Commerce tweaks CVDs on Korean CR

CVDs and anti-dumping duties matter when importing steel. Korea often offers very competitive import rates. The importer of record is responsible for paying any ADs, CVDs, or tariffs.

CVDs and anti-dumping duties matter when importing steel. Korea often offers very competitive import rates. The importer of record is responsible for paying any ADs, CVDs, or tariffs.

Let’s say the going price for HR is around $1,000/st. Want to place a 1,000-ton spot order at that price? Good luck. It probably won’t be easy.

SMU's sheet and plate prices increased this week to new multi-month highs.

Nucor’s consumer spot price (CSP) for hot-rolled coil increased to $1,005 per short ton (st), up $15/st from last week.

Sources in the domestic hot- and cold-rolled coil market said they are beginning to feel prices creeping up this week.

Trade for many of the sheet and plate products we follow has fallen to multi-year lows through December.

With domestic steel prices rising steadily and mill lead times pushing out, import offers are becoming more attractive to US buyers.

Sheet prices continue to grind higher on tight supply and 'okay' demand. Plate finally saw some movement after weeks of stability as price increases begin to stick.

SMU sits down with JSW Steel USA CEO Rob Simon.

North American auto assemblies recovered in January, up nearly 12% vs. December, though down more than 2% year on year (y/y), according to GlobalData.

Nucor’s consumer spot price (CSP) for hot-rolled coil increased to $990 per short ton (st), up $10/st from last week.

Participants in the domestic sheet market say they experienced lighter inquiries and fewer orders than in previous weeks, rendering domestic mill price increases for spot-market hot- and cold-rolled coils irrelevant.

Hot rolled and galvanized lead times are about half a week longer than they were three months ago, while production times for cold rolled, Galvalume, and plate products are one to two weeks longer.

Since late 2025, mills have begun to hold a firmer stance on prices, tightening their grip at the start of this year and holding on since

As referenced in Michael Cowden's last Final Thoughts, Mexico has opened a formal investigation into cold-rolled steel imports from the US, China, and Malaysia. Here are the details.

Three of SMU’s price indices increased this week, while two remained steady, all holding at multi-month highs.

Nucor increased its list price for hot-rolled (HR) coil to $980 per short ton (st) on Monday, up $5/st from last week.

CRU: US Midwest sheet prices have continued to rise from our mid-January assessment.

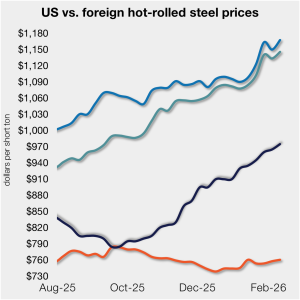

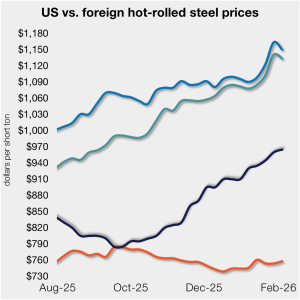

The price gap between US hot-rolled coil (HR/HRC) and landed offshore product was largely flat this week, as price movements stateside and abroad mirrored each other. Still, the premium for US hot band over imports has remained in a relatively tight band since early December.

SMU’s sheet price indices inched up to new multi-month highs this week, while plate prices held steady.

Friedman Industries delivered a strong fiscal third quarter, posting sharp gains in sales, shipments, and margins across both its flat-rolled and tubular segments.

AZZ Inc. expects steady top-line growth and improved annual earnings, capitalizing on new capacity ramp-up and strong downstream demand.

Nucor’s consumer spot price (CSP) for hot-rolled coil increased to $975 per short ton (st), up $5/st from last week.

The Dodge Momentum Index (DMI) fell 6.2% in January to 272.7, retreating from December’s downwardly revised reading of 291.0, according to the latest data released by Dodge Construction Network.

The price gap between US hot-rolled coil and landed offshore product narrowed this week, as price movements stateside and abroad diverged.

November steel exports tumbled 15% from October to the lowest monthly export rate since July 2020.

One third of the steel buyers responding to our market survey this week reported that domestic mills are negotiable on new spot order pricing. Mills began to hold a firmer stance on prices towards the end of last year, tightening their grip in early January and holding it since.

Steel mill lead times marginally declined on sheet products this week but edged higher on plate, according to responses from SMU’s latest market survey. Overall, lead times remain one to two weeks longer than levels seen three months ago.

U.S. Steel plans to idle the No. 14 blast furnace at its Gary Works near Chicago for a reline for ~100 days from May to August.

Since my last column, confidence within the physical market has been restored. However, that does not mean necessarily confidence in the outlook for demand. More so, it's confidence that better pricing is not lurking around the corner. So where do we go from there?