steel Demand Index recovered by nearly 10 points last week, though it still remains in contraction territory.

Prices were stable to down in November for all seven steelmaking raw materials tracked by SMU, according to our latest analysis.

Nucor is holding its hot-rolled (HR) coil base price flat at $750/st for the third week in a row.

The price spread between US-produced cold-rolled (CR) coil and offshore products on a landed basis widened slightly in the week ended Nov. 22.

US rig activity has remained in multi-year low territory since June. Drilling in Canada has edged lower across the last few weeks but remains historically strong.

Trademark Metals Recycling opened an advanced metal recovery facility in Bushnell, Fla.

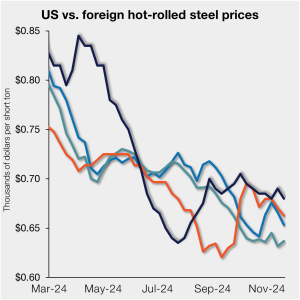

US hot-rolled (HR) coil prices slipped this week, while tags in offshore markets were also largely down. Thus, the price premium between stateside hot band and imports on a landed basis was relatively unchanged.

SMU’s flat-rolled steel prices were mixed this week with slight declines across most products and a modest increase in prices for cold-rolled coil.

The price spread between hot-rolled coil (HRC) and prime scrap remained the same in November as both tags were at the levels seen a month earlier, according to SMU’s most recent pricing data.

This CRU analysis from discusses steel sheet prices, demand, and inventory levels around the globe this past week.

The investment is aimed at growing Kloeckner’s automotive and industrial segment in the US and Mexico.

Ferrous scrap prices were largely rangebound to down at the November settle, market sources told SMU.

The pig iron markets have retreated over the last two months amidst a concerted effort by US-based buyers to drive down prices to more closely follow the lower domestic scrap prices.

Following a strong August, total heating and cooling equipment shipments eased in September to a five-month low, according to the latest data from the Air-Conditioning, Heating, and Refrigeration Institute (AHRI).

Slowing growth in data center planning and nonresidential projects caused the Dodge Momentum Index (DMI) to pull back in October.