AISI: Raw steel production ticks back up

US raw steel output rebounded last week, according to the American Iron and Steel Institute (AISI). Mill production remains historically strong, with output at or near a multi-year high since early June.

US raw steel output rebounded last week, according to the American Iron and Steel Institute (AISI). Mill production remains historically strong, with output at or near a multi-year high since early June.

Is this just a severe case of the summer doldrums? Will demand improve in the fall, as it often does? Or has uncertainty around tariffs and the economy created a more lasting impact?

Chief executive of the Institute for Supply Management (ISM), Tom Derry highlighted how reactive buying behavior has shifted the market into a quiet demand period. Derry presented ISM data during the weekly SMU community chat.

U.S. Steel and Nippon Steel are not done settling scores with those who opposed their historic, $14.9-billion partnership.

Drilling activity slowed in the US and increased in Canada last week, according to the latest oil and gas rig count data released by Baker Hughes.

SMU’s Steel Buyers’ Sentiment Indices eased this week, both approaching multi-year lows.

President Trump said a negotiated deal with Canada might not occur, and all existing tariffs, along with those set to take effect soon, will stay in place, according to media reports.

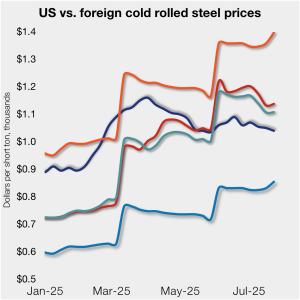

Cold-rolled (CR) coil prices continued to decline in the US this week, while prices in offshore markets ticked higher.

SMU’s latest steel buyers market survey results are now available on our website to all premium members.

US tariff expansion to stainless material in imported downstream products will not be enough on its own to incentivize capital investment

Is there any clarity to be hoped for on the tariff front?

Steel mill lead times on sheet products contracted across the board this week compared to early July, while plate production times moderately extended, according to steel buyers responding to this week’s market survey.

More than nine out of every ten steel buyers polled by SMU this week reported that mills are negotiable on new order prices. Negotiation rates have increased in each of our last three surveys following the early-June lull, reaching a record high this week.

Despite improved operating results, SSAB Americas' second-quarter and H1’25 profits fell short of those of last year.

Hot-rolled (HR) coil prices in the US edged lower again this week but have remained in a tight band for roughly four months. Stateside prices continue to trail imports from Europe, supported by Section 232 steel tariffs that were doubled in early June.

The total volume of raw steel produced around the globe fell by 5% from May to June, according to recent data published by the World Steel Association (worldsteel).

The latest SMU Community Chat webinar reply featuring Tom Derry of the Institute for Supply Management (ISM), is now available on our website to all members.

Metalforming manufacturers say they’re more confident that near-term economic conditions are improving

A tariff on Brazilian pig iron could cause great upheaval in the market.

Steel prices continued to decline this week across all of the sheet and plate products tracked by SMU, pressured by short lead times and the typical summer slowdown.

Galvanized steel prices ping-ponged in the $50/hundredweight range during the month of July, settling in at roughly the same position as in June.

Institute for Supply Management CEO Tom Derry will join SMU for our next Community Chat on Wednesday, July 23, at 11 a.m. ET (10 a.m. CT). You can register here.

SMU’s Mill Order Index (MOI) rebounded in June after declining for three straight months. The gain complemented a modest boost in service center shipments for the month, according to our latest service center inventories data.

Domestic steel mill output edged lower last week, according to the American Iron and Steel Institute (AISI). While down, production remains historically strong since peaking in early June.

Nucor is lowering its list price for spot hot-rolled coil for the first time since May 27.

What to look out for regarding ferrous scrap ahead of Steel Summit.

Drilling activity increased in both the US and Canada for the week ended July 18, according to the latest data from Baker Hughes.

Section 232 tariffs have doubled to 50%. Reciprocal tariffs rates remain uncertain. But while prices have softened on even softer sentiment, tariffs have firmed the floor.

US housing starts recovered slightly in June after reaching a five-year low the month prior, according to figures recently released by the US Census Bureau.

Cold-rolled (CR) coil prices continued to tick lower in the US this week, with a similar trend seen in offshore markets.