SMU Price Ranges: Sheet and plate prices flat or up (again) – for how long?

Sheet and plate prices were flat or modestly higher this week, continuing a trend we’ve seen since the beginning of Q4. The big question: How much longer can the trend hold?

Sheet and plate prices were flat or modestly higher this week, continuing a trend we’ve seen since the beginning of Q4. The big question: How much longer can the trend hold?

Nucor has increased its consumer spot price (CSP) for hot-rolled (HR) coil to $1,035 per short ton (st), a $10/st bump from last week.

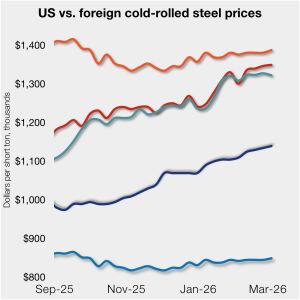

CR imports from Germany, Italy, and Japan on a landed basis remain much more expensive than domestic product. But South Korean imports remain competitive, in theory, even with the 50% Section 232 tariff.

Most steel buyers see prices continuing to inch higher on stable or improving demand. But some are concerned higher energy prices stemming for the Iran war could dent the overall economy.

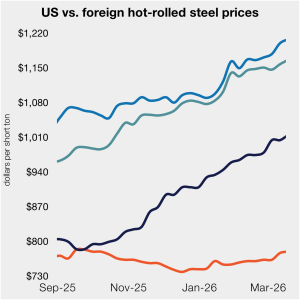

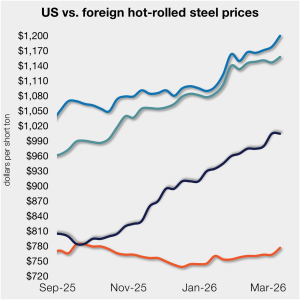

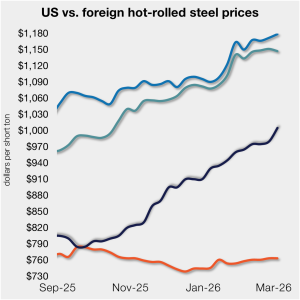

The price gap between US hot-rolled coil (HR) and landed offshore product remained within a tight band this week. The dynamic continues as both stateside and offshore prices have trended higher.

North American auto assemblies gained ground in February, up more than 8% vs. January, but still down more than 4% year on year (y/y), according to GlobalData.

The galvanized sheet market continued to tighten in March as distributors and service centers reported firm demand, low inventory levels, and rising transportation costs. Participants on the monthly HARDI sheet metal and air-handling call on Wednesday described a market defined by constrained supply and steady upward pricing pressure.

Sheet prices continue to inch higher. And people who once thought hot-rolled coil (HR) prices couldn’t go above $1,000 are now saying $1,100 doesn’t seem out of the question.

The pace of sheet and plate price increases slowed this week, with most products holding at some of the highest levels seen in over a year.

Mexico’s Ministry of Economy issued a preliminary ruling in its anti-dumping case on hot-rolled steel from China and Vietnam. The government found evidence of price discrimination and imposed provisional duties on a wide range of hot-rolled flat products, including coils, sheet, strip, and plate.

As spot prices for hot- and cold-rolled coils edge higher, mill capacity utilization rates hover below 80%, raising concern among some market participants.

Steel mill lead times extended to multi-year highs on both sheet and plate products this week.

Most steel buyers report that domestic mills are unwilling to negotiate price on new sheet and plate spot orders.

US service centers’ flat-rolled steel supply declined for a second consecutive month in February, with shipping days of supply slipping to 52.2 on an adjusted basis, according to SMU data.

Prices for both sheet and plate products climbed higher this week, with some rising to multi-year highs, according to SMU's latest market canvass.

US steel exports jumped 33% in January but remain historically low, according to recently released US Department of Commerce data.

Nucor raised its consumer spot price for hot-rolled coil to $1,015 per short ton, up $5/st from last week.

Steel imports remained close to multi-year lows in January and February, according to US Commerce Department data released this week.

This week sources said spot prices on hot-rolled coils increased modestly.

A month ago, the steel market was defined by stability. Prices had firmed and held, and the HRC futures curve appeared to be absorbing strength and follow-through rather than rejecting it. Since then, that stability has evolved into something more meaningful, repricing.

The price gap between US hot-rolled coil (HR) and landed offshore product widened this week, as stateside tags were little changed.

Earlier this week, SMU polled steel buyers on an array of topics, ranging from market prices, demand, and inventories to tariffs, imports, and evolving market events.

SMU's sheet and plate prices were flat or higher this week in a US market that remains characterized by extended lead times and limited spot availability.

Nucor’s consumer spot price (CSP) for hot-rolled coil increased to $1,010 per short ton (st), up $5/st from last week.

Prices are moving up and lead times moving. And most people expect them to continue to do so for a little while longer, according to our latest survey results. But there is one big wildcard: the Iran war.

Participants in the US hot- and cold-rolled sheet market cautiously called the week a win as prices inched north and demand picked up.

Cold-rolled (CR) coil prices ticked up in the US this week, matching a similar trend seen in most offshore markets as well.

Following extensions in February, steel mill lead times held steady or extended further for both sheet and plate products this week, according to buyers responding to our latest market survey.

The price gap between US hot-rolled coil (HR) and landed offshore product tightened this week, as stateside tags continue to rise.

Most steel buyers responding to our market survey this week said domestic mills remain unwilling to negotiate lower prices for new spot orders.