Nucor lifts list price for spot HRC by $20/ton

The $20/short ton increase applies to all of the steelmaker’s sheet mills, including West Coast joint-venture subsidiary CSI.

The $20/short ton increase applies to all of the steelmaker’s sheet mills, including West Coast joint-venture subsidiary CSI.

I want to draw your attention to SMU’s monthly scrap market survey. It’s a premium feature that complements our long-running steel market survey. We’ve been running our scrap survey since late January. And over just that short time, it’s become a valuable way not only for us to assess where scrap prices might go but also to quantify some of the “fuzzy” indicators - like sentiment and flows - that help to put the price in context.

Domestic hot-rolled coil prices edged up marginally this week, while offshore prices ticked down.

With the pace that news has been breaking lately, there will be no shortage of things to discuss.

Oil and gas drilling activity was mixed this week, according to Baker Hughes. US totals slipped for a sixth straight week, while Canada saw a slight bump in activity.

The increases are effective June 6.

Timna Tanners, managing director of equity research for Wolfe Research, will be the featured speaker on the next SMU Community Chat. The webinar will be on Wednesday, June 11, at 11 am ET. It’s free to attend.

This CRU Insight examines how the increase in Section 232 tariffs on steel to challenging levels will lead to significatively higher prices for end consumers in the US market.

SMU’s ferrous scrap market survey results are now available on our website to all premium members. After logging in at steelmarketupdate.com, visit the pricing and analysis tab and look under the “survey results” section for “ferrous scrap survey” results. Past flat-rolled survey results are also available under that selection. If you need help accessing the survey results, […]

April now represents the third-lowest monthly import rate witnessed in nearly two and a half years, with several steel products falling to multi-year lows

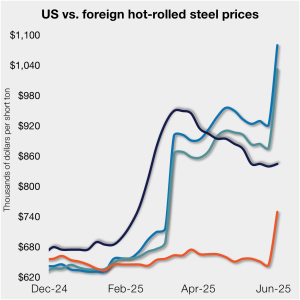

I think there is an obvious case for sheet and plate prices going higher from here. That’s because, on a very basic level, the floor for flat-rolled steel prices, which is typically provided by imports, is now significantly higher than it was a week ago.

US manufacturers brace for the implications spurred by the latest round of Section 232 tariffs.

The startup steelmaker produced its first rebar at its greenfield steel mill in Osceola, Ark., marking a key milestone by completing construction in 22 months.

How is the ferroalloys market in the US faring with the new tariffs.

On Monday and Tuesday, SMU polled steel buyers for their thoughts on the current market. We received an array of feedback, including prices, demand, inventories, imports, and evolving market events.

Following eight consecutive weeks of declines, sheet and plate prices saw some upward movement this week in the wake of last Friday’s Section 232 tariff increase announcement. Gains varied by product.

We're about to hit 50% Section 232 steel tariffs. What could happen?

Service centers and distributors contend that weak demand is to blame for the flattening of domestic steel spot prices, as reflected in Nucor Steel’s weekly Consumer Spot Price (CSP) notice. On Monday, the Charlotte, North Carolina-headquartered steel producer left prices unchanged from the previous week. Nucor has maintained prices of plate produced in Brandenburg since March 28.

SMU’s Monthly Review provides a summary of our key steel market metrics for the previous month, with the latest data updated through May 30.

US raw steel production rose again last week, climbing to the highest weekly output recorded since last September, according to the American Iron and Steel Institute (AISI).

The American Iron and Steel Institute has tapped four members for its board.

Nucor halted a four-week decline in its spot price for hot-rolled coil this week, maintaining its weekly consumer spot price (CSP) at $870/st.

With higher tariff rates on steel and aluminum set to go into effect on Wednesday, June 4, a new round of chaos across the supply chain is likely in store. Expect a significant impact on manufacturers and metal fabricators. But even before the latest round of Trump-tariff whiplash on Friday evening, there was a lot of interesting data coming out of SMU's steel-market survey.

Timna Tanners, managing director of equity research for Wolfe Research, will be the featured speaker on the next SMU Community Chat. Timna has coined Sheet Storm, Galv Galore, and Rebarmageddon. Her forecasts and insights are always though provoking. And she’s not afraid to speak her mind. So it's no surprise that she's one of our most popular guests!

The price premium of galvanized coil over hot-rolled (HR) coil has narrowed over the past two months, resuming the downward trend seen for most of the last year. As of May 27, the spread between these two products is at one of its lowest levels in nearly two years.

Highlights from the week and things to keep an eye on.

SMU’s latest steel buyers market survey results are now available on our website to all premium members. After logging in at steelmarketupdate.com, visit the pricing and analysis tab and look under the “survey results” section for “latest survey results.” Past survey results are also available under that selection. If you need help accessing the survey results, or if […]

After reaching multi-month lows in mid-May, SMU’s Buyers’ Sentiment Indices modestly recovered in our latest survey.

CRU analysts discuss how downward pressure on the US premium has persisted due to weakness in key consuming sectors, while concerns over zinc supply have been largely alleviated for the time being.

A short tour of key dates in the Nippon/USS deal, and what the future might hold.