IIMA meeting: Decarbonization to drive demand for scrap, DRI

In the Americas, the ongoing conversion to EAF melting is driving demand for prime grades of scrap and increased use of ore-based metallics

In the Americas, the ongoing conversion to EAF melting is driving demand for prime grades of scrap and increased use of ore-based metallics

We moved our pricing momentum indicators from “lower” to “neutral” for all sheet products this week. For those keeping score, we had been at “lower” for six weeks. And I know some of you think we should have been there for even longer.

Voestalpine and partners have begun building an industrial-scale Hy4Smelt demonstration plant in Linz, Austria, which they hope will become key in the decarbonization of steel.

Domestic mills praised the US International Trade Commission’s (ITC's) final determination that imports of corrosion-resistant (CORE) steel from 10 countries pose a threat to them.

Most steelmaking raw material prices held steady or ticked higher over the past month

Algoma Steel has publicly confirmed that it might scale back its presence in the US market. It's no secret why: 50% Section 232 tariffs remain in place against Canada, which has traditionally been one of our closest allies.

The US International Trade Commission (ITC) finds that corrosion resistant steel (CORE) imports from 10 countries have caused material damage to domestic product producers, according to the ITC’s statement.

The ferrous scrap market is still searching for clues about the direction of the October market.

August marked the second-lowest monthly production rate this year, down 13% from the two-year high of 166.6 million mt in March.

A compromise has been reached in the pig iron market, sources told SMU. Recall we reported US buyers were bidding $390 per metric ton (mt) FOB or less while sellers were holding sideways at about $400/mt.

For the next month, CRU forecasts that global demand for steelmaking raw materials will increase month on month (m/m).

The pig iron market in Brazil is currently in flux and there have been few, if any, confirmed cargoes transacted for the US.

A recap of this week's steel industry news...

International trade law and policy remain a hot topic in Washington and beyond this week. We are paying special attention to the ongoing litigation of the president’s tariff policies and the administration’s efforts to heighten trade enforcement.

Following a 3% decline in June, the amount of steel shipped outside of the US edged up 1% in July to 623,000 short tons. July was the sixth-lowest monthly export rate since the COVID-19 pandemic, and...

ArcelorMittal has partially restarted operations at its direct reduction plant in Lazaro Cardenas, Michoacan. An explosion on Aug. 18 rocked the massive steelworks on Mexico’s Pacific coast, impacting production of direct-reduced iron (DRI).

US steel imports declined for the second consecutive month in July, according to recently finalized US Commerce Department data.

Here are highlights of what’s happened this past week and a few upcoming things to keep an eye on.

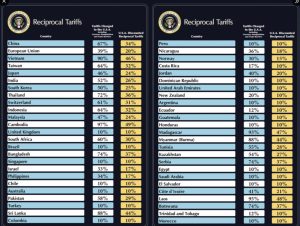

Repealing any reciprocal tariffs placed by President Donald Trump on US imports of direct reduced iron (DRI), iron ore, hot-briquetted iron (HBI), and pig iron would have only a nominal impact on the US steel market, market participants said.

The Brazilian-US pig iron market has remained quiet, market sources told SMU.

he US longs market remained stable this month despite ongoing challenges from tariff-impacted imports, even as end-use demand was relatively unchanged and scrap prices held flat in August.

Could an upcoming BRICS meeting spell trouble for President Trump's trade policy?

Ternium CEO Máximo Vedoya predicts that China is going to reduce its steel overcapacity.

Nucor’s Dan Needham views the steelmaker’s flexibility and diversification as key to pivoting when economic conditions require.

Thais Terzian, principal analyst at CRU, gave a presentation of Ore-Based Metallics(OBM), namely pig iron and direct-reduced iron (DRI), and how important they are to the global steel industry.

Most steelmaking raw material prices we track saw little change across the month of August. Iron ore, pig iron, shredded scrap, busheling scrap, zinc, and aluminum prices all held relatively steady,

The Commerce Department announced the final anti-dumping and countervailing duty (CVD) margins in the sprawling trade case investigating corrosion-resistant steel imports.

World crude steel output declined for a second straight month in July, falling 2% from June to an estimated 150.1 million metric tons (mt), according to recent data published by the World Steel Association (worldsteel).

The big show is here again. SMU Steel Summit begins on Monday. This year, like last year, more than 1,500 people will be joining us. And I couldn’t be more excited to have everyone here in Atlanta.

Domestic sheet prices in the US remained under pressure, limiting interest in imports, while domestic prices for longs products continued to rise.