Nucor's hikes list price for HRC by $10/ton

Nucor raised its published weekly spot price for hot-rolled (HR) coil by $10 per short ton (st) on Monday.

Nucor raised its published weekly spot price for hot-rolled (HR) coil by $10 per short ton (st) on Monday.

Flat rolled = 57.1 shipping days of supply Plate = 55.7 shipping days of supply Flat rolled US service centers reined in flat roll supply in May, coinciding with declining shipments. At the end of May, service centers carried 57.1 shipping days of supply, according to adjusted SMU data. That’s down slightly from 57.6 shipping […]

We just wrapped another Steel 101 Workshop, where you take what you learned in the classroom into the steel mill.

Steel market participants learned that negotiations between the US and Mexico include discussions about Section 232 tariffs on steel and aluminum despite President Trump’s June 3 proclamation increasing the tariffs from 25% to 50% for all steel and aluminum imports—except for those from the UK.

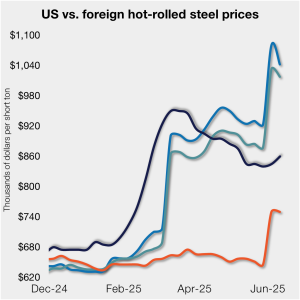

US cold-rolled (CR) coil prices edged up again this week, and most offshore markets moved in the opposite direction. But the diverging price moves stateside vs. abroad did little to impact pricing trends. The bigger impact was from Section 232, which were doubled to 50% as of June 3. The higher tariffs have resulted in […]

If you’re feeling a sudden jerk and a case of tariff whiplash coming on, you’re not alone.

More developments with USS-Nippon. A look at whether imports will be needed. The latest prices. And more.

SMU’s latest steel buyers market survey results are now available on our website to all premium members. After logging in at steelmarketupdate.com, visit the pricing and analysis tab and look under the “survey results” section for “latest survey results.” Past survey results are also available under that selection. If you need help accessing the survey results, or if […]

SMU’s Steel Buyers’ Sentiment Indices moved in opposing directions this week. Our Current Steel Buyers’ Sentiment Index sharply fell to one of the lowest levels recorded in five years, while Future Buyers’ Sentiment marginally improved.

Subdued demand has continued to weigh on steel sheet prices globally.

Steel equities and steel futures fell hard after news broke earlier this week that the US and Mexico might reach an agreement that would result in the 50% Section 232 tariff coming off Mexican steel. The sharp declines didn’t make much sense, especially if, as some reports indicate, Mexico might agree to a fixed quota. They didn't make sense even if steel flows between the US and Mexico remain unchanged.

All five of the averages for sheet and plate mill lead times tracked by SMU extended moderately this week, according to buyers responding to our latest market survey.

Most steel buyers responding to our market survey this week reported that domestic mills are considerably less willing to talk price on sheet products than they were in recent weeks, but remain open to bargain on plate prices.

Following three months of little to no growth, the Dodge Momentum Index (DMI) increased in May, according to the latest data released by Dodge Construction Network

The US steel industry is edging closer to independence from imports, and it may only take one more mill to tip the scales, according to Timna Tanners, managing director at Wolfe Research.

Domestic hot-rolled (HR) coil prices edged up marginally again this week, while offshore prices ticked down.

The latest SMU Community Chat webinar reply featuring Timna Tanners, managing director of equity research for Wolfe Research, is now available on our website to all members. After logging in at steelmarketupdate.com, visit the community tab and look under the “previous webinars” section of the dropdown menu. All past Community Chat webinars are also available under that selection. If […]

We’ll have a lot to talk about because construction is at the intersection of so many of today’s hot-button issues. The main question: Will construction thrive or dive in the rest of ’25? (Nothing wrong with a rhyme, even in serious times.)

Steel industry veteran David ‘Dave’ Aycock died on Saturday at the age of 94.

The price spread between HRC and prime scrap widened in June.

ArcelorMittal’s (AM) Hamilton location to be shuttered, wire production shifting to Montreal.

The amount of finished steel that entered the US market in April declined 3% from March but remained at elevated levels, according to SMU’s analysis of Department of Commerce and American Iron and Steel Institute (AISI) data.

Even before the news about Mexico, I didn’t want to overstate the magnitude of the change in momentum. As far as we could tell, there hadn’t been a frenzy of new ordering following President Trump’s announcement of 50% Section 232 tariffs. But higher tariffs had unquestionably raised prices for imports, which typically provide the floor for domestic pricing. We’d heard, for example, that prices below $800 per short ton for hot-rolled (HR) coil were gone from the domestic market – even for larger buyers.

Steel prices climbed for a second straight week across all five sheet and plate products tracked by SMU.

Brazilian pig iron prices fail to rise after ferrous scrap market settle.

Ferrous scrap prices in the US have remained stable from May to June.

The Atlanta-based company informed customers on Monday it is shutting down its metal division while continuing to operate the logistics business.

Subdued demand is causing importers to cancel hot-rolled (HR) coil orders and renegotiate the terms of shipments currently enroute to the US, importers say. An executive for a large overseas mill said customers might find it difficult to justify making imports buys after US President Donald Trump doubled the 25% Section 232 tariff on imported steel […]

Domestic steel mills are ramping up production, according to the American Iron and Steel Institute (AISI), with output rising to a three-year high last week.

US steel exports totaled 579,000 short tons (st) in April, according to US Department of Commerce data. That's the lowest monthly volume recorded since July 2020.